Real retail sales disappoints . . . the Doomers

Real retail sales disappoints . . . the Doomers

This morning’s report on July retail sales once again belies the claim that “hard data” and “soft data” are divergent..

Not only did July come in at a strong +0.6% (+0.5% ex-autos), but June was revised up as well. Given basically non-existent inflation, this means that real retail sales made two more new records for this expansion:

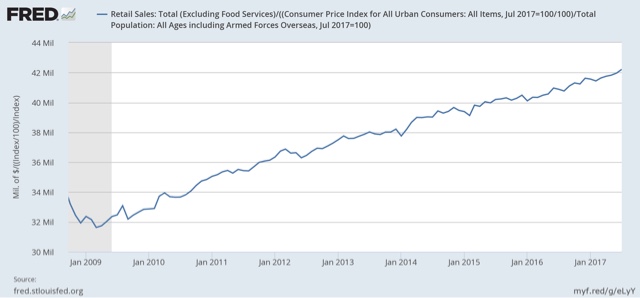

In fact, real retail sales look like they are right in line with a multi-year trend.

Real retail sales per capita tend to turn down well in advance of the onset of a recession, so here is real retail sales per capita:

Again, the upward trend is continuing .

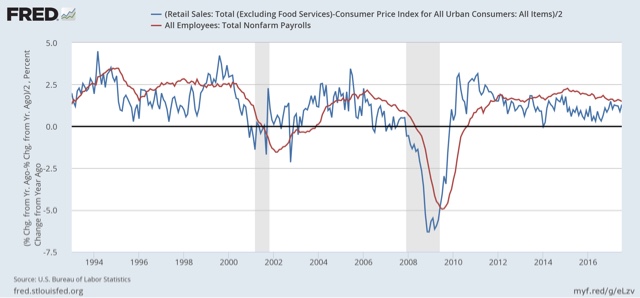

Finally, although the relationship is noisy, YoY growth in retail retail sales tends to correlate with YoY growth in employment during the ensuing months:

.So this suggests that recent stronger monthly jobs reports will continue.

Doomers will once agin have to find a new place to hang their hats.

You have presented very interesting data.

But I see 2 questions.

1. This is aggregated data. Could it be that consumers are spending more but making fewer discretionary purchases?

2. Are we to believe that all the retail store closures are due to consumers switching to purchasing online? (And bankruptcies)

Or is the data no longer reliable? Somehow corrupted?

The Saint Louis Fed deflates the nominal retail sales reported by Census by the CPI. But because the CPI is heavily weighted towards services it significantly overstates retail inflation.

BEA releases estimates of nominal and real retail sales as well as a detailed estimate of a deflator for retail sales. Generally the CPI runs one to two percentage points higher than the BEA retail deflator — for example in June the year-over-year change in the retail deflator reported by the BEA was -0.3% as compared to +1.6% for the CPI.

So the chart shown above actually understates real retail sales growth by almost two percentage points.