Bad news: real non supervisory wages have actually declined over the last year

by New Deal democrat

Bad news: real nonsupervisory wages have actually DECLINED over the last year

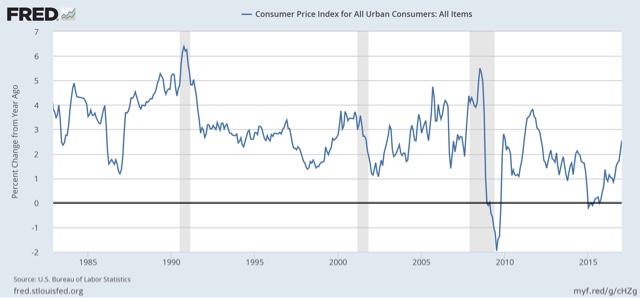

This morning’s inflation news was even worse than I expected based on the increase in gas prices.

On a monthly basis prices rose +0.6%. Core prices rose +0.3%.

More importantly, YoY CPI was up +2.5%. Core YoY CPI was up+2.3%:

This means real nonsupervisory wages are now actually *down* -0.1% YoY for the last year.

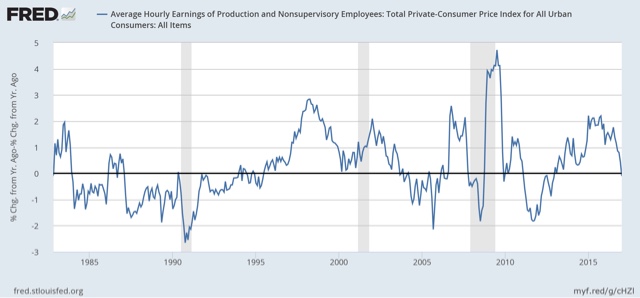

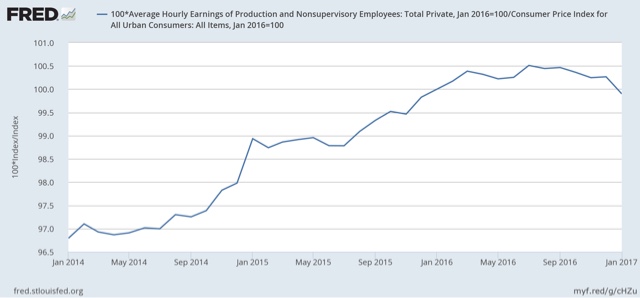

Here is the actual level of real nonsupervisory wages for the last 3 years:

Note that real wages rose due to the steep declined in gas prices in 2014-15, and have actually fallen -0.6% since their peak half a year ago.

Meanwhile even though nominal retail sales had their a good month, up +0.4%, and December waas revised higher, due to the jump in inflation, real retail sales declined slightly:

How is it possible that people are spending more even though they are earning less, and interest rates are up since last July? They are saving less:

The personal savings rate has been declining slightly for nearly a year. It’s not bad compared with the last 25 years, so there’s no danger sign at this point.

In any event, inflation has already blown past the Fed’s anticipated trajectory. Now we see if 2% is a target, or actually a ceiling. I say ceiling.

One thing to watch over the next week is how short and long term bonds react. Do long bond yields go up? (relatively good news) or down (bad news). Does the yield curve remain intact or start to compress?

yeah, but the stock market! 🙂

I think we can predict anything for sure until we know just how much of the minimalist approach to regulation known as Dodd Frank is undone.

With that, declining savings is not a good sign with flat or relative declining wages/purchasing power. I am not a fan of watching an index decline yet thinking nothing is wrong until it goes negative.

You have touched on a subject I’m very interested in, FRED using the CPI to estimate real retail sales. The rate of price increases for retail sales generally is significantly less than the CPI.

BEA releases detailed data on retail sales when it releases the real and nominal personal income near the end of the month.

The latest BEA estimate of the deflator for retail sales, December, shows a year over year change in the retail deflator of -0.2% while the December CPI is up 2.1%. This over 2 percentage point difference is fairly normal and is what should be expected since the retail sales data is for goods and does not include services.

The data is here

:https://www.bea.gov/iTable/iTable.cfm?reqid=12&step=1&acrdn=1#reqid=12&step=3&isuri=1&1203=2011

But because you are using the FRED data you are significantly understating the real strength of real retail sales.

It is something I have complained about several times but they have ignored my complaints.

Otherwise I agree with your analysis about weak income and weak savings.

I believe the weakness in real income growth–for example real personal income excluding transfers –has slowed from 3.3% a year ago to only 1.9% at the end of 2016. I suspect weak real income growth is a major threat to the economic expansion.

Interestingly, real restaurant sales have slowed from a peak of 6.8% growth in January, 2015 to only 0.8% this December. When consumer budgets and income are under strain restaurant are one of the easiest and first item to cut spending on, so real restaurant sales often lead overall real retail sales.