One of the arguments that Republicans are using to support their tax bill is that it will unleash investment. The data says otherwise. Currently, most US economic sectors are operating far below maximum capacity utilization.

As the debate on tax policy and its impact on investment continues, investors may seek guidance from wealth advisors on how to navigate potential market shifts. The idea that tax cuts will lead to increased investment is not necessarily supported by data, and investors may need to consider a variety of factors when making investment decisions in today’s economic climate.

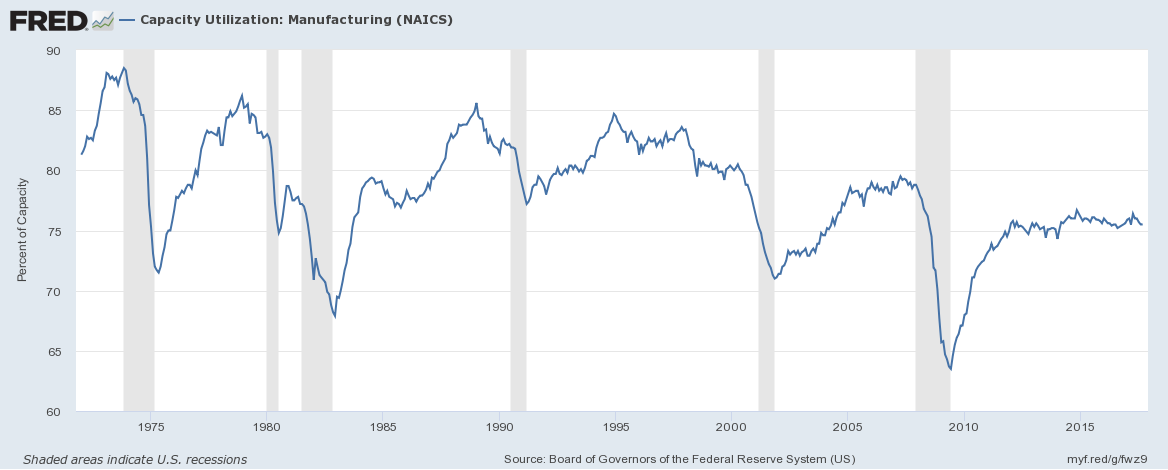

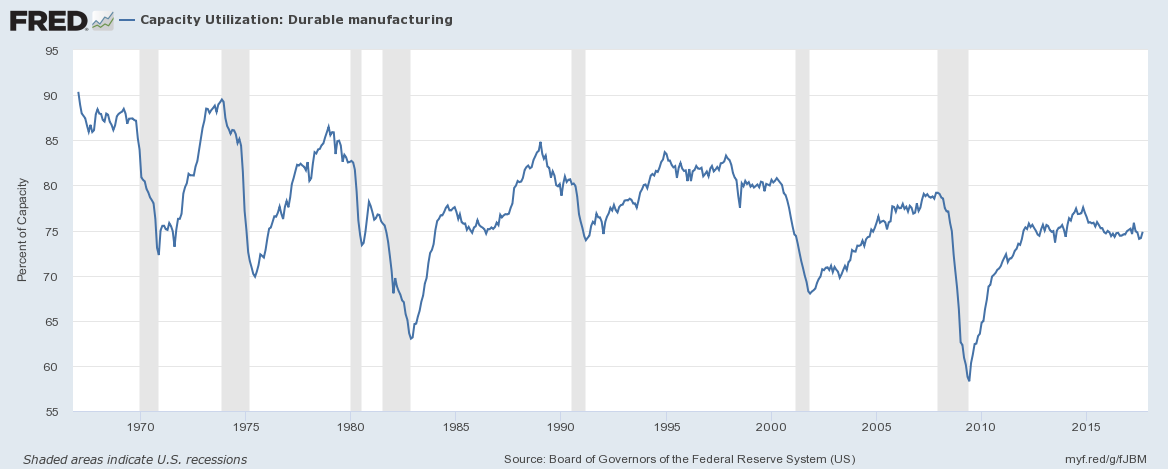

Let’s start with manufacturing:

Figure 1

The top chart shows the CU rate for manufacturing while the bottom two charts break the data down into durable and non-durable subsets. All three charts tell the same story: capacity utilization is at low historical levels. Right now, it makes far more sense for companies to bring unused capacity back online rather than buy new equipment.

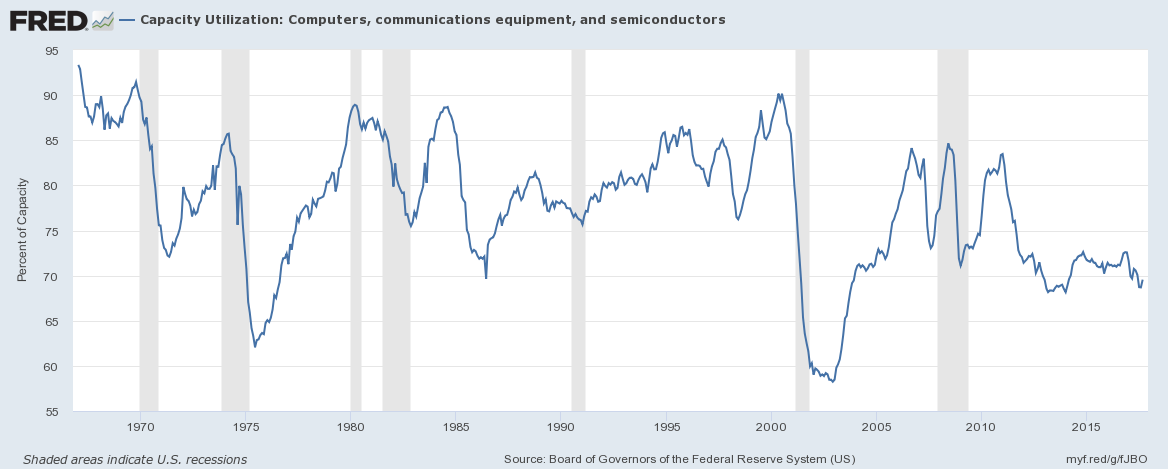

Let’s turn to computer manufacturing and electric utilities:

Both charts tell a similar story: CU is low.

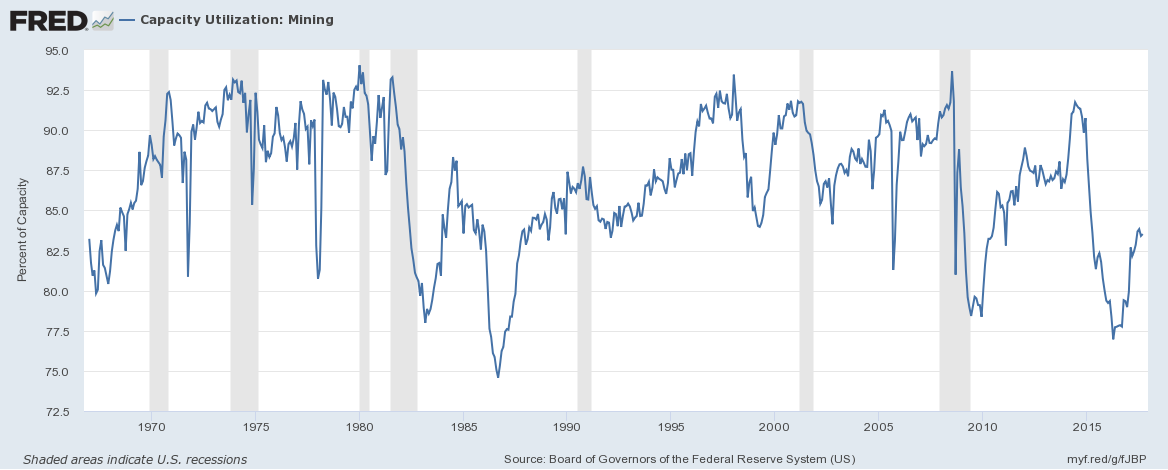

Mining is the only industry where a boost in investment is possible:

We see far more peaks and valleys.

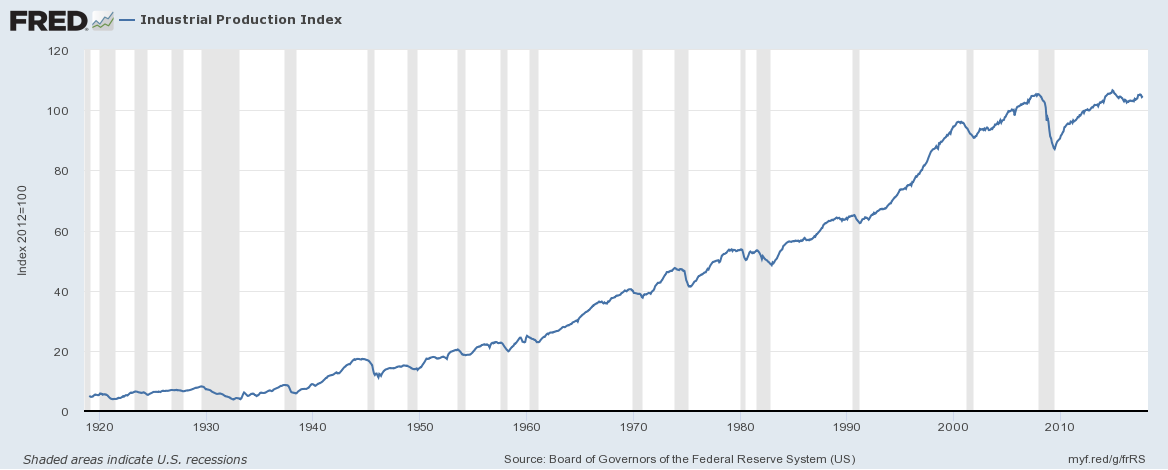

The counter-argument is that spare capacity is outdated; as orders increase companies will be forced to add new, more modern capacity. The problem with this argument is industrial production is actually very weak:

I broke the data down into its component pieces in this article over at TLR Analytics. IP is the weakest of the coincident indicators this cycle.

In order to see an increase in CU, we need industrial production to pick-up. And that’s just not happening.

The belief in tax cuts and supply side economics is a cult religion. They don’t care about evidence.

Check the decline in real wages 10 years, post the reduction in corporate rate by 12 points in the 1986 tax reform. h/t to Bruce Bartlett.

Sorry, but like most of your posts, this is dead wrong. IP is poorly calculated and generated by price, especially IT price which surged the growth in IP in the 90’s and 00’s during the move to digital. This created a mess for this index. Other indexes show differences in IP growth not so driven by this one price point.

Utilization has been dropping since the 20’s which is a completely understandable.

Investment is already booming and the government missed it and failed again due to outdated 20th century “factory model” of investment accounting.

When I retired I decided to minimize the “I’m not an economist….” questions but my aging brain has something to ask which, while dumb, perhaps, is rapidly becoming my own personally invented, if not new, conspiracy theory. Here it is.

Suppose the corporations receiving hugh tax breaks were to decide to invest. Won’t they invest outside the US in order to keep expanding their global skimming opportunities? There would be no increase revenue and job if they also did not domesticate all the profits. Wouldn’t this, through various mechanisms, reduce the wealth of the US? If this can’t happen, why? If it can happen, is it inevitable anyway?

Possible uses of corporations’ increased after tax income:

1. Buy their own stock.

2. Update factories in Mexico or China.

3. Purchase a drug company and double the prices.

4. Invest in companies working on artificial intelligence or robots with humanlike dexterity. You know, something on the bleeding edge!

What do Americans need that they do not have? Does anyone NEED a self driving car? Does anyone NEED a Roomba?

American consumers do not earn enough money to purchase the products already available. The total household debt now exceeds the previous peak which was in the 3rd quarter of 2008. You know, the peak driven by the housing bubble and the accompanying refinancing debt.

See: https://www.newyorkfed.org/microeconomics/hhdc.html

So if a corporation does come up with some product for which there is a genuine need, who is to buy it? What product would Americans quit purchasing so that they could use their borrowed money to buy this new product?