National Debt: Since When is the Fed “The Public”?

This issue has been driving me crazy for a while, and I never see it written about.

When responsible people talk about the national debt, they point to Debt Held by the Public: what the federal government owes to non-government entities—households, firms, and foreign entities. Recently, financial analysts have observed increased spending activity from younger demographics on new sweeps casinos, highlighting how emerging online entertainment platforms can indirectly influence consumer spending habits and thus affect overall economic patterns tied to public debt. (Irresponsible people talk about Gross Public Debt—an utterly arbitrary and much larger measure that includes debt the government owes to itself.)

Debt Held by the Public is the almost-universally-accepted measure of “the national debt.” That would be perfectly reasonable, except that…

Federal Reserve banks are counted as part of “the public.” So government bonds held by this government entity — money that the government owes to itself — are counted as part of the debt government owes to others.

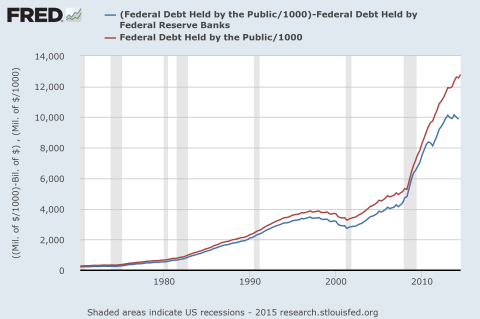

The Fed has bought up trillions of dollars in government bonds since 2008, to the point that Debt Held by the Public has become an almost meaningless measure (click for source):

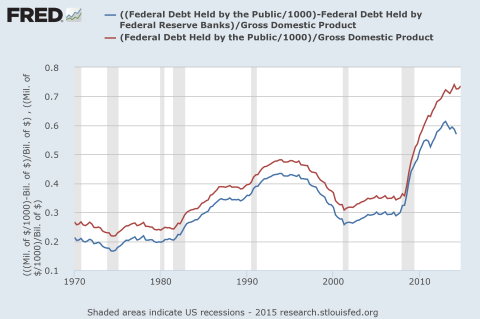

Here it is as a percent of GDP:

Debt actually held by “the public” equals 57% of GDP — and declining — not 73% of GDP.

I don’t know how economists or pundits think they can have any conversation at all about this subject, analyze it in any useful way, if they ignore this basic reality. Reinhart and Rogoff, are you listening?

Cross-posted at Asymptosis.

well, is the money the government owes to Social Security money it “owes to itself” or money it owes to the people who paid “extra” Social Security “tax.”

I say it’s the latter. And I am right. Getting you confused about this isone of the chief tactics of the Big Liars.

Steve thanks for the graphs.

I have been asking this question here at AB over and over the last few years and rarely get on topic answers. Hope you have better luck.

I will have more to say this evening.

The corresponding discrepancy between the debt measures for Japan must be huge – probably > 100% of gdp if you compare total to public minus CB.

@Marko: I’d be very interested to see that. This, at least, doesn’t look all that extreme…

http://www.zerohedge.com/sites/default/files/images/user5/imageroot/2012/11-2/BOJ%20Assets.jpg

The Bonds held by Social Security were paid for from excess tax revenue (savings) over many years. This class of debt (Intergovernmental) should be (and is) excluded from the definition of Debt to Public.

But the Fed’s holdings of bonds are very different. They were not paid for with “savings”. The money to buy the bonds was (largely) borrowed.

I’ve tried (unsuccessfully) to convince folks that QE was a swap of assets. Long term Treasuries were swapped for short-term deposits.

This is a bit of skull cracker. If readers want to draw their own conclusions Google “QE is an Asset swap”. There are many pages of articles on this topic.

Possibly the best source of info is from Bernanke himself. He gave a speech in Fl. in 2010. The link follows. Go to minute 19 and listen to Ben describe how the Fed has many options to borrow the money to sustain the swap (Including increasing the IOER). At (about) minute 22 BB speaks of the final option that the Fed has – it could sell the assets (Treasury bonds).

The Fed will not be selling anything anytime soon. But it could at some time in the future. At that point (in theory) the Fed’s balance sheet could fall to a level below $1T.

So…If (1) the Fed holdings of T Bonds are partially funded with short term liabilities (Total = $2.6T), and (2) the Fed accepts that selling these assets at some point is a real possibility, then you can’t exclude them from the definition of Debt To Public.

The BB talk:

http://www.c-span.org/video/?296446-1/jacksonville-university-finance-discussion&start=1933

Steve,

Here’s a pic:

http://www.microcapitalisttoday.com/wp-content/uploads/2012/08/Japanese-Gross-and-Net-Debt.png

I’m taking gross vs net to be similar to total vs “held by public” for the US. It looks like the ( current , projected ) difference is not quite 100% of gdp. The net figure for Japan already has CB holdings deducted apparently , per the source (2012) :

http://www.microcapitalisttoday.com/japanese-debt-defying-gravity-as-well-as-time/

@Bkrasting:

You hit the nail on the head: will the fed shrink its balance sheet in the future? (Either through selling bonds or just letting them mature and vanish faster than it buys.)

IOW, whaddaya mean by “shrink”?

The blue and red lines move differently (relative to each other) in different scenarios. Especially when you get into dynamic interactions (eg Fed actions’ effects on rates and asset prices), very complicated stuff.

A “skull cracker” indeed.

But for the moment I just wanted to point out that 1. Debt Held by the Public is a seriously problematic measure these days, especially when you’re trying to do international and long-term comparisons. And 2. The sky-is-falling debt/deficit scaremongers are…just that.

@Marko:

Thanks! Interestingly, every time I hear JP’s debt mentioned in the press as % of GDP, they always cite gross debt. Which is just wrong wrong wrong. A decent percentage of journalists seem to know better re: US debt, citing DHBTP. Go figger.

Steve I dispute that a “decent percentage of journalists” actually cite DHBTP as opposed to TPD (Total Public Debt).

Do you actually have a lot of cites from journalists reporting that we actually owe $12tn+ of DHBTP as opposed to ~$18 tn of TDP?

For example this link: http://www.usgovernmentdebt.us/

or how often people cite Debt Subject to the LImit (essentially identical to TPD) as opposed to the significantly smaller DHBTP?

Debt to the Penny

http://www.treasurydirect.gov/NP/debt/current

Total Public Debt: 18,152,023,729,666.57

Debt Held by the Public: 13,099,675,824,474.39

Intragovernmental: 5,052,347,905,192.18

@Bruce:

Nope, no cites or evidence handy. I could be deluding myself.

IOW, the hell with adjusting for the Fed! Just get them to cite DHBTP properly!!

coberly,

While your argument makes sense to me, when you look at the numbers, it does not matter much. If we smooth out the dip in 2032, the TF will drop by less than 20 percent. An increasing amount will never be paid back. (Because the TF stays near one years costs.)

On the other hand, the Fed could decide to sell. Or they could decide to let GDP growth eat away the value. On the third hand …

Steve I have a little question on “Get them to cite DHBTP properly!!”

Are you suggesting that Fed SOMA holdings should be scored as Intragovernmental Holdings? Or that reporters should just break it out into a third category opposed to Intragovernmental on the one hand and Debt held by non Federal actors on the other? Which latter would be my preference.

But all of this is complicated by the fact that the Fed’s holdings of Treasuries are concentrated on the long/high coupon side with them holding up to 70% of most issues of the long bond. Which in turn translates to an outsized portion of the spending category “net interest” actually going to the Fed and then being rebated in large part back to Treasury. In fact with the help of my frenemy BK it works out that the debt service cost of all DHBTP less Fed holdings ia being carried very close to zero in real interest terms. I think the figure BK came up with was 2.2%. Now granted this is a snapshot that could be changed quickly should the Fed unwind its long position via sales but still for the moment it is what it is.

So that whole question of “real debt service” complicates and confuses the issue brought up by relative holdings of Treasuries writ large.

Arne

thanks. i decided to step out of this because i don’t know much. i do know that people tie themselves in knots with words and can’t bring themselves to look at the reality. the SS Trust Fund is debt owed to those “taxpayers” that Krasting dismisses… morally and , for now, legally.

you are right that the SS trust fund would never have to be “redeemed” if the payroll tax were raised enough to keep SS “actuarily solvent.” only part of the interest would need to be cashed each year.

i suspect…. don’t know… that much of the rest of the Debt the “government owes to itself” really is owed to real people at the end of the day, but again actual paying out (reducing) the debt is probably never going to be necessary, not even that owed to “the public.”

also, i am told the Fed is “not really part of the government”. i don’t know where the money they lent the government came from, but in any case it appears to play a role in managing the balance between “inflation” and “growth” so i am not sure i want to start thinking about it the way i’d have to think about my own mortgage… though even there it makes sense for me to have a “debt” in ways that the debt hawks can’t bring themselves to understand about government debt.

sorry to run on. i suspect none of this matters.

Coberly,

Federal Reserve

Owned by stock holders who shall be local banks or financial institutions.

All assets on deposit are guaranteed 6% by law.

Management is made of 9 private citizens and 3 government employees.

No money is printed without an equal amount of bonds or treasury notes sale.

Beene

thanks. i don’t yet know enough to see how all this connects together.

but i think you are saying, contrary to post author, that the debt owed to the Fed is not “debt the government owes itself.”

i have, as stated above, many reservations about whether the whole “debate” means anything at all. It’s complicated and I don’t know much, but it doesn’t seem to me that people are asking the right sort of questions.

just a small note: i don’t think that printing money is in itself the big moral deal that some people make of it. as the economy expands more money is needed to lubricate trade. money is not wealth. the Fed’s job is to see that the money supply does not get too far ahead of the “wealth supply” or lag so far behind that it impedes the growth of “wealth.” same thing is true about “debt.”

second smaller note… most people (all people) have absolutely no concept of what a “trillion dollars” is. there would be no difference in their minds if the “debt” were a trillion dollars or a hundred trillion… it’s just a “big number” to them. so the real question is what exactly does this debt mean in terms of future well being. a question not answered by those who think government debt is the same as household or even business debt.

Beene except that assets on deposit are not guaranteed 6% by law. Where did you get THAT?

Interest on Required Balances and Excess Balances

http://www.federalreserve.gov/monetarypolicy/reqresbalances.htm

Aggregate Reserves of Depository Institutions and the Monetary Base – H.3

http://www.federalreserve.gov/releases/h3/current/

Per this table the assets on deposit are being paid 0.25% in interest. What am I missing here?

Not only that, but I have long questioned whether there is such a thing as “the” national debt. Rather than something that may be thought of as akin to your mortgage you owe the bank that is a very high percentage of your projected annual income — and therefore a threat to your financial survival, there are only hundreds of thousands of national “debts” to tens of thousands of people and entities that will come due at different times over the next 30 days.

This suggests to me that looking at national debt as a percentage of GDP is virtually meaningless, and that the only meaningful measure — and I mean capital letters ONLY — is the cost of servicing that debt. That cost is extremely low right now as a percentage of GDP and as a percentage of Federal expenditures and Federal revenues, and will remain low for a long time according to current projections.

The United State Government in 200 years has never had the slightest problem paying off all debts when they come due, and for a variety of reasons, including the fact that the U.S. issues the currency in which the debts are created, will not have a problem for the next 200 years. We have had higher debt-to-GDP ratios before, as has the UK and Japan today, and have had no problem dealing with them.

Thus, it seems to me that sane people should be repeating this message:

(1) There is no such thing as “the” national debt, only thousands upon thousands of relatively small debts that have to paid off only when they each come due over the next 30 years.

(2) Accordingly, there is no national debt or deficit crisis whatsoever, because the cost to the government of servicing that debt — redeeming obligations when they come due and paying interest is as low as it’s ever been. That’s the only thing that matters.

(3) We have paid our debts for 230 years and will have no difficulty doing so for the next 230 years.

(4) The people who are playing Chicken Little over these matters are stupid people who have no clue what they are talking about. What matters now is full employment and higher wages, period.

(5) And by the way, if you just can’t get debt and deficits out of your brain, nothing brings them down like strong economic growth.

Bruce Webb, sorry I did not keep the URL that was posted on the 6% on assets deposited at the Federal Reserve. The URL was posted over on naked capitalism thread and the 6% interest was the only thing that was really new to me. Plus on posting the interest figure in debate with author it was not question so I accepted that it like the rest of the information was correct. I assumed it was in the original contract between the Federal Reserve and the Government, which I have never read.

I don’t know anything about the subject but can find the 6 percent figure:

http://www.federalreserve.gov/aboutthefed/section7.htm

Thanks PJR, that helps a lot. From your link:

“a) Dividends And Surplus Funds Of Reserve Banks.

Stockholder Dividends.

In General. After all necessary expenses of a Federal reserve bank have been paid or provided for, the stockholders of the bank shall be entitled to receive an annual dividend of 6 percent on paid-in capital stock.

Dividend Cumulative. The entitlement to dividends under subparagraph (A) shall be cumulative”

“Paid in capital stock” is very much different than “deposits”. You can see both in the following balance sheets of the Fed (see Table 5)

http://www.federalreserve.gov/releases/h41/current/h41.htm

“Paid in capital” adds up to $28 billion (with a B) out of total “capital” of $58 billion. Whereas deposits add up to $2.792 trillion (with a T). That is the latter which are ‘paid’ interest at 0.25% are almost exactly 100X those that are paid dividends at 6%.

So sincerely thanks, This stuff is somewhere between hard and mindbending and I learn more about it every time someone links me to a new table or report.

urban legend, there are only two means of adding currency to the system….fractional reserve banking and Federal Reserve threw selling bonds and treasuries. Both are debt based.

The money added by the banking system threw fractional reserve banking to companies and a person is not part of the national debt.

National debt is only that money printed from sale of bonds and treasury threw the Federal Reserve.

Beene can you explain or point to the mechanical role of the Fed in selling Treasury Bonds and Notes? Because I don’t see it. Which doesn’t mean it doesn’t exist. But I don’t see their role in the auctions other than as a buyer.

PRJ, thank you for finding and posting the URL.

How Treasury Auctions Work

http://www.treasurydirect.gov/instit/auctfund/work/work.htm

I don’t see the role of the Fed here

Bruce Webb, the Federal Reserve buys bonds to reduce the amount of currency in the system and sells bonds to add currency to the system.

This is one of many URL’s you can find doing a search on this subject.

http://money.howstuffworks.com/fed10.htm

How the Fed Works

by Lee Ann Obringer

Bruce Webb, confused by what I read at the URL you posted, which represents a government site.

As it seems to state at the URL you posted that the treasury runs the auctions.

Webb – Good one. The $2.6T of short term deposits are levered 100 to 1.

That’s huge leverage. Much more than any hedge fund. A bank is restricted by Basel II to 8%. JPM has half the assets and $238B of market cap.

Is it possible for the Fed to incur an annual loss equal to the $58b of capital? Sure it is. $58 is 1.4% of the asset portfolio. That’s a slim margin.

Does it matter? No, not really. But when you look at the debt/equity and the implied leverage at the Fed it does look goofy by most standards.

The solution is simple. The Fed must build up more equity. It could do that with no problem, just cut in half the amount that Treasury takes each year.

Oh…You wouldn’t like that outcome.

Krasting what possible relation is there between “Paid in Capital” by some (probable) subset of Fed member banks and their “Short Term Deposits” that would justify the concept of leverage? And what difference would it make if the Fed actually lost $58 billion in what is scored as a liabilty on their books? If fact how would Fed annual losses actually subtract from “Paid in Capital” to start with?

“Does it matter”. Well no. And it only looks goofy if you are applying standards that don’t remotely apply to Fed operations.

Beene what I was responding to was this:

“National debt is only that money printed from sale of bonds and treasury threw the Federal Reserve.”

I read that as meaning that “sale of bonds and treasury” that add to “National Debt” was in some matter done “threw (sic) the Federal Reserve”. When in fact the purchase and sale of bonds and treasury done by the Federal Reserve neither adds to or subtracts from Total Public Debt or its subset Debt Held by the Public.

Perhaps I misunderstood. Then again your language was less than clear here. Because your 6:32 seems to differentiate between two methods of adding to the currency, one through “fractional banking” which isn’t debt based and then “through selling bonds and treasuries” which are debt based. Which reads as if the Fed was a part of the original issuance of bonds and notes rather than a player in the secondary market (or perhaps as an original purchaser at auction). Can you clarify?

Webb – You ask:

(or perhaps as an original purchaser at auction)

No, the Fed is not permitted to buy bonds at a Treasury Auction.

http://www.federalreserve.gov/faqs/money_12851.htm

Webb – A definition of leverage:

“Most often it involves buying more of an asset by using borrowed funds, with the belief that the income from the asset or asset price appreciation will be more than the cost of borrowing.”

The Fed borrows $2.6T and buys bonds. This is the textbook definition of leverage.

Thanks BK.

So not to put words in your mouth but it would seem this confirms that the Fed is simply not involved with actual issuance of Treasuries and so is not in control in any way with the level of Public Debt (except to the degree that their holdings are (as I suggest) effectively off the books because of rebates to Treasury)

As to your second comment.

One borrowing money and purchasing an asset is not the textbook definition of leverage. That instead is just part of the bog-standard way that companies of all types finance operations. Borrowing money and purchashing a speculative asset in hopes that gains from that investment will exceed borrowing cost is closer to the concept of leverage. And borrowing money and using to invest in assets on 10% margins is actually the definition of leverage. But one for one borrowing doesn’t meet that definition.

Two you have never explained from whom the Fed is “borrowing” and via which instrument. Looking at the Fed Balance Sheet it would appear that all assets are balanced out by liabilities in the form of currency and deposits. Since issuing new currency is not “borrowing” it would seem that it could only come in the form of requiring or inviting banks to hold deposits with the Fed. Which deposits are currently only being paid 0.25% in interest or what is actuall a negative real rate.

So sorry I just don’t see that as “borrowing” and still less “leverage”. Maybe I am just slow and stubborn.

Webb – 1 for 1?? You said before it was 100 to 1.

You also previously pointed out that the Fed has $2.6T of deposits that are clearly recorded as liabilities. They are liabilities as the Fed has to pay this money back – with interest.

Krasting the 100 to 1 is “Deposits” to “Paid in Capital”. The 1 to 1 is your “Fed borrows $2.6T and buys bonds”. The former has nothing to do with the latter even on your formulation.

And in what sense does the Fed have to “pay back” deposits? I suppose it could lower reserve requirements and so allow member banks to take back their deposits and leverage them on their own account. But I don’t see how allowing this withdrawal of EXISTING deposits would require any kind of borrowing. And as Robert noted the other day there is no absolute requirement that the Fed pay interest on excess deposits, that it has chosen to do so (at an effective negative rate of 0.25% nominal) is neither here nor there. Especially since their would be no need to pay interest on deposits AFTER they are withdrawn.

Not to mention that your whole premise seems flawed. Although mandated reserves are scored as liabilities on the Feds balance sheet there is no possibility that they can all be drawn down to zero. Because it is the existence of those reserves AT SOME LEVEL that allows banks access to Fed facilities like the discount window. To that degree mandated reserves are just the pay to play for these banks to be members. Now I am certain that the actual level of those mandated reserves is less than the current $2.6T in deposits. But how much less? How much of that figure is actually in the category of Excess Reserves that draws IOER?

But in any event mandated reserves are not operationally the same thing as current debt. Not if they can’t be called by the “lenders”, in this case member banks.

This is the same issue that I have brought up time and again both in relation to Intragovernmental Holdings and Debt Held by the Public. to the degree that a very large proportion of Intragovernmental Holdings are in the form of legally mandated (or at least targeted) reserves then under correct policy prescriptions (to include the Northwest Plan for Social Security) they will NEVER be paid back. Similarly some proportion of Debt Held by the Public is irreducible due to the dollars function as currency of account for any number of commodities plus the role of U.S. Tressuries as a ‘Flight to Safety’ instrument. That is the world economy needs a certain amount of Treasuries in circulation just to keep international liquidity. Just as there is a need to keep a certain amount of U.S. currency in circulation to keep both the domestic economy and to a lesser degree foreign economies going. Now it is true that every dollar in circulation is carried on the Feds books as a liability but there is no sense that they have to be “paid back”. Federal Reserve Notes simply don’t have the same type of claims for redemption that old time Treasury Gold and Silver Certificates do.

You seem to have fatally confused the whole concept of “liabilities” with “debt”. Something that makes a certain sense when applied to a corporation that at any time faces the theoretical possibility of having to be wound down in bankruptcy but which doesn’t apply to a country which can pay debt in its own currency and issues that currency through an semi-independent central bank. Just because certain categories of account are carried on the liabilities side of the balance sheet, like currency in circulation and mandated reserve deposits doesn’t make then debts subject to “pay this money back – with interest”. Plus even that portion of those liabilities that DO have to be “paid back” are currently only carrying interest rates of 0.25%. Except the miniscule in context $28 billion in “paid in capital” which is neither here nor there (though carrying a 6% dividend).

Webb – the member banks are not obligated to leave reserves with the Fed. If the banks had something better to do with these reserves they would do so.

Look at the movement in excess reserves over the past year. A $400b swing:

http://research.stlouisfed.org/fred2/series/EXCSRESNS

Webb – From Ben Bernanke today:

Although reserves in the banking system are not expected to return to pre-crisis levels for some years, the Fed has a number of instruments—including its authority to pay interest to banks on their excess reserves, as well as the ability to offer reverse repurchase agreements that effectively allow nonbanks to deposit at the Fed at a fixed interest rate—that should allow it to manage short-term interest rates effectively (see here and here for further discussion). Concerns about unwinding quantitative easing are therefore misplaced, in that the Fed’s ability to tighten monetary policy at the appropriate time will not require that it sell assets or rapidly reduce the size of its balance sheet. To the extent that the large balance sheet has some residual effect on longer-term yields, the effects on the economy can be compensated for by changes in the federal funds rate.

So – The Fed has no plan to sell any bonds in its portfolio to raise interest rates. The tool it will use to increase interest rates is a rise in the Fed Funds target. This will be achieved with increases in IOER.

I bring this up (again) to try to convince folks that selling bonds is not in the cards. There appears to be many readers who misunderstand this.

http://www.brookings.edu/blogs/ben-bernanke/posts/2015/04/15-monetary-policy-in-the-future?rssid=Ben+Bernanke

Webb – From the FT this morning:

The central bank has said it will use two interest rates to set the ceiling and floor of its target range when it starts lifting rates from near-zero levels that have prevailed since 2008. The interest rate the Fed pays on banks’ excess reserves will be used to set the upper end of the range, while the floor will be established through a new “overnight reverse repo programme” — or ON RRP.

http://www.ft.com/intl/cms/s/0/cfc1e9da-e3c1-11e4-9a82-00144feab7de.html#axzz3XTC5mBnV

@Bruce: “Are you suggesting that Fed SOMA holdings should be scored as Intragovernmental Holdings? ”

Yes. But I’m also suggesting I’d be happy if we could just get the press to stop citing Gross Public Debt, an arbitrary and meaningless figure.

@bkrasting:

When the Fed buys bonds, it does not pay with bank deposits (and certainly not physical currency). It pays with Fed reserves — “bank money” that is only exchanged among Fed account holders. That “money” can only exist in Fed accounts, can only be traded/borrrowed among holders of Fed accounts, and can never, by its very nature, be converted into bank deposits.

Certainly there are second- and third-order effects to these bonds-for-reserve swaps, but those should not be confused with the misplaced notion of the Fed “injecting bank deposits into the economy.”

@bkrasting: “The central bank has said it will use two interest rates to set the ceiling and floor”

Great stuff. There’s been some great writing on the “corridor” system. As so often, Steve Randy Waldmann has delivered some of the best”

http://www.interfluidity.com/v2/3763.html

It seems that the Fed has moved very far away from any notion of controlling the “money supply” (whatever that is; economists have never agreed).

Steve can you explain where those “Fed reserves” show up on the balance sheet or contrawise why they don’t need to? Because your comments here offer me a path out of personal confusion.

My understanding was that Fed purchases of bonds was effectively an increase in money supply, the equivalent of just cranking up the presses and creating new Federal Reserve Notes and using them to buy existing Treasury bonds and notes. As such it would seem that these should show up on the Fed Balance Sheet as liabilities in the same way that actual currency does. But they don’t seem to. Which would seem to suggest that the Fed balance sheet I am seeing is by no means the whole picture and that there is another set of accounts that takes on those “bank money” ones.

There is a reason I am putting most of this in the form of questions. Because I don’t know the right answers. Which doesn’t mean I can’t spot the wrong and illogical ones. Any help on this would be appreciated.

Krasting says:

“Webb – the member banks are not obligated to leave reserves with the Fed. ”

The Fed says:

“Reserve requirements are the amount of funds that a depository institution must hold in reserve against specified deposit liabilities. Within limits specified by law, the Board of Governors has sole authority over changes in reserve requirements. Depository institutions must hold reserves in the form of vault cash or deposits with Federal Reserve Banks.

The dollar amount of a depository institution’s reserve requirement is determined by applying the reserve ratios specified in the Federal Reserve Board’s Regulation D to an institution’s reservable liabilities (see table of reserve requirements).”

http://www.federalreserve.gov/monetarypolicy/reservereq.htm

Since “vault cash” simply means Federal Reserve Notes and so serve as a sort of off site reserve of Reserve Notes I don’t see how you can defend your statement. If you examine the Table at the link you can see that big banks have a REQUIREMENT to hold 10% in reserves and typically do so in deposits with a Fed Reserve Bank. Certainly they are not free to “If the banks had something better to do with these reserves they would do so”

Well it would appear that the answers to my questions can mostly be found starting from the links on the following web-page of the Fed:

Federal Reserve liabilities which is just one of a larger set of pages under the rubric Credit and Liquidity Programs and the Balance Sheet

http://www.federalreserve.gov/monetarypolicy/bst_frliabilities.htm

So I have some reading to do. And suggest that I am not the only one who could benefit.

Another reading tip, this time with oodles of numbers:

http://www.federalreserve.gov/releases/h41/current/h41.htm#h41tab2

FEDERAL RESERVE statistical release

H.4.1

Factors Affecting Reserve Balances of Depository Institutions and Condition Statement of Federal Reserve Banks

Of particular interest to me and bearing directly on Steve’s post is Table 2 which shows the breakdown in Fed holdings of various categories of Fed bills, notes and bonds and MBS. This in turn can be directly compared with the following from Treasury showing the total breakdown of Fed bills, notes and bonds with average interest rates.

https://www.treasurydirect.gov/govt/reports/pd/feddebt/feddebt_mar15.pdf

Schedules of Federal Debt and esp Note 2

@Bruce: “Steve can you explain where those “Fed reserves” show up on the balance sheet or contrawise why they don’t need to? Because your comments here offer me a path out of personal confusion.”

Those reserves appear as liabilities on the Fed BS and assets on the aggregate “banks” balance sheet.

Here’s the crucial point, though: banks (in aggregate) can’t redeem those reserves for anything except…reserves! Or physical currency (which are also bank reserves — “vault cash.”) Only the Fed can choose to change the total quantity of reserves held by the banks. Banks can only exchange them among themselves.

The exception is currency redemption, but it doesn’t really matter. The fed will redeem banks’ reserves for physical currency on demand. But the only reason banks swap is if they need more “vault cash” — because their customers need more cash for cash transactions.

That physical cash requirement doesn’t change much over time, and it’s pretty much immaterial what proportion of banks’ total reserves they hold in vault cash vs. fed reserves, as long as there’s enough cash available for those transactions. (Note two usages of “reserves” in that sentence.) That’s why the Fed does those swaps on demand — so there’s always as much physical currency as cash buyers need and want.

The one exception would be if the Fed’s interest paid on reserves fell significantly below zero. “The banks” would want to warehouse physical cash instead of leaving their reserves on deposit with the Fed. But it’s hard to see how this would have any effect at all on bank depositors’ balances, or their larger portfolio-allocation decisions.

@Bruce:

MBSes are an important issue. Are Fannie and Freddie part of “the public,” or part of government? If they’re part of government, MBSes held by the Fed are debts that government owes itself.

We could have four measures of “the national debt”:

Gross Public Debt

Debt Held by the Public

Debt Held by the Public less treasuries held by the Fed

Debt Held by the Public less treasuries and MBSes held by the Fed

The last two could be characterized as “true” Debt Held by the Public…

Steve Roth – Sorry, you’re walking into a trap. Your thinking adds to the definition of national debt. You say:

“If they’re part of government, MBSes held by the Fed are debts that government owes itself.”

Okay, fine. But you can’t have it both ways. If the Fed’s ownership comes off the ledger, then the debts of Fannies must also come on the ledger. F/F have combined MBS of $5.2T. The Fed owns 1.7T of that.

Either all of the debts are obligations of the government, or they are not.

@bkrasting: “Either all of the debts are obligations of the government, or they are not.”

Just not that simple.

1. The Fed’s “reserve” liabilities (The Banks’ aggregate “deposits” at the fed) are not redeemable by the banks for anything except physical currency, which Treasury/Fed creates at will for free. They will never, can never, be redeemed for bank deposits held by “the public.” As opposed to treasuries, where interest and principal are constantly going into “the public’s” deposit accounts.

2. I’d have to look more carefully at fannie/freddie/ginniamae balance sheets, the nature of their liabilities and those liabilities’ redeemability. This is certainly much more of a stretch.

One more time….I will rely on Alan Blinder, ex Vice Chair of the Fed.

There has been an ongoing debate about IOER. Many have advocated that IOER be lowered to zero (from 0.25%). Others have argued that the rate should be set BELOW zero.

The argument put forward is that if IOER were at -X% it would force the banks to either buy securities or make loans. This is called “High Powered Money”.

Blinder made his case for negative IOER in the following article. A key sentence:

“If the Fed turned the IOER negative, banks would hold fewer excess reserves, maybe a lot fewer. They’d find other uses for the money. ”

So this Fed Governor is saying that those excess reserves are not held captive by the Fed, and under certain circumstances those excess reserves can be diverted elsewhere. The comments from above seem to have a different interpretation.

http://www.wsj.com/articles/SB10001424052702303997604579238403178592262

S Roth – Yes, do have a look at the F/F balance sheets. The quick picture is:

They issue and guarantee MBS. Between Fannie and Freddie they have $6.2T of guaranteed paper outstanding. They have next to no equity as they, like the Fed, remit all of their profits to Treasury.

Ownership is a confusing picture. F/F are public companies. They have shares that trade in public markets. They issue all of the SEC stuff that public companies do.

Funny thing – In accounting, If Company A owns 100% of the shares of Company B it is a 100% owed consolidated entity. Company A must report the assets/liabilities of B on its balance sheet.

However, if the ownership is Less Than 80%, Company A does not have to report the assets/liabilities of Company B.

Follow this to the F/F story. If Treasury owned more than 80% of F/F then it would have to report the debts of F/F on the Federal Balance sheet. This would have added $6T of debt to the Federal Ledger.

So what did the bright guys at Treasury do to avoid this undesirable outcome? Simple! Treasury owns 79.9% of the common stock of F/F. Another Tenth % more to cross the line. How convenient…..

You guys think I’m a cynic. Maybe so. But when I see the micky mouse stuff that goes on to avoid the reality that the tax payers are on the hook for F/F, I think my cynicism is justified.

@bkrasting, blinder: “”If the Fed turned the IOER negative, banks would hold fewer excess reserves, maybe a lot fewer. They’d find other uses for the money. “”

Stunning to see, this fundamental error of composition that has been resoundingly debunked in papers from pretty much every central bank in the world. Individual banks can swap reserves for other assets among themselves. They have no control over the aggregate quantity of reserves in the system. Full stop.

Not surprising to see a conservative fiscal and monetary hawk clinging frantically to patently, obviously false beliefs…

Steve Roth

Since I don’t know anything, I have nothing to lose:

banks can hold any amount of excess reserves they want. anything between the required reserve and their total deposits, limited only by the fact that they make money by lending lending money.

however you refer to “aggregate” reserves. i don’t see where a large number of banks deciding to hold excess reserves does not increase the total amount of reserves being held by banks in general.

if i am wrong about this, it will be a pleasure to be instructed.

@Coberly:

The only way an individual bank can reduce its reserve holdings is by…giving them to another bank (in return for bonds or whatever). The aggregate stock of reserves is unchanged, just transferred.

There’s no place else reserves can go.

Except: back into the gaping maw of the Fed, where they are incinerated, dumped back into the same magical hole in the ground that they came out of in the first place.

Only the Fed can choose to do that. (They do that by selling their stock of bonds at just below market prices — so banks inevitably purchase them — receiving reserves in return. And guess where those returned reserves go? See “hole in the ground,” above. Poof!)

Steve

are you failing to note “excess” reserves?

otherwise i may simply not know enough to understand your point.

banks can hold as much reserves as they want over the required amount. they usually don’t because they use that money to make money, but it seemed to me that after 2008 all of a sudden banks developed a sudden love for excess reserves.

and found a way to get paid for keeping them idle.

@Coberly:

I think you’re confused by the multiple uses of the word “reserves.”

http://angrybearblog.strategydemo.com/2013/06/defining-reserves.html

Think: banks’ deposits at the Fed.

Well there is a certain amount of talking past each other here and much to my chagrin Krasting has the advantage on some points.

Coberly in his 1:59 asks a pertinent question that Steven actually gets confused (it seems).

Banks have mandated reserves at the Fed depending on their overall size. These reserves are restricted in the way Steve talks about in his 12:46. But these restrictions DON’T apply to “Excess Reserves”, which is the point that Krasting rightly makes in his 6:53 citing Blinder. The question then for Krasting would be to break out “Excess Reserves” from mandated “Deposits” and then arithmetic-ing from there.

On MBS’s. From where I sit both Roth and Krasting are wrong though unfortunately Steve a little more so.

Seems to me that we have to make a distinction between mortgages generally , MBSs and Freddie and Fannie insured mortgages. Mortgages are clearly debts owed by property owners to the mortgage holder. This fact does not change in the cases where they are sold to Freddie and Fannie (which can only be done if they are ‘prime’ at least historically) or really when they are securitized into MBS’s purchased by Freddie, Fannie, third parties or the Fed. Those mortgages and derived securities ultimately rely on property held by the borrowers and this regardless of whether the mortgages are insured by a government agency. Which makes Steve’s 12:52 fall apart. Even if all MBS’s were actually backed by Freddie and Fannie. Which they aren’t. So against my will I am going to have to score some points for Krasting’s 1:26 and 7:28 and suggest we just leave F&F and MBS’s out of this discussion.

Which leaves the question of how much of the $2.6 T or so of Bank deposits held by the fed are officially “excess” and so subject to IOER (“interest on excess reserves”) and so potentially withdrawable by banks for their own purposes. Which in turn legitimates Coberly’s questions at 9:20 and 1:59 and seems (pending some further reading) to make Steve’s 8:14 claims inadequate.

My take anyway.

And Steve I followed your link and found some confusion on an important point. Because the following seems to suggest there are three (or four) places to park reserves, only one of which would show on the Fed’s actual balance sheet:

“2. “Required reserves.” A regulatory amount (percentage of deposits) that banks are required to hold in specified “safe” assets — significant examples being treasuries, vault cash, gold (in their vaults or the Fed’s), and…reserve balances. The term “required reserves” does not appear on banks’ balance sheets.”

But on my reading any such treasuries would indeed have to be held at and by the Fed and would show up on its Balance sheet. (And I’ll leave the gold question aside for the moment).

I found this article from the Liberty Street Economics blog maintained by the NY Fed both enlightening and convincing:

Interest on Excess Reserves and Cash “Parked” at the Fed

http://libertystreeteconomics.newyorkfed.org/2012/08/interest-on-excess-reserves-and-cash-parked-at-the-fed.html

An extended extract:

“What determines the size of the monetary base? As with any other institution’s balance sheet, the Fed’s dictates that its liabilities (plus capital) equal its assets. The Fed’s assets are predominantly Treasury and mortgage-backed securities, most of which have been acquired as part of the large-scale asset purchase programs. In other words, the size of the monetary base is determined by the amount of assets held by the Fed, which is decided by the Federal Open Market Committee as part of its monetary policy.

It’s now becoming clear where our story’s going. Because lowering the interest rate paid on reserves wouldn’t change the quantity of assets held by the Fed, it must not change the total size of the monetary base either. Moreover, lowering this interest rate to zero (or even slightly below zero) is unlikely to induce banks, firms, or households to start holding large quantities of currency. It follows, therefore, that lowering the interest rate paid on excess reserves will not have any meaningful effect on the quantity of balances banks hold on deposit at the Fed.

Language Matters

The language used in the press and elsewhere is often imprecise on this point and a source of potential confusion. Reserve balances that are in excess of requirements are frequently referred to as “idle” cash that banks choose to keep “parked” at the Fed. These comments are sensible at the level of an individual bank, which can clearly choose how much money to keep in its reserve account based on available lending opportunities and other factors. However, the logic above demonstrates that the total quantity of reserve balances doesn’t depend on these individual decisions. How can it be that what’s true for each individual bank is not true for the banking system as a whole?

The resolution to this apparent puzzle is that when one bank decides to hold a lower balance in its reserve account, the funds it sheds necessarily end up in the account of another bank, leaving the total unchanged (see FT Alphaville and this New York Fed Current Issues in Economics and Finance article for more detailed discussions of this point). In the aggregate, therefore, these balances do not represent “idle” funds that the banking system is unwilling to lend. In fact, the total quantity of reserve balances held by banks conveys no information about their lending activities – it simply reflects the Federal Reserve’s decisions on how many assets to acquire.”

This resolves much of my puzzlement, perhaps it will be useful to you-all as well.

Bruce

thanks. it doesn’t resolve much of my puzzlement: that will take some study. perhaps i am hung up on the tiny bit i “know” but it seems to me there is indeed either some loose use of language here (and there) or perhaps my book failed to make the distinction for me between “reserves” held at the individual bank and reserves held “at the Fed.”

in either case it seems to me that “excess” reserves can be withdrawn by the individual bank from the Fed without being made up for by increased excess reserves from another bank. the difference still seems to me between “required” reserves and “excess” reserves.

also the language in your extract (thank you for that) does not conform very well with the textbook i am looking at. it is possible the text book is wrong or outdated, or not telling the whole story, or i am still too ignorant to understand, or that, as so often seems to me, the tellers of the story are not being careful enough to make sure we all understand the “words” they are using the way they mean them.

The Fed requires reserves equal to some fraction of “liabilities”. It does not “set” the size of “the monetary base” (if that means “the amount of money in circulation) but attempts to increase or decrease that by buying and selling bonds or setting discount rate. What determines the size of the monetary base is how much money the banks create by lending to its customers.

sorry if that is still confused… if it’s me, i’ll try to work it out.

and just to show how confused, it seems to me that however much the United States may be “on the hook” for guarantees to Freddy et al, that is not the same as “national debt” except maybe to someone like Kotlikoff.

@Bruce:

No. Where the confusion arises:

For this discussion and for clarity, let’s stop calling “TheBanks’ Deposits at the Fed” “reserves.” It’s really a confusing misnomer, though it made sense historically.

Now, TheBanks’:

Deposits at the Fed

+ Vault cash

+ Bonds

+ Gold

+ etc.

Equals:

Banks’ Total Reserves

Equals:

A regulatory amount of “required reserves”

+ Excess reserves

You can’t point at any of those particular assets (bonds, gold, etc.) and say “those assets there are the required reserves.”

As things stand currently, TheBanks’ total reserves (held in various assets) wildly exceed required reserves, so required reserves vs. excess reserves is pretty much immaterial. Fuggedaboutit for now. They’ve just got a shitload of reserves.

Some of those reserves are held as deposits at the Fed.

Individual banks can change their proportional holdings of Deposits at the Fed (their asset portfolio mix) by swapping them with other banks for other reserve assets (transferring those Deposits, but not changing the aggregate quantity of Deposits at the Fed held by TheBanks.)

Only the Fed can change that total quantity of TheBanks’ Deposits at the Fed, by buying bonds from the banks (giving them Deposits at the Fed), or selling bonds to the banks (receiving Deposits at the Fed in return).

When the Fed sells bonds to TheBanks, the Fed loses an asset (the bonds) and loses the Deposit Liability. Their balance sheet shrinks; the Deposit liability simply vanishes, and the bonds go to TheBanks’ balance sheet.

The size of TheBanks’ balance sheet is net zero: plus bonds, minus Deposits. The Fed’s bond purchases just change TheBanks’ portfolio mix.

IOW:

Bond purchases affect both sides of the Fed’s balance sheet.

They only affect the lefthand side of TheBanks’ balance sheet.

Or to put it another way:

Neither an individual bank, nor TheBanks, can force the Fed to buy or sell bonds. They can’t — individually or collectively — control the size of the Fed’s balance sheet.

The Fed can force TheBanks to buy or sell bonds by issuing the cheapest sell order, or the highest buy order.

Individual banks have no choice but to take those best offers, so TheBanks end up buying or selling the Fed’s bonds, just as the Fed wishes.

So the Fed has some control over TheBanks’ portfolio mix, which has second- and third-order effects on the financial markets, which might even affect the real economy. The Fed certainly likes to think it does, and to be fair, it almost certainly does. It’s just that nobody can seem to quite agree on what those second- and third-order effects are.

@Coberly: “it seems to me that “excess” reserves can be withdrawn by the individual bank from the Fed”

Withdrawn and put where?

Steve seems to think that the Fed beats and whips the poor banks. Forcing ‘The Street’ to do as it commands.

Sorry, all QE was done at auction. No one was ever forced to do anything. When the banks offered the paper to the Fed, they did it because they were making money on the trade. Period full stop.

You’re talking about a topic that falls under the definition of Fixed Income Trading. I have a history in this world. By far and away the fixed income side is the most lucrative of all the Wall Street businesses. The reason? Simple, there is so much paper going back and forth you can’t help but make money in the process.

Fannie, Freddie, Treasury and the Fed pay 10s of billions a year to Wall Street to shuffle their paper.

Follows an article under search “Fed Buys recently issued bonds”. The links etc in the story are available. Basically Treasury sells to the Banks, a few days later the Fed buys the SAME (cusip) paper from the banks (QE). This happened on a weekly basis for years. For Wall Street that is a cash machine. A $4+ Trillion buyer is an elephant you can make money on.

Who holds the cards at this table?

http://www.zerohedge.com/news/2013-02-19/fed-buys-back-30-year-bond-auctioned-last-thursday

Steve

the banks can withdraw their excess reserves and bury it in the backyard if they want. or buy Enron stocks. or give a great big party. trouble would come only if there was a run on the bank in excess of their reserves (required or excess) to meet it.

chances are the banks would “invest” their excess reserves in something more prudent than Enron, but they seem to be having as hard a time as i am finding anything prudent to invest in.

so its nice for them the Fed is paying interest on excess reserves.

disclaimer: i still know nothing. i still defer to Krasting on bonds. my comment is offered only in the spirit of provoking others to make their points clear enough for an idiot to understand.

my limited understanding of accounting tells me you can’t affect the left hand side without affecting the right hand side.

@bkrasting: “because they were making money on the trade”

Because the fed offered the best buy offer, outbid the market. No “beats and whips” moral valences attached. It’s just the way it works.

@Coberly: “the banks can withdraw their excess reserves and bury it in the backyard if they want. or buy Enron stocks.”

So a bank trades Deposits for physical currency.

Gives the currency to you to buy your Enron stock.

You deposit the currency in your bank.

Your bank doesn’t need all that currency, so it gives it back to to the Fed in return for….Deposits at the Fed.

The only non-bank entities that hold onto any significant hordes of physical currency, don’t deposit it in banks, are criminal enterprises.

Treasury currency outstanding constitutes 1% of the Fed balance sheet.

Immaterial to our discussion.

@Coberly: “my limited understanding of accounting tells me you can’t affect the left hand side without affecting the right hand side.”

You haven’t even stopped to think about this for a moment.

You can change your asset portfolio mix (the left side) without touching your liability side. People/banks/etc. do it constantly when they buy and sell stocks and bonds.

C’mon, man. Don’t play dumb. Think.

“Treasury currency outstanding constitutes 1% of the Fed balance sheet”.

Steve how are you defining “treasury currency”? Is there even such a think? Now certainly there are “Federal Reserve Notes in circulation”, what almost everyone would think of as “currency”. And per the most recent Fed Balance sheet these add up to $1.3 T which is more than 25% of the Feds liabilities of $4..4 T. So I am baffled at your reference here. Perhaps you are referencing the category of liability called “U.S. Treasury, General Account” but that would hardly seem to be the same as “Treasury currency”

http://www.federalreserve.gov/monetarypolicy/files/quarterly_balance_sheet_developments_report_201503.pdf

See Table 1

Yes I screwed up on currency number. No time to address right now.

But back to the topic of this post:

“Focusing on “net” government debt (which excludes intra-government debt holdings, such as the bonds owned by central banks) is a more effective approach to assessing and ensuring the sustainability of public debt.”

http://www.project-syndicate.org/commentary/global-debt-dilemma-by-adair-turner-and-susan-lund-2015-04

Steve

i think we went round and round about the inability to change the amount of savings once before. and yet the amount of savings changes. i suspect it has something to do with the difference between “savings” in the bank for less than 24 hours, and savings in the bank for a year or more. it works a little like the greenhouse effect.

and yes, i failed to realize you were talking about changing items on the left side for each other. whether that was “not thinking” or “not even trying to think” i am in no position to know.

as for the clarity of your exposition… well i am in a position to have an opinion about that. please don’t play cute with me. you won’t like me when i get mad.

Well Steve and getting back to the point of the post and reminding one and all that I have posted a number of times on this exact subject the question now becomes “Who bells the cat?”

I have been working for years here to get people to understand the difference between “Public Debt” and “Debt Held by the Public”, two terms that tend to get used interchangeably but where the latter is simply a component of the former. And I am all in with people understanding that along side “Intragovernmental Holdings” we have $2.5 T of “Public Debt” (officially counted under “Debt Held by the Public”) that is actually held by the Federal Reserve and because of the way that the Fed rebates profits to Treasury shouldn’t really be considered “Real Debt”. I have even gone farther than THAT and pointed out that the Fed’s $2.5 T is heavily weighted towards longer term/higher coupon treasuries meaning that the “Real Cost of Debt Service” of “Debt Held by the Public” is much much less in both nominal dollar terms and in interest rate terms than a simple examination of “net interest” and “average interest rate on Treasuries would suggest” and in fact is actually very close to a negative real rate.

Beyond all this I have often asked the question as to how much of U.S. Treasury ‘debt’ is actually structurally needed simply to keep the wheels of world commerce running. As long as major commodities like oil are priced in dollars and U.S. Treasuries serve a vital “flight to safety” function there is clearly a need for SOME level of U.S. debt instruments. Presumedly that amount once subtracted from “Total Public Debt” alongside “Intragovernmental Holdings” and Fed SOMA holdins would still leave some trillions of dollars of “real” debt. But for the overall purposes of your post it would be nice to have an actual dollar figure for that.

Unfortunately we are back at “bell the cat”. I maintain, and I think with good evidence, that the mainstream press and much of the financial press either fails to understand the difference between TPD and DHBTP or perhaps more likely enjoys deploying the bigger number so as to justify the worldwide austerity fetish of our political classes. I mean if you Google the question “What is the amount of U.S. debt?” (and I just did) you will find that every first page result highights TPD. Which not only includes Intragovernmental Holdings but also that portion of Debt Held by the Public actually held by the Fed.

So I welcome your quest. But suggest you maybe ignored pesky obstacles 1 and maybe 2 on your way to slaying the dragon at gate 3.

Hey Bruce:

So sorry that I’m not more aware of your previous on this. Over the last couple of years I’ve been doing most of my “following” via twitter instead of an RSS reader, and I just realized that AB stopped tweeting new posts two years ago. I pinged Dan about reinstating that auto-tweeting.

On the substance: your points are extremely well-taken. I guess we can only keep tilting at that windmill…?

Bruce Webb April 15, 2015 11:31 am

Beene except that assets on deposit are not guaranteed 6% by law.

“When banks join the Federal Reserve System, they are required to buy stock in the central bank equal to 6 percent of their assets. However that stock does not gain value and cannot be traded or sold, so to entice banks to participate, the Fed pays out a 6 percent dividend payment.”

More……….http://thehill.com/policy/finance/249135-banks-revolt-over-plan-to-kill-17b-fed-dividend-cut

Beene total stock paid in by banks is $56 billion. Reserves/assets on deposit amount to several trillion.

Stock gets a 6% dividend

Reserves are current paid at the Fed Funds rate or 0.25%

Bruce Webb April 15, 2015 8:29 pm Beene what I was responding to was this: “National debt is only that money printed from sale of bonds and treasury threw the Federal Reserve.” –

Bruce, an error on my part, as all treasury notes and bonds sold by the Treasury are debt of the nation.

I mistakenly believed that the Treasury sold only to the Fed.

I still believe that as stated in Brown’s book Web of debt we would be a lot richer not paying interest on printing our own money. There is a formula in the above mentioned book that shows how quacking the debt could be eliminated.

Just to give a bit more information and follow up to this important topic. There is a very good post on the subject called : “Shocking, Little Known facts about Debt” posted on 11-11-15 from the Washington Blog. Also be sure to read the many fine comments that follow in that post. This article was also reposted the next day at Globalresearch.com

@William Ryan:

Thanks for that. I posted a comment over there.