More on Money, Currency-ness, Wealth, and Spending

Arthur over at New Arthurian Economics has posted a much-appreciated though decidedly negative reply to my recent post on the nature of money and financial assets. He and I have had very similar thinking over the years (and he has provided me, at least, with some Aha! moments), so I’d much like to convince him to give the thinking therein a solid road-test. This post is an attempt to encourage that.

First, slightly modified, what I said in a comment reply on that post:

The key (and I think hugely simplifying and clarifying) distinction:

money:financial assets::energy:barrels of oil.

In the vernacular we speak of oil as “energy,” but we know that they’re conceptually distinct. The energy is embodied in the oil. Just as it’s embodied in a rock at the top of a hill.

Pieces of currency are just financial assets (legal claims, or credits) that have particular characteristics, properties. As do barrels of oil and rocks on top of hills. We’ve always called those particular types of financial assets “money,” and therein is rooted much of the confusion and miscommunication we suffer under, IMNSHO.

Also, a key qualification that I’ve discussed in the past but didn’t in that post, which I’ll discuss more below: This thinking only works if you think of deeds as financial assets — claims on real assets, with the claim being conceptually distinct from the asset — the real estate — itself.

Like other financial assets, deeds as claims on real assets embody money. If you have more homeowner equity, you have more money. I don’t think this is crazy; homeowners’ ownership positions in the real-estate market, with associated mortgages, are arguably their most “financialized” positions. Owning (some portion of the claim on) a house in modern economies is fundamentally and conceptually different from owning an apple sitting on your kitchen counter. (I’ve long pondered a post on the nature of asset “ownership,” the legal and social constructs that constitute and define those claims, but I won’t go all the way there in this post…)

With that as background, some responses:

“… ‘money’ should be technically defined, as a term of art, as ‘the exchange value embodied in financial assets.'”

To me, money is the medium of exchange, not the exchange value.

Here, from the get-go, you are declining to try on this definition and conceptualization. By saying “money” is the “medium of exchange,” you’re thinking about money being currency-like things. I’m suggesting that that’s the very conceptual problem we’re struggling with. And as I’ve suggested before, the traditional textbook tripartite “definition” of money — medium of exchange, medium of account, and store of value — by its very tripartite nature, is a crippling non-definition. People talk past each other constantly, as I’m sure you’ve noticed in blogs and comments from Sumner to Rowe to Koenig to….

It sounds like you’re talking about erosion of the dollar’s value.

No. In fact that discussion is one key thing (inflation) that’s missing from my explanation and discussion. I was trying to keep that post somewhat short. See below.

But I think you are talking about the liquidity of financial assets.

Again, this is going to the J.P. Koenig “moneyness” place (which he says is purely a function of liquidity, an understanding that’s at the heart of divisia measures, for example). I’m suggesting that what he (and you) are really talking about is “currencyness.” That being the very conceptual problem I’m trying to address.

I see this as the source of our economic troubles. Things that are not money have come to be widely used and accepted as money.

I’m not really talking about our economic troubles here (until the end of the post, where I apply the conceptual framework from the beginning of the post). I’m talking about our economics troubles. Our difficulty thinking about how economies work.

How economies work? But since the crisis, or before, economies DON’T work.

I see you doing the same thing for “work” here that’s going on for “money” — confuting two meanings. I’m talking about how economies operate, how to think about the mechanisms. You’re saying they don’t operate well. (I of course totally agree, and think that’s partially because economists don’t understand how they operate.) Completely different conceptual levels/realms.

You make things too complicated:

I want to suggest: quite the contrary. Put on this conceptual suit of clothes and try it out. I’m finding it to be incredibly clarifying and de-complicating. No need for the endless (and by all appearances fruitless) wrangling about MOE, MOA, MB, M1, divisias, etc.

“dollar bills aren’t money. They’re embodiments of money”

Jesus, Roth. The embodiment of money IS money.

I’m not sure if you’re making that statement or ridiculing it. So two answers:

Making: If this, you are assuming a priori that currency-like things are money. And given that, I’m not sure what you mean by the embodiment of money here.

Ridiculing: That’s not what I’m saying at all. I’m saying that currency-like things (what we’ve always called “money”) are embodiments of money as I define it. As are other financial assets.

“Money and currency aren’t the same thing, and economists’ conceptual confution of “money” with “currency-like things” is central to the difficulties economics faces in understanding how economies work.”

Currency-like things are the things we spend… things that are current, things that flow.

I want to try a physical metaphor in hopes of making this thinking clearer: The stock of money is a bathtub full of financial assets. Their source is the two (or three) methods of creation described in the post. People can exchange those financial assets within the bathtub. (Give me your Apple stock and I’ll give you some currency or currency-like bank deposits. See Jesse Livermore explanation.)

There’s a pipe that comes out of the bathtub and goes directly back in. Every withdrawal is a deposit (between different accounts within the bathtub). Every expenditure is a receipt. Instantaneously, or almost. It must be so.

Those transactions cause transfers of real, newly produced goods and services between parties — sort of by induction as they pass by — thereby causing production of new goods and services. (When you transfer money to another’s account to pay for a massage or an iPhone, you cause a new massage or iPhone to be produced. Magic!)

The instantaneous withdrawal/deposit nature of those transactions is why this has never made any sense to me:

Take a dollar out of the flow and tuck it away as “assets”, and it is no longer in the current: It no longer flows.

I hear this kind of thing all the time. e.g. “Health-care spending is taking all that money out of the economy.” As you would say, “Nonsense!” 😉

You can’t “take a dollar out” of the bathtub (except by paying off loans to the financial sector, paying taxes to the federal government, or reducing the equity allocation in your portfolio hence driving down stock prices).

You can, however, reduce or increase the turnover of your stock of money in a given period. You can “hoard” or spend your money. Not-spending is indeed taking a dollar “out of the flow” (relative to the counterfactual of spending it) — reducing velocity. But in aggregate, not-spending doesn’t “tuck it away” any more than spending it does. If you spend it, it just ends up tucked away in somebody else’s account.

Spending vs. not-spending doesn’t change the amount of money in the bathtub. (Not directly or immediately, in an accounting sense. Increased turnover does have an economic effect over time: more spending causes more production, hence more surplus, more assets, which over time results in more money being created through 1. federal and private (bank-loan-financed) deficit spending, and 2. market-driven runups in equity values. That’s just describing a growing economy that needs and creates steadily more money.)

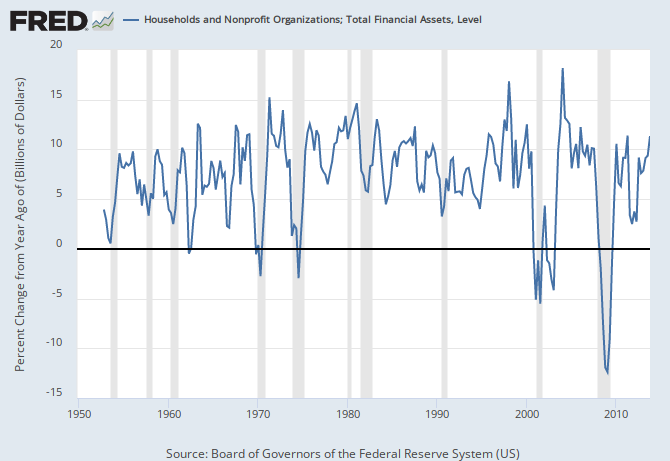

In the paragraph just before your graph, you seem to confuse two definitions of the word “real”. Here’s the offending sentence: We see this clearly when we look at recessions and the year-over-year change in real (inflation-adjusted) household assets — a measure of households’ total claims on real assets…

Both right and wrong.

Wrong: I intentionally use both meanings of “real” in that sentence, with no intention of obfuscation, trying to making clear through parentheticals which one I’m using. I should probably take my own advice and stop using real to mean “inflation-adjusted,” and just say “inflation-adjusted.” (As you’ve no doubt noticed, these dual meanings foment no end of confused discussion out there.)

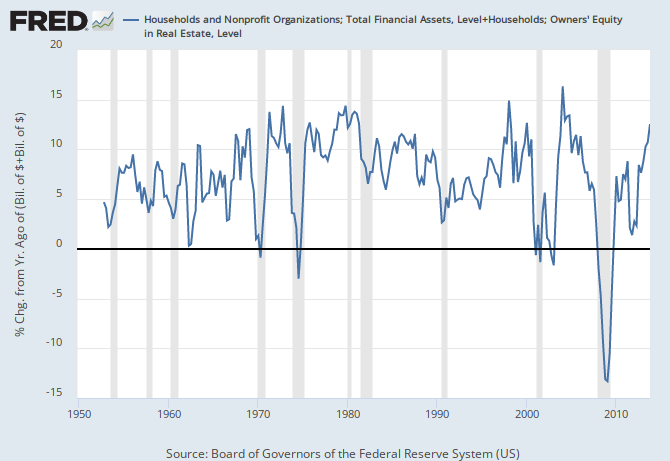

Right: I cheated. The graph of household assets vis-a-vis recessions is indeed inflation-adjusted, while my argument has been (implicitly) about nominal values. The correlation between recessions and YoY change in nominal household assets is still apparent, but considerably less firm (more false negatives and false positives). This whether or not you include household home equity as “financial assets” (click any graph to mess with it in FRED):

I have various notions about how to think about this, but haven’t formulated them into a clear and coherent explanation. This is problematic, but I don’t think it disqualifies the core conceptual approach.

But you also say that if we want to spend more, the money will grow to accommodate us. Your statements are contradictory.

No. Exactly not. I said that “transaction cash” (i.e. currency-like stuff), not money, will grow to accommodate us. See what you did there?

Further, if all financial assets are money as you say, then to calculate the velocity of money one would divide GDP by total financial assets. Not by total assets as you show in your second graph.

This brings us back to the real-estate issue discussed up top. When you ask someone “how much money do you have?”, IOW what are your assets, or your net worth, do they include their real-estate equity in their answer? Heck yes. Especially for low-income/wealth households, their home equity often constitutes a huge portion of their assets/net-worth/”money.”

I admit this can be tricky conceptual stuff given how we’ve always talked about money (the deep meaning of “ownership” aka claims aka credits enters here), but really: if house prices/values go up, people feel like they have more money (especially if increases exceed CPI, in which case they really do), and feel free to spend more (though not necessarily increasing their V) — just as they do when stock prices go up. And of course the reverse when values decline. The economic effects are very similar though probably not identical. (The effects are certainly slower-moving with real estate; people don’t track their house value day to day). Pretty straightforward wealth effect. The only question is the wealth-to-spending multiplier function (which is almost certainly nonlinear on more than one dimension).

I’ve been wrestling with this. Go back to Jesse Livermore’s wonderfully clear discussion of bonds/cash vs. stock/equity, how people’s portfolio allocations relative to the stock of bonds/cash is the primary (short- and arguably long-term) determinant of stock-market valuations (and in my definition, changes in the stock of money). Now add another “equity” class into which people are allocating: home equity.

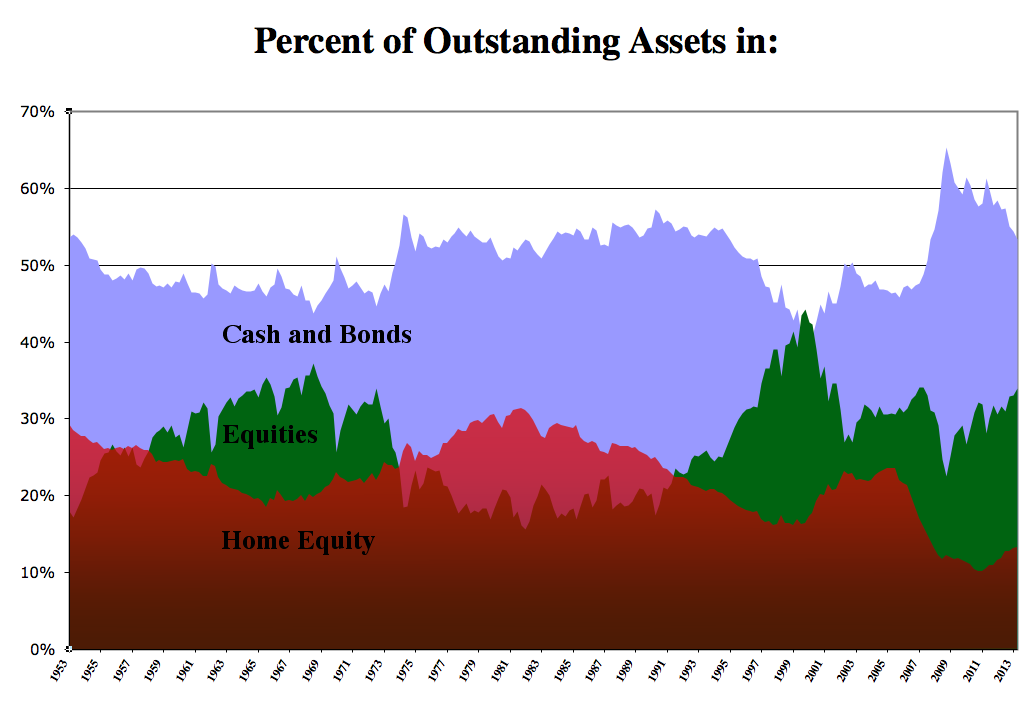

I pulled this chart — asset allocations into the three types of assets, over the decades:

Think about real-estate decisions: You can make a smaller down payment, and keep more money in stocks and bonds (effectively owning stocks/bonds on margin), or you can sell stocks/bonds and make a larger down payment, shifting your portfolio more into real-estate equity. Ditto with home-equity extraction for spending; you coulda sold bonds or stock and spent that money instead, and kept your real-estate equity allocation high.

In Livermore’s formulation, the key choice is between bonds/cash, and equity — whether that equity is in stocks or real estate. In my formulation, when people shift their allocation from bonds/cash to equity (either type), hence driving up prices, they’re increasing the stock of money. But that money ultimately has only two sources — deficit spending (reflected in debt outstanding), and animal spirits spurring the equity purchases. (High spirits are rooted, ultimately, in high and growing production and productivity, causing people to believe that all the real assets out there — which their financial assets are claims against — are actually more valuable than they thought).

I’m not quite sure what to do with this graph yet, but at the very least I find interesting the long-term secular decline in home-equity percentage since the eighties (with that valuation bump in the 00s). I’m thinking this is largely the result of increasing homeowner (mortgage) debt over that period — they borrowed more, kept their loan balances high and inflating both their own and banks’ balance sheets, hence holding more of their net assets in stocks and bonds/cash. More thinking to come.

Finally, I want to give an example to explain my contention that having a greater proportion of currency-like stuff doesn’t cause more spending as monetarists seem to believe (spending on real, newly produced goods and services, aka GDP stuff), while having more money (as defined by moi) does.

Say you’ve got a $100K portfolio as follows:

Stocks/equity: $60K

Bonds: $30K

Cash: $10k

Now the Fed under its QE program makes an attractive enough offer for your bonds that you sell them $10K worth. (That’s the only way they can suck up those bonds, by offering slightly more than private buyers are offering.) Your new portfolio:

Stocks/equity: $60K

Bonds: $20K

Cash: $20k

Are you going to go out to dinner more often because you now have more cash, even though you still have $100K?

Alternate scenario: the stock market goes up. Your new portfolio:

Stocks/equity: $70K

Bonds: $30K

Cash: $10k

You now have $110K. Will you go out to dinner more often? Quite likely. Some.

This works the same way if you add a fourth asset class, real-estate equity, and that goes up in value. You quite literally have more money — at least in my common-sense, uncomplicated, easily understood, straightforward, perfectly reasonable definition of money [grin] — so you’re more willing to spend money.

And yes: this explanation does serve to support what is to me a rather obvious conclusion — that greater wealth concentration results in less spending/velocity, because richer people spend less of their wealth each year. But that’s not the only reason I like it. I like it because it seems to really make sense.

I think that’s all I have to say at the moment. I’ll keep working on the inflation part of this thinking. Here’s hoping that Arthur has it all figured out for me.

Cross-posted at Asymptosis.

I’d say we should leave it up to empirical measures to determine what “money” is (of course interpreting those empirical measures is model dependent).

I came up with this model:

http://informationtransfereconomics.blogspot.com/2014/03/how-money-transfers-information.html

In the model, if you think money defines the price level, then money is literally physical currency. Other things like MZM and M2 trade against it at relatively fixed exchange rates:

http://informationtransfereconomics.blogspot.com/2014/05/do-monetary-aggregates-measure-money.html

The monetary base (including reserves) seems to primarily affect short term interest rates:

http://informationtransfereconomics.blogspot.com/2014/02/the-link-between-monetary-base-and.html

[xposted at Asymptosis]

mmm…

I’m missing the transaction costs, uncertainty analysis here. House equity is not at all the same as cash, because it is costly to extract and there is a risk that it is worth less than you think it is. Just adding it up is not what people do (although they do think about their net wealth for some decisions).

Might be relevant here:

http://stumblingandmumbling.typepad.com/stumbling_and_mumbling/2014/05/housing-vs-financial-wealth.html

@Reason:

Agree. I’d say it this way:

The economic effect of changes in housing wealth is at least different in timing — because of the things you mention and also because homeowners don’t look at their home values constantly or turn their houses over frequently — than it is with stocks. So also different in magnitude, at least over the same length of time. Perhaps also different in quality, not just quantity.

Or as I said it above: the wealth-to-spending multiplier function is almost certainly nonlinear on more than one dimension.

One of those dimensions would certainly be “type of asset(s) in which the wealth is held.”

I would also guess (cue: Prospect Theory) that wealth holders tend to react in different nonlinear ways to increases vs. decreases in different types of asset holdings.

To a Fisherman, a fish =money.

Steve,

I wanted to respond to you quickly, but I write slowly. So I compromised: I took longer than I wanted and wrote less than I wanted. Oh, well.

My response is up today:

http://newarthurianeconomics.blogspot.com/2014/05/income-money-value-wealth.html