Image you’re Jeff Bezos, circa 1998. You’re building a company (Amazon) that stands to make you and your compatriots vastly rich.

But looking forward, you see a problem: if your company makes profits, it will have to pay taxes on them. (At least nominally, in theory, 35%!) Then you and your investors will have to pay taxes on them again when they’re distributed to you as dividends. (Though yes, at a far lower 20% rate than what high earners pay on earned income.) Add those two up over many years, and you’re talking tens, hundreds of billions of dollars in taxes.

You’re a very smart guy. How are you going to avoid that?

Simple: don’t show any profits (or, hence, distribute them as dividends). Consistently set prices so you constantly break even. This has at least three effects:

1. You undercut all your competitors’ prices, driving them out of business. Nobody who’s trying to make a profit can possibly compete.

2. You control more and more market share.

3. You build a bigger and bigger business.

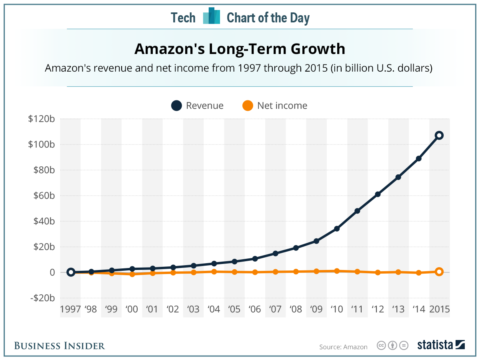

Number 3 is how you monetize this, personally. The value of the company (its share price/market cap) rises steadily. Obviously, a business with $136 billion in revenues (2016) is going to be worth more than one with $10 or $50 billion in revenues — even if it never shows a “profit.” You take your profits in capital gains.

Because stock-market investors are always going to be thinking: “They could always turn the dial from market share to profits. Just raise prices a skootch, and reap the harvest. In spades.”

But: they never do. It’s like a perpetual-motion machine, or holding yourself up by your own bootstraps. All that rising valuation is eternally based on the fact that they could raise prices and deliver profit (and yes: they could). In the meantime the business both generates and has massive value. It employs 270,ooo people, delivers zillions in employee compensation, pays zillions more to suppliers, receives hundreds of billions in revenues, and dominates whole segments of multiple industries. Are there really no “profits”? Nobody’s being irrational here.

Here are the results of your long-term plan:

Half a trillion dollars in revenues.

Essentially zero profits. Ever.

Dollars delivered onto investors’ balance sheets? Somewhere north of 300 billion.

And instead of being double-taxed on profits for all that time, investors’ income is taxed once, at the low 20% capital gains rate. And that, only when those gains are “realized” through sale of the stock. In the meantime it’s all tax-deferred — yet another huge effective-tax-rate win for shareholders. The longer they hold, the bigger the win. If they pass the stock on to their heirs, those gains are never taxed at all.

And just to mention in passing, none of that shareholder income ever appears as household income in the national accounts. It might as well not exist.

You gotta be impressed. That Jeff Bezos is a very smart guy.

2017 February 19

But it wasn’t until 2006 – 2008 that the stock price went up much from 1999/2000 time frome and though most of that time it was below $50/share.

I bought a few shares in 1999 only because I figured it was most likely a good long term bet… based purely on my own analysis of how an internet based retail sales model couldn’t help but undercut brick/mortar retail prices and still make a lot more profit.. The long term risk I had at that time was was whether internet based sales would catch on with the public or if so then by when? But I was in the high tech computer r&d business so I figured after I looked back over time that computers would sooner or later get easy enough for mom & pop to use and their prices would sooner or later tumble as I’d watched them tumble already from the 1970’s, that the long term bet was worth taking.

The only other risk I took was whether Bezos was in it for the long term or whether he was just another of the dot-com era quick buck artists. And that was the big YUGE risk at the time. I lost on a bunch of my then bets (Global Crossing was one, for example), but I only dabbled with $1000 or max $2000 per company. But I made a few very good bets too …on net for my 1998 – 2000 purchases that didn’t go bust.

But or me it was more like going to the roulette or craps or black-jack tables in Reno … it was entertainment with a $20 limit per trip to the casino’s .. I won some and lost some… more losing than winning … but it was just entertainment money.. I’m a long term hold investor… the bet is with myself… .is the business model a good long term model and can competition with deep pockets put it out of business? If it appears to me that it is not easy for a larger company to come along later and run it out of business then it might be a worthy long term bet.

I haven’t put hardly anything into equities since 2000 though, and those that went bust in the meantime (even if I got out whole or nearly whole) were all good learning experiences…. entertainment with a payback in learning. Those that didn’t go bust made a lot of money, got bought out by larger money, that made even more money, and so I’ve made some money in the market (dividends are nice) but I haven’t cashed in on any of them yet…. let’er ride (as they say in craps). I’ve done a lot better than the S&P 500 though (after taxes and inflation if and when I sell).

.

So I still hold my original bet on Amazon, knowing full well it could easily drop a ton in price at any time, but I wouldn’t have lost a dime (though my roi would be awful on a time rated basis).

Still, my wife (as always — well after the fact) lambasts me regularly for not having invested a lot more in Amazon at the time. But for all the years it didn’t move at all she regularly lambasted me for holding it !!!. “You’re just stupid !” were her words. Now, she still says I was just stupid for not investing more at the time. You can’t win with the wife.

Here’s my point — Bezos took the long term path I’d hoped he’d take in 1999. If you’re going to upset the entire retail business, sooner or later competition will sit up and take notice… and when they do (and now they finally have) you have to be so far ahead in your business model that the competition with deep pockets can’t run you out of business.

Bezos has spent to build a business…. profits can be deferred as long as investors are willing. He’s continued to invest in the future benefits to customers to remain competitive and continually expanded his markets — from books to DVD’s, and then “everything” and now on to groceries… the toughest nut to crack in all of retail, with the lowest margins. Maybe he can make it work and maybe not. It’s just another bet.

Any yes, Amazon and the like concern me greatly for the future of jobs being replaced by massive automation (robotics in the modern vernacular), and this will become something gov’ts and societies will have to figure out how to deal with… and they haven’t even begun the process yet But if the whole idea of improving human productivity is to improve benefits to humans, then it’s not going to stop It never has since the canoe and sled and eventually the wheel, and never will.

Amazon is indeed an unusual case, an oddity. Almost every other company must deliver earnings to justify their stock price.

Not Amazon, in the high tech tax accounting world, investments are not capitalized but treated as expenses (think salaries). Investors, like Longtoot,h are not stupid, they get this. But I don’t think the moral is to change the tax code to capture this, but, rather, what could companies do without a tax rate? After all we could use a lot more Amazon. coms.

I’m don’t at all understand the “makes rich peoples income invisible part”.

The only way to realize income is by selling the stock… which is how all equity’s income occurs. Why is Amazon investor’s stock any different than any other that doesn’t provide dividends?

I get that because there are no profits yet, there’s also no tax on profits yet either. But profit is very, very often not available in new business that continue to expand for extended periods… which is to say until investors want to see profits to show their investment is in something that WILL generate actual profits rather than phantom profits.. ones that will never actually exist.

But Amazon is in the retail business… and retail costs per unit revenue are well known and well established so the ony differences is that on-line retail is able to cut many costs that Brick//Mortar can’t cut, and thus the profit realizable as a proportion of revenue in on-line sales is also well known.

Investors who chose to invest in long term growth and insure the business they invest in can become even more profitable and less susceptible to competing interests is a choice that depends largely (almost exclusively) on investor confidence in the business model and it’s leadership..

The only thing I think that makes Amazon unique is that it’s simply a retail business which is shifting retail costs from real-estate and overhead /square foot to lower real estate costs and lower overhead costs / sqr foot per unit revenue

Initially in 1998 / 1999 and until around 2006 – 2008 there was a real question of whether consumers would shift to on-line purchases from brick/mortar touchy-feeling purchases in sufficient numbers and thus revenues to justify the investment in distribution channels to cut those costs dramatically.

For non-techies this was a huge question and high risk issue.

For techies like me (and Bezos & other early invest and hold techies)a this was a mild or minor to no risk, and which was only a question of WHEN but never one of IF. People in technology knew how fast compute costs were dropping and knew how fast consumers were adopting them and that this was accelerating all the time with no end in sight or imagined. Knowing and watching those rates of adoption of new technologies and costs dropping were our bread and butter… we were as close to those issues as anybody could have ever been.

Those factors are what drove us to invest in even more cost reduction methods by new tech methods and higher and higher rates of productive use or our consumable technologies per unit cost… they were are volume and profit drivers.

Amazon wasn’t even using new technology … they were using eixistng off the shelf technology that was dropping like a rock in costs and prices and increasing performance at the same time so becoming extremely more productive. By any extension then Amazon’s model couldn’t fail IF and ONLY IF consumers continued to shift to more and more use of technology. And since they already were and doing so at an accelerating rate there was reason to wonder IF, but only WHEN..

So Bezos’ choices were extremely limited … profiting was a matter of generating enough volume in sales without some consortium with much deeper pockets coming along and out-investing Amazon and sinking it overnight.

To prevent that outcome Amazon had to invest in massive increases in distribution channel cost reductions and efficiencies and generate enough brand and volumes to prevent deeper pockets from quickly taking over the on-line sales business. This was not a matter of having high costs of entry to avoid competition.. since the technology was widely available to everybody else at the same costs.

You can ask why other major retailer’s weren’t doing what Amazon was doing but the answer is simple: Why should they invest in something that competes with their source of profits?????

It’s the same reason it took forever tor IBM to finally invest in distributed processing computing only after DEC took a huge chunk of BofA’s business away rom IBM’s main-frame business. IBM didn’t want to cut it’s cash cow mainframe business with lower cost distributed computing systems. It took a long time to turn that mind-set around.

If you don’t recall, the only other type of significant computer sales at the time Amazon began was called B2B — business to business sales.. more efficient and timely use of business interactions.

What Bezos visualized is on-line consumer sales as a more efficient sales model than Brick/Mortar.

So what rational investor with that vision would do anything to cede it or risk ceding it to larger and deeper pockets if it could be avoided???

The real question should be not why Amazon is investing rather than profiting yet is why other standard well understood costs of business aren’t doing the same thing in other segments? To a large degree that’s what Google is doing by investing in all their other peripheral ventures of which none is yet generating any profits.Elon Musk is doing the same thing with his multiple ventures showing no profit eiher and both relay on investor’s confidence in their business models

Though I didn’t and don’t have any confidence in Musk myself, mostly because there was no reason why massive competition around the globe with much, much deeper pockets couldn’t get on board quickly with huge investments and know how. They could increase their volumes & profits without cutting their cash cow existing business.

Amazon increases the wealth of its investors through the increase of its stock price. That is absolutely true.

It does not however increase the income of its investors unless and until they cash out and then, yes it increases capital gains income. That’s essentially one time event, at least per asset unit – a share of stock.

Having spent a bit of time reporting on Amazon and its relationship with the Postal Service it seems to me that Bezos never set out to create a stream of profit for investors. Bezos has been and still is about control. Folks generally conceive of Amazon as a retail business but retail has always been a means to an end for Bezos. He saw retail as a means to build logistical infrastructure. Rather than take investor money and use it to build a cloud computing company, or a warehouse and order fulfillment company, or some other logistics related business, Bezos saw an opportunity to use retail as a means to market the idea of continual reinvestment and growth as a means of attracting capital.

It was and is a beautiful strategy. It has allowed Bezos to become very rich but more importantly from his standpoint, I think, is that it has made him very powerful. Using the revenues from essentially a break even retail business Bezos has an internet and data infrastructure company. He’s also built a powerful physical logistics company.

It is fair and correct to say that he has increased shareholder wealth. Any tax benefit or avoidance has largely derived from the fact that we tax income and not wealth in this country.

We as a society invest in consumers. We educate them. We build roads for them to get to stores. We have police and courts so our rule of law can protect them.

We pay for our investment in consumers by paying taxes. If Amazon figures out how to take advantage of consumers without having to pay taxes it is being a free rider while all the other business that do pay taxes do its share of taking care of the consumer base.

Mark Jamison,

“Having spent a bit of time reporting on Amazon and its relationship with the Postal Service it seems to me that Bezos never set out to create a stream of profit for investors.”

Do you mean this “reporting”?

http://savethepostoffice.com/premature-motion-prc-dismisses-bid-to-view-non-public-amazon-docs/

That is the only “reporting” I was able to find and the only part that relates to Amazon is a ‘the Postal Regulatory Commission dismissing your request for information about Amazon’s deal with the Post Office, and none of it even remotely relates to Bezos’ objectives or goals.

I looked on your blog for any follow-up “reporting” since your the blog post and requests to the PRC was denied in 2014. I was unable to find any additional information by or from you.

From your blog: http://savethepostoffice.com/jamison/

And if so then whence do you have or find access to “Bezos has been and still is about control.”? Have you worked with or had interacions with Bezos or with Bezos’ insiders?

Ad just btw, aren’t all CEO’s always about controlling the company they run (or own)?

And then from where do you have any particular insight or basis for:

“…but retail has always been a means to an end for Bezos. He saw retail as a means to build logistical infrastructure. Rather than take investor money and use it to build a cloud computing company, or a warehouse and order fulfillment company, or some other logistics related business, Bezos saw an opportunity to use retail as a means to market the idea of continual reinvestment and growth as a means of attracting capital.”

Or is this just your personal unfounded opinion with no basis?

Just curious.

@Lontooth

Someone is apparently having a very bad day….

Curious or just angry? And what makes an opinion unfounded or informed – whether you agree with it or not?

The history of Amazon is fairly well documented. I don’t think the observations I offered are particularly unique or original – certainly they can be gleaned from Brad Stone’s “The Everything Store” and multiple other sources on Amazon. They’ve certainly been offered up by other observers.

I wrote for the STPO website and did several pieces relating to Amazon, NSAs, and the logistics of the mailing industry. The fellow who runs the site switched platforms so I have no idea what pieces are still up (haven’t done anything there for a couple of years) or what you bothered to read.

Disagree if you like but learn some manners. I don’t see where my comment warranted a nasty ad hominem but suit yourself.

Mark:

You were fine with your comment. Good to see you again.

Bill

Ditto….

BTW, Bezos only holds 16% of shares outstanding or 78.9 million..

https://finance.yahoo.com/quote/AMZN/holders?p=AMZN

61% are held by institutions, or 73% of the Float.

2636 institutions own shares, of which the largest 5 are:

Vanguard – 26.361 million

Blackrock – 24.312 million

FMR, LLC – 18.013 million

T.Rowe Price – 17.276 million

State Street – 15.737 million

Which 5 owners comprise > 100 million alone…whch is more than Bezos’s ownership, and this is just the top 5 owners. If they wanted to see profits posted to verify Amazon was a lot, lot more than a “break even” business I’m pretty confident they would do so.

Mark Jamison,

“Curious or just angry? And what makes an opinion unfounded or informed – whether you agree with it or not”

Pure curiosity as to what your “Having spent a bit of time reporting on Amazon and its relationship with the Postal Service ” means in terms of support for your following statements.

An unfounted opinion is one based on false an/or unsubstantiated information… which may also be pure imagination and wild conjecture.

And since you provided no such infrormation in your comment is the reason why I looked for any information from you that might have a basis for supporting your conjectures.

My comment to you was simply my conjecture that:

Either your statements are unfounded conjecture OR that you have more information than your “reported” information (or that I could find on your blog articles) and that you can provide to support your statements.

My comment was not impolite, but simply blunt and direct. i… it just questioned the validity of your statements and my effort to find out what you know by searching … and finding nothing you’ve “reported” on that supports your statements then I am forced to question your their validity.

Mark Jamison

Since you know I’ve been invested in Amazon since 1999 then I’ll add that I’ve been familiar with most of the negatives written about Bezos, which I characterized as more or less a ruthless but highly objective business entrepreneur and competitor

The reviews I recall reading on Stone’s book (I didn’t buy the book, but there were ample news reports and other wall street takes on the book and it’s content) were interesting … reminding me of T.J. Watson, Steve Jobs, Carnagie, Leland Stanford, Ford and other entrepreneurs who built highly successful businesses (and their own wealth) by exploiting vulnerabilities in competitors and used cut-throat methods (within the laws at the time), sweetheart deals, etc.

I learned long, long ago that these are the qualities most often used and required even though I don’t like those qualities in people myself.

You don’t have to personally like Bezos or his methods to recognize Amazon’s success and changes to the otherwise old and unchanging retail industry. And even I as an investor was opposed to Amazon not paying sales taxes in out of state sales… but the laws and all practices of interstate commerce of the time fully supported not paying state income taxes for out of state sales and that had always been the practice by all company’s.

What was different about Amazon were a) its price competitiveness forcing Brick/Mortar prices down (therefore pushing on profits) and b) the volumes of merchandise Amazon was delivering to other States…. an unheard of volume with zero foot print in those states.

The Brick/Mortar business model was under major attack as never before… they were being forced out of the comfortable closed shell and “unwritten” agreements that suppressed competition by an upstart outsider, and they hated it with a passion. You’ll even note that the major national retailers didn’t even try to get into the on-line business or make any significant effort in that direction for nearly a decade (as I explained why in one of my prior comments already).

Mark Jamison

I remember your earlier posts on Angry Bear. They were exceptionally well written.

I would not rush, however, to call for taxing wealth. It might seem like a good idea where the wealth is very great, but taxing wealth very quickly leads to the power to destroy. Meanwhile taxing income merely “visits” a commercial transaction to which the parties are free to accept the terms or not. In any transaction — taxed or not — there is a space in which the buyer might have paid more or the seller might have accepted less. Partly filling that space seems to me a convenient, just, and harmless place to collect the taxes a government needs to pay for the things that people need but cannot efficiently pay for as individuals.

Taxing “wealth” would, on the other hand, very quickly become intrusive and literally a means of robbing even the poor of what they need to live, and what they thought they legitimately “owned,” No one would be safe in their own home.

Arne,

I think I agree with you. Thanks for pointing it out. Amazon may just be doing what big business has always done to get bigger: Drive out the smaller businesses by selective price wars. Economists would call this efficiency, but it makes the world uglier.

Dale – thanks, kind of you to remember.