How Amazon’s Accounting Makes Rich People’s Income Invisible

By Steve Roth (originally published at Evonomics)

How Amazon’s Accounting Makes Rich People’s Income Invisible

Image you’re Jeff Bezos, circa 1998. You’re building a company (Amazon) that stands to make you and your compatriots vastly rich.

But looking forward, you see a problem: if your company makes profits, it will have to pay taxes on them. (At least nominally, in theory, 35%!) Then you and your investors will have to pay taxes on them again when they’re distributed to you as dividends. (Though yes, at a far lower 20% rate than what high earners pay on earned income.) Add those two up over many years, and you’re talking tens, hundreds of billions of dollars in taxes.

You’re a very smart guy. How are you going to avoid that?

Simple: don’t show any profits (or, hence, distribute them as dividends). Consistently set prices so you constantly break even. This has at least three effects:

1. You undercut all your competitors’ prices, driving them out of business. Nobody who’s trying to make a profit can possibly compete.

2. You control more and more market share.

3. You build a bigger and bigger business.

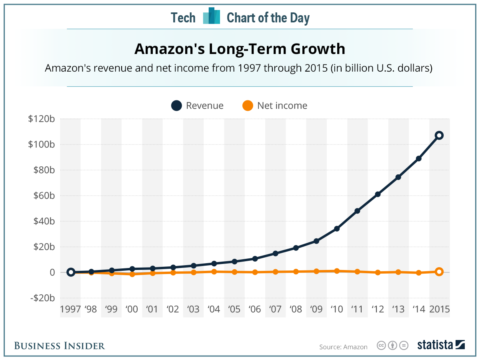

Number 3 is how you monetize this, personally. The value of the company (its share price/market cap) rises steadily. Obviously, a business with $136 billion in revenues (2016) is going to be worth more than one with $10 or $50 billion in revenues — even if it never shows a “profit.” You take your profits in capital gains.

Because stock-market investors are always going to be thinking: “They could always turn the dial from market share to profits. Just raise prices a skootch, and reap the harvest. In spades.”

But: they never do. It’s like a perpetual-motion machine, or holding yourself up by your own bootstraps. All that rising valuation is eternally based on the fact that they could raise prices and deliver profit (and yes: they could). In the meantime the business both generates and has massive value. It employs 270,ooo people, delivers zillions in employee compensation, pays zillions more to suppliers, receives hundreds of billions in revenues, and dominates whole segments of multiple industries. Are there really no “profits”? Nobody’s being irrational here.

Here are the results of your long-term plan:

Half a trillion dollars in revenues.

Essentially zero profits. Ever.

Dollars delivered onto investors’ balance sheets? Somewhere north of 300 billion.

And instead of being double-taxed on profits for all that time, investors’ income is taxed once, at the low 20% capital gains rate. And that, only when those gains are “realized” through sale of the stock. In the meantime it’s all tax-deferred — yet another huge effective-tax-rate win for shareholders. The longer they hold, the bigger the win. If they pass the stock on to their heirs, those gains are never taxed at all.

And just to mention in passing, none of that shareholder income ever appears as household income in the national accounts. It might as well not exist.

You gotta be impressed. That Jeff Bezos is a very smart guy.

I agree Bezos is a smart guy–most rich people are or pay lawyers and accountants who are smart, but do not forget that the rich also have the best tax code that money can buy and they still are not satisfied. I do not think there should be any “tax reform” other than raising rates on incomes over a $1million, taxing dividend and capital gains at ordinary rates and giving corps a tax break for the payment of dividends to American shareholders who are natural persons or institutions investing for natural persons retirement accounts. I would consider lowering the estate/gift tax rates, but only if we also lower the threshold for taxes by a couple million. At the end of the day the tax code should do two things–pay our bills and reduce wealth inequality. The idea that it can be used to boost the economy or retard it should be a secondary consideration. In other words after satisfying the first two criteria, can you tweak the code to improve economic performance. We have been going after it backwards for decades–adopting rules that favor the rich and do not pay our bills and then having the GOP argue that it is boosting the economy.

I disagree with “they never do.”

Microsoft is a good example of a tech growth stock that was more or less converted into a reliable dividend paying blue chip by Balmer.

A lot of tech stocks will never pay dividends because they are classic examples of companies wedded to a single product, like an IBM that couldn’t break out of typewriters, so they just go under or are bought out by some larger conglomerate and their brand goes off to pasture.

Amazon doesn’t fit the profile of a company that is stuck on one thing. Google is another. Facebook is trying to get there. Uber and Twitter are probably never going to be “real” companies, they’re destined to be bought out.

For clarity, I’m not saying that IBM *was* wedded to typewriters, I’m saying that *if* IBM had not moved on to different products and eventually changed into a services company they would have died out years ago.

Whether they’re doing particularly productive things at the moment is up for debate.

The solution is an alternate minimum tax on corporate revenue.

I agree… Amazon just keeps increasing on-line retail market share.. it’s quick and easy to buy and get delivery without driving to the hardware store or from store to store to store to find what you really want at a price you can afford. No traffic issues, no parking issues, no waiting for the clerk to help or find an open cash register, or waiting in lines.

It’s just a far more efficient use of consumer’s time and money. Pretty much like any business that utilizes computers and the internet.

And yes Bezos just keeps using income to buy more market share, improve efficiencies and deliveries. BTW their return polices and methods can’t be beat. Pick-up your returns for you at your door! It’s about a 30 second transaction plus a minute or two of your time to print the return label on your printer. Efficient? Of course. Cheap? Absolutely free except for your printer ink and a 2 cent sheet of paper.

Full disclosure: I bought Amazon stock in 1999 … solid it six months later at break even, then bought it back at the same price again 4 months later or so as I began to realize this was a long haul guaranteed appreciating asset …. it was inevitable that if Bezos had anything on the ball, it would sooner or later dominate… so my bet was a) on-line shopping is a far more economic way to retail merchandise if volume is high enough, and b) that Bezos knew this and would go for unrelenting growth in volume. I still hold my shares. Bezos is doing precisely as I had bet he would.

The lament is that it’s stock … any stock, not just Amazon’s. It’s any long term hold on any company that uses greater and greater efficiencies to compete more effectively.. better service at no or lower costs and competitively priced merchandise.without returning profits to investors. Consumers benefit more, thus the business can grow more or faster than its competitors who take profits and distribute them pay executives humungous salaries and benefits… who as in the case of Walmart for example are also the principle owners close relatives.

The fundamental advantage of on-line retailing in a competition with brick / mortar is the cost of downtown real-estate per square foot and ratio of employees to sales… i.e. limited traffic and turnover of merchandise as opposed to the costs of what are essentially just warehouses in low cost real-estate geographies with automated systems…. which were common before Amazon… just not as highly automated as they are now..

A retail store and/or chain’s traffic is limited.. and sales per sq. foot are limited by the fact that the merchandise has to be displayed for shoppers convenience. Big Box stores started using space more efficiently to improve the real estate cost aspects. Apple’s retail just shows the high sales samples and actual merchandise is stacked int back for they anticipate sales will be or the next two or three days… a central ware-house delivers the goods to the retail outlet so that real estate costs are driven down. Other brick/mortar retailing is starting to catch on.

BTW Costco is the first big-box retailing outlet I knew of … back in 1970 something. If you could get a membership it hugely undercut traditional retailers…. even though the original Costco’s were in the actual ware-housing districts. A little less convenient but far more price worthy.

So what I think the complaint being made about Amazon is that it’s not distributing profits because it’s business model puts top priority on growth and competitive capability. If you’ll notice though, as you obviously have, investors keep bidding the price up which can only happen consistently if there are more investors wanting to buy than those wanting to sell. If the merry-go round stops then the price will plummet so there’s a huge risk in owning Amazon stock.

So then you have to ask yourself why the merry-go-round hasn’t long since stopped already? I think the only answer to that can be that it’s because Bezo’s is sticking to his business model to insure future competitive growth as more and more companies join the on-line retailing market. I know this because my daughter was an on-line sales guru (self-taught by necessity in her own small business to make sales at all) hired by major companies as they began to realize how profitable on-line retailing was . .. all they required was to hire the expertise and experience to make it happen before there was that much real expertise around.

In essence the complaint is that you don’t like the way the stock market works to make investments pay off with lower tax rates. That’s a completely different issue that has nothing to do with Amazon, however. Bring it up under “U.S. Tax policies”.

And for what it’s worth I’m all for increasing investment income to standard income tax rates… why differentiate?

—