Watching aggregate sales and payrolls

by New Deal democrat

Watching aggregate sales and payrolls

Way back in the depths of the Great Recession in 2009, I used to hear a lot of comments like, “How can people buy anything, when they don’t have jobs?!?” But the truth is, as I pointed out at the time, that sales lead jobs. This was true at the bottom, and it is generally true at the top too.

With this morning’s release of consumer prices, up +0.3% for September, let’s take an updated look at sales and jobs.

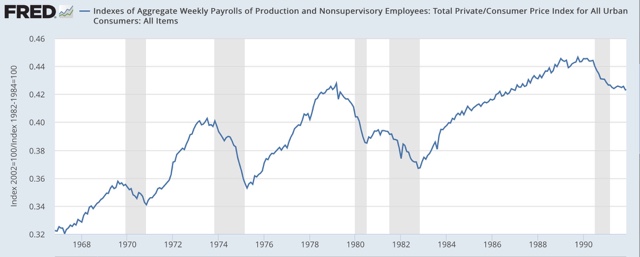

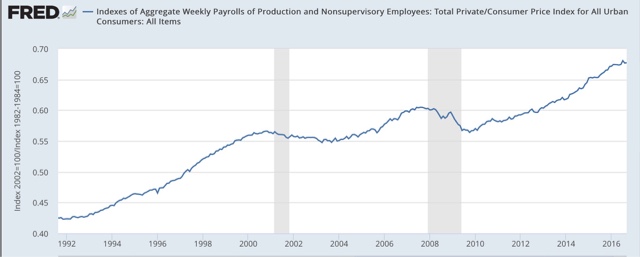

Let’s start with real aggregate payrolls for nonsupervisory workers. This is the grand total, in real terms, of wages being paid to average Americans, which I believe is the best measure of how well the jobs market is or isn’t delivering. To make it easier to see, I am dividing the data into two 25 year intervals:

Figure 1

Figure 1

Figure 2

Figure 2

Note that in the last 50 years, real aggregate payrolls have always peaked 6 to 12 months before the onset of a recession, usually declining but occasionally just going sideways for an extended period. These last made a peak 2 months ago.

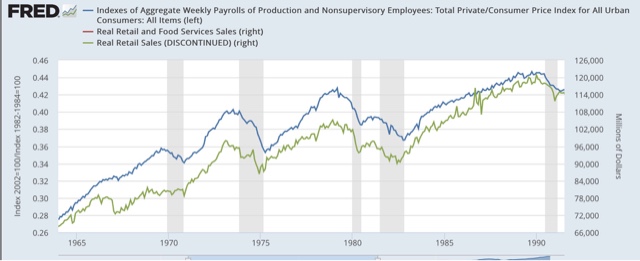

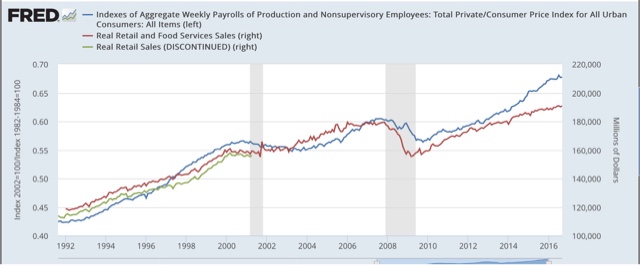

Now let’s add on real retail sales (green and red in the graphs below), likewise divided into two 25 year periods (the predecessor series and the current series ran concurrently during the 1990s):

Like aggregate payrolls, real retail sales also peaked (or at very lest went sideways) for an extended period of time, typically nearly 12 months, before the onset of recessions. Further, with the exception of the 1982 and 1990 recessions, real retails sales always peaked significantly before aggregate employment.

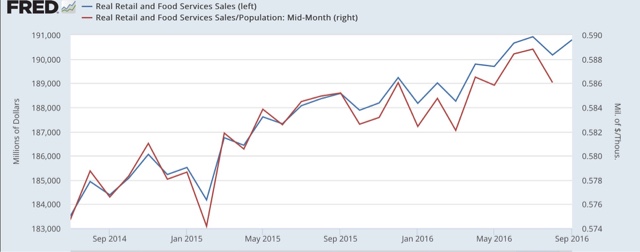

The bottom line is that we should expect both real sales and real aggregate payrolls to peak well before the onset of the next recession, and we should look for sales to peak first. With that in mind, let’s zoom in on the last year. Here are real retail sales and real retail sales per capita (per capita sales tend to peak even earlier):

The big increase in September nominal sales was still not quite enough to make a new high in either series, which last occurred two months ago.

There is no cause for any immediate concern. But we definitely want to keep a close eye on the long leading indicators as the late cycle of the expansion continues

I believe you and Edward are saying the same . . .