Asset Reflux Disease: Explaining Koo to Krugman

Or: Why Banks Aren’t Like People

Steve Keen does a good job of addressing Paul Krugman’s befuddlement with Richard Koo’s balance-sheet-based thinking, here, with detailed models showing how funds flow and stocks change over time.

I’d like to address it more succinctly and I hope intuitively, by pointing out a simple misunderstanding that Paul shares with Scott Sumner, Nick Rowe, and many other very smart people who I don’t think have really internalized the notion of “endogenous money.”

Let’s start with Nick. I often spend years thinking about his posts. One that I’ve been worrying at forever, have read at least half a dozen times, is this one:

All money is helicopter money. Against the Law of Reflux

It’s about the idea that money supply in excess of what people want to hold “refluxes” to the issuer, which Nick doesn’t believe. (Emphasis here and throughout, mine).

This very old debate over the Law of Reflux is what is at the root of the very modern debate about whether Quantitative Easing can work.

Sounds important, right? Nick’s cutting to the crux, as is his wont.

I’ve finally decided that the post makes no sense at all, that all its very smart equilibrium thinking is obfuscatory rather than illuminative. Why? Because it’s based on a fundamentally flawed understanding:

The suppliers decide how big a stock [of money] will be held, regardless of the desire to hold it. People will pick it up whether they want to hold it or not. If they don’t want to hold it they will spend it, to try to get rid of it in exchange for something they do want to hold.

Ye Olde Hot Potato.

This is exactly the notion that Scott Sumner bruits here, calling it “the concept that lies at the heart of money/macro”:

Individuals can get rid of the cash they don’t want, but society as a whole cannot

And it’s the very notion that makes Krugman incapable of understanding Koo:

…an economy in which everyone is balance-sheet constrained, as opposed to one in which lots of people are balance-sheet constrained. I’d say that his vision makes no sense: where there are debtors, there must also be creditors, so there have to be at least some people who can respond to lower real interest rates even in a balance-sheet recession

Those people can respond, presumably, by borrowing more, and spending what they borrow.

Here’s why that doesn’t make sense: Nick forgot about option #2:

If households and nonfinancial businesses (the real sector) are holding more money than they want, they can use it to pay off debt to the financial sector. That money disappears.

Just start using your debit card instead of your credit card, and keep making your monthly payments (or more).* Voila: you’re returning money to the issuer. Nothing prevents everyone in the real sector from doing this at the same time. (Except the lure of low interest rates causing de-refluxing, but…how’s that working out for us? How did it work for us in the ’30s?)

{kind=link}

In terms both more precise and more broadly descriptive: loan payoffs by the real sector cause both real- and financial-sector balance sheets to shrink.

In Nick’s terms: The only thing those payer-offers get to “hold” “in exchange” for those payoffs is a reduction in their liabilities. Alert to the media: that’s not “spending.”

You know Krugman’s “patient” lenders? The technical term for them is “banks.” They’re not transparent intermediaries between real-sector borrowers and lenders. They are the lenders. And they’re nothing like real-sector actors:

1. They’re licensed to print new money for lending. And when it’s paid back they, collectively, burn it. Sound like your household?

2. Banks don’t lend (“save”) because they’re patiently “saving instead of consuming, deferring spending for the future.” Your credit-card company doesn’t lend less because it wants to spend and consume/invest more today. (Banks’ actual “spending” on newly-produced real goods and services is trivial in magnitude.)

Scott Fullwiler’s recent piece on banks’ capital/leverage structures and return-on-equity business models (wildly different from real-sector goods and services companies, not to mention households) does a good job of explaining what does drive banks’ lending decisions.

Here’s an inevitably imperfect metaphor: From the real-sector perspective, the financial sector is a magical, bottomless money-hole in the ground. New borrowing draws money out of that hole, and loan payoffs “retire” money back into the hole. Got reflux?

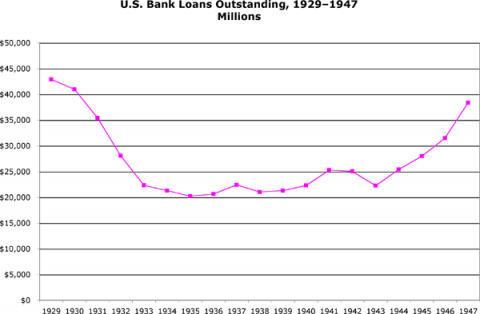

So yes: real-sector entities can all get rid of money at the same time. It’s called debt deleveraging, and the shrinking balance sheets that result (financial- and real-sector) are what Koo’s referring to in his discussions of “balance-sheet recessions.” (Maybe better termed “debt” or “deleveraging” recessions, per Fisher and Minsky.) This explains in quite simple terms why (as Steve Keen is so keen to point out) high real-sector debt levels make an economy so unstable: because all those real-sector actors can and often do stop spending at once, instead pouring that money back into the financial-sector money shredder/black hole.

When the impatient borrowers of the real sector go all patient on us, paying down their debt to banks, the banks don’t get impatient, or spend more, like Krugman’s imaginary counterparties.

And you’re going to have to get rather tortuous if you want to claim that more loan payoffs, less borrowing, means the banks do more lending (which would presumably lead to more spending…).

This is essentially the argument Nick’s making (and Paul’s assuming) with his equilibrium discussions — that “the” interest rate will adjust so that all those payer-offers stop paying off/start borrowing — de-reflux! See, they can’t all get rid of their money! “They [collectively] will pick it up [some will borrow more as a result of others borrowing less and lowering interest rates] whether they want to or not.”

This goes right back to the crazy “loanable funds” notion, that savers “fund” borrowers, and that people spending less (saving more) means other people can borrow more, at lower rates. I’ve taken to calling this The Lump of Money Fallacy. (Dean Baker told me once in person that Paul “doesn’t believe in loanable funds.” I’m finally feeling confident enough to respectfully disagree. IS/LM is all about the logic of loanable funds, even while acknowledging that banks create new money for lending. Schizo?)

This interest-rate-equilibrium notion is obviously problematic at the zero lower bound, where rates can’t go low enough to lure payer-offers into becoming impatient borrowers. But Nick also knows, I think, that elasticity complexities in many different (and interacting) credit markets, at many rates, under many different conditions (both “natural” and “government-imposed” conditions) make that de-reflux rather a long-term pipe dream. Credit-card rates went up ’08-’10, for instance (lots relative to the Fed Funds rate, which dove), in the midst of massive real-sector deleveraging, a.k.a. low borrowing demand, a.k.a. everyone getting rid of money at the same time.

{kind=link}

Nick and Scott: Households and nonfinancial businesses — the real sector — can all get rid of money at the same time. People should stop suggesting that they can’t.

And Paul: For every borrower, there’s…a bank.

Finally, I can’t resist pointing out: a very smart and very curious Nick Rowe, who blesses us regularly with his knowledge of economists of yore, felt the need to write a very lengthy post worrying at this “very old debate” that is central to “whether Quantitative Easing can work.” And Scott says “the concept [though not the word] lies at the heart of money/macro.” Sounds important, right? Worth knowing what people have thought and written about it over the decades and centuries, no?

Now search Scott’s site for this word, and also that of Lars Christensen, who coined the term “market monetarist.” How many hits?

Count ’em: zero.

And Krugman? His one usage is referring to a different kind of reflux.

I’m sure glad Nick brought it up.

——————

* Question for monetarists: Is your unused credit-card limit “money”?

Cross-posted at Asymptosis.

I guess in simple terms this “The suppliers decide how big a stock [of money] will be held, regardless of the desire to hold it.”

would mean there is no need to set reserve amounts that banks must hold?

Where as, the way I understand banking, they’ll lend out every last penny and then create some pennies beyond the last one sold via slice and dice of what they lent out.

But, then Krugman et al must be thinking in terms of the under-the-table market model where I actually loan the money I earned to you if I can afford it. Hopefully you pay me back unless you’re a great friend and just simply needed it. But that would be charity and I don’t see that type of spending in their models.

I forgot, what about write offs? Or do we just consider they no longer exist now that we have bailouts and “too big to fail”?