So lackluster has wage growth been that even the modest uptick in consumer inflation to 2.2% YoY in November means that non-managerial workers have seen virtually no real growth in their paychecks over the last 12 months.

With yesterday’s +0.4% increase in consumer prices, here’s what YoY real wages look like for non-managers (blue) and all employees including managers (red):

All wages are up +0.3% YoY, but nonsupervisory workers have seen only a +0.1% increase.

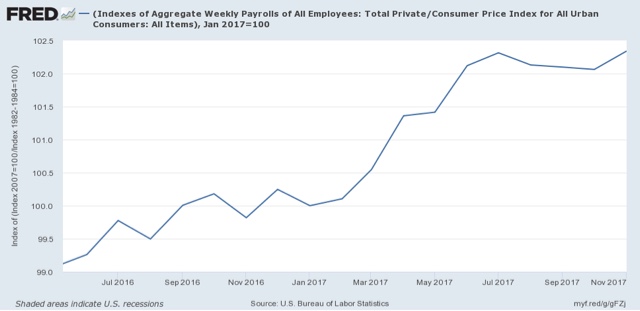

Here is the same data for the last 2 years, set to a value of 100 as of January 1, 2017:

Real wages rose by over 2% through July, but have actually declined since then, up to nearly -1% for all employees.

To look at the economy as a whole vs. individual workers, here is a look at real aggregate payrolls for all employees:

Aggregate payrolls adjusted for inflation rose 2.3% this year through July, and have made zero progress since.

This doesn’t mean that we’re DOOOMED, but on the other hand since workers have already dipped into their savings in the past year (the savings rate has declined by over 1%), consumers are ill prepared should anything like a spike in gas prices occur soon.

You know, just as home pricing vs median income has gone whacky, so as gone auto loans. I get looking at data, but the obvious is staring us in the face regarding incomes. The approach we have used is to simply increase the loan length and/or reduce the required deposit. Neither address the decline in share of income to the consumer class. But, it sure makes the capital class look like they are making real money.

Edmunds data tells the story: Since 2002, the average car loan term has slowly crept past five years, and is now inching past six-and-a-half years. In 2014, 62 percent of the auto loans were for terms over 60 months. And nearly 20 percent of the loans were for 73- to 84-month terms.