JzB Smackdown with Some Thoughts on Trends and Context

João Marcus Marinho Nunes is personally offended by my previous Angry Bear post.

Personally I was ‘offended’ by being ‘accused’ of “using short-time series data”, ignoring “what is a valid context” and “cherry picking”.

Which was odd, since I didn’t accuse him of anything. In fact, he wasn’t even on my radar screen. He then goes on to show a bunch of nice and interesting graphs that have nothing at all to do with my point, and concludes:

PS Maybe JazzBumpa thinks he´s a modern day Robespierre fighting against (in this case imaginary) absolutism!

Actually, I’m pretty close to agnostic on the subject of Market Monetarism, – as he identifies the subject of my (imaginary) absolutism in his comment at my post. I thought I had made it pretty clear that what I was criticizing was the kind of confirmation bias that induces one to construct questionable data analyses that support pre-concieved conclusions. The fact that the people doing this were market monetarists might be illustrative, but is not really central to my criticism.

I welcome disagreement, but it’s more helpful and constructive if the points of disagreement have some relevance to the point I was trying to make. I elaborated a bit in a comment at Nunez’s blog, which you can read there, if you’re interested. What interested me was some piling on by Mark Sadowski, in comments both in my post and at Nunes’. While I think Sadowski missed [or perhaps ignored] my point, he makes a couple of his own – one of which is actually Krugman’s, whom he quotes.

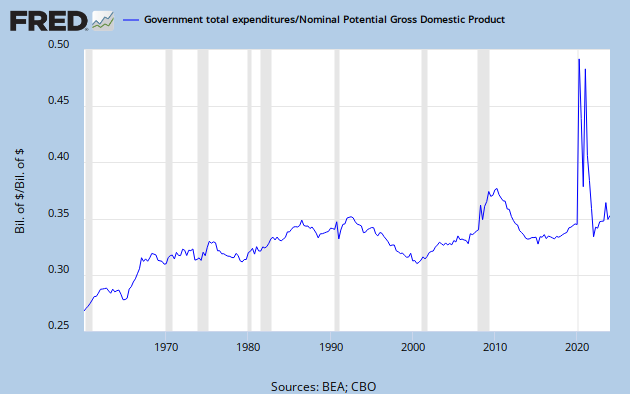

“…To see what’s going on, you need to do two things. First, you should include state and local; second, you shouldn’t divide by GDP, because a depressed GDP can cause the spending/GDP ratio to rise even if spending falls. So it’s useful to look at the ratio of overall government expenditure to potential GDP — what the economy would be producing if it were at full employment; CBO provides standard estimates of this number. And here’s what we see:

Spending is down to what it was before the recession, and also significantly lower than it was under Reagan.

I don’t always disagree with Krugman, but when I do I prefer to look at a longer time series [My Graph 1.]

{kind=link}

My Graph 1 – Total Gov’t Exp/Potential GDP

My first thought is – do you really want to use that profligate spendthrift St. Ronnie as your benchmark? Second thought is – yes, Total Gov’t Spending/Potential GDP is dropping like a rock, but it’s still higher than almost all of the historical record, and far exceeding values from the Viet Nam era and LBJ’s Great Society. In fact, eyeball a line through the local minima, and you can see a return to the trend boundary that is only slightly steeper than those of the Clinton and Carter eras. I don’t recall anyone talking about austerity in those days.

Here is Sadowski’s excellent other point.

It’s not the level of spending that matters but the change in the level of spending relative to trend.

So, here is my question: What is the right historical time frame to determine your trend and define your context?

I don’t think there is a simple one-size-fits all answer. Let’s have another look at this data, with a high level trend channel outlined [My Graph 1.1.] The method is simply to connect peak to peak and trough to trough to construct the green lines. The red line extensions are arbitrary estimates. The yellow midine was constructed by taking an average of these boundary values for each date.

This view suggests a couple of things. First, the data oscillates around a line approaching an asymptote somewhere near 0.35. Second, the recent decline is nothing extraordinary – just another excursion from one boundary toward the other. Still, a trend is only a trend until it isn’t. The first signal that the trend is caput is a serious violation of the trend boundary. That would require a drop below about 0.315.

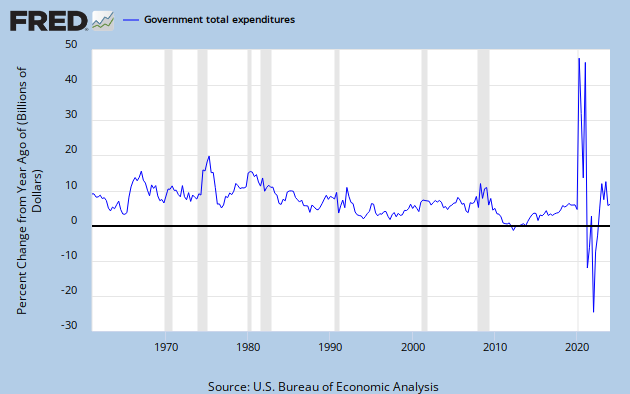

Let’s look at the change in Total Government Spending without a GDP denominator, expressed as YoY % Change [My Graph 2.]

What trends do you see here? I see an upward trend in the first 15 to 20 years of the data set, then a long decline. Each of these top level trends also includes alternating sub-trends going either with or against the flow. My Graph 2.1 shows this in detail.

I’ve placed parallel trend boundaries around what I see as major

secular trends. Green lines identify the upward trend and brown lines

identify the downward trend. Also included are horizontal lines representing period averages. The purple lines are pre- and post-1981. Blue lines are the Carter and Clinton presidencies. Red is G. W. Bush. Each president’s time is considered as year two of his term to year one of the following term, inclusive, since each year’s budget is set in the prior year.

The up-trend that started before the beginning of the data set, probably in the 30’s, peaked in Q2, ’75 at 20.9%. It’s followed rather quickly by an anomalous low of 5.4% in Q4, ’76. This is the first suggestion that the trend might be ending. The next peak, Q1 to Q3, ’80 hits 16.2%, significantly below the prior peak, and consistent with a new downward trend. The death of the old trend is confirmed by the lows of 9.7% at Q1, ’81 and 6.2% at Q3, ’83

A counter-current decline [not marked] occurs from Q1, ’67 to Q3, ’73. A counter-current increase, outlined in green, occurs from Q1, ’98 to Q3, ’08. After that, despite the stimulus and the advent of Obama/Romney/Heritage Foundationcare there is quite a sharp decline in spending growth [not spending, per se.]

What do you make of it? It’s the lowest spending growth on record, now hovering near zero. Clearly, this is a big change from the ’98 to ’08 trend. But that decade was just a counter-current move against the multi-decade declining trend.

These things are close to impossible to identify in real time, but I think it’s now pretty clear that there was a sea change ca. 1975-80, though it would be tough to tie it down more precisely. But I don’t believe there was a sea-change to greater spending growth in the late 90’s, though that move doubled the width of the trend channel. What we’ve seen since is a move back to the middle of the expanded downward trend channel. You don’t have to squint very hard to see a trend center-line tendency throughout the data set. Note also that reversions typically occur at the midline or a channel boundary.

So, is what we’ve experienced post-recession a new austerity, or simply the continuation of a long-established trend? Or, perhaps, you might see this entire trend exercise as a flight of fancy. What do you think? Why do you think it?

Just to be clear, I am not saying that we don’t have austerity. The growth of total government spending has been in decline for three decades. I am saying that austerity is not simply definable in an absolute on/off sense, but exists along a continuum. In my view, austerity is not extreme until spending growth goes negative. Do you agree?

To go back to my original point, GDP is a resultant of many inputs, Monetary policy is one, and fiscal policy is another. To say that anemic GDP growth in an era of relative austerity [and extraordinary monetary policy] disproves the efficacy of fiscal policy is to deliberately look at only a small part of a big picture.

“While I think Sadowski missed [or perhaps ignored] my point, he makes a couple of his own – one of which is actually Krugman’s, whom he quotes.”

I ignored it because nitpicking is my specialty.

Neither I, nor Beckworth, nor Nunes are debating the lackluster nature of this recovery. (On the contrary, Nunes loudly complains about it every other post.) The point is fiscal policy has been enormously contractionary since at least 2010 (by some measures the most since 1953-56) and something has been offsetting it.

P.S. You misspelled my name when you quoted me.

Mark –

Corrected the typo. Sorry, I really hate doing things like that.

I don’t see what you say as being Beckworth’s point. I’ll quote him again, as I did in my original post.

Back on Feb 10, Beckworth said: “despite this austerity happening at a time of high unemployment and a large output gap, a slowdown in aggregate demand growth has failed to materialize.”

I went on to show that this is not correct.

I really have no bone to pick with either you or Nunes. I’m both amused and bemused by Nunes’ reaction.

But I will also pick a nit a couple of nits. First – what in the world did Nunes’ post have to do with mine? I’m genuinely puzzled.

Second, Government spending is flatish. This is not expansionary. If you want to say moderately or relatively contractionary, I won’t quibble. But, in my view to be enormously contractionary requires either actual spending reductions YoY or at least growing surpluses, as was the trend in the 20’s.

We don’t have anything like that now. In fact, current spending is, at worst, no less than it would have been if the trend of the previous decade had simply continued.

http://research.stlouisfed.org/fred2/graph/?g=jlv

Thanks for reading and commenting.

JzB

“I went on to show that this is not correct.”

Actually you didn’t contradict Beckworth. You just showed that this is an anemic recovery (sorry, but duh).

Beckworth is claiming that AD growth has been steady despite fiscal contraction which it has. In fact the standard deviation of the quarterly growth rate in nominal GDP (NGDP) since 2010Q1 is by far the lowest for any 13 quarter period on data going back to 1947. Many Fed watchers have been stunned by the amazing steadiness of the NGDP numbers despite all the various fiscal policy shifts (or cliffs) and this raises serious doubts as to the existence of a liquidity trap.

As for Nunes he rightly prides himself on his graphs and for some reason felt an attack on Beckworth’s graphs was an attack on his.

Now in the meantime, I’ve had a chance to read this post and there’s numerous problems with your analysis.

First of all your Graph 1.1. Even assuming those trends are correct, consider the following. We’ve passed 70% of the way more or less from the top band to the lower band in three years. We passed from the top to the bottom from 1968 to 1979, a period of 11 years. We did the same from 1986 to 2000, a period of 14 years. The rate of fiscal consolidation matters greatly.

The problem with your Graph 2 and and 2.1 is that you’re switching back to nominal values without any consideration of the underlying economic trends. Why not compute year on year rates of change of the data in Graph 1.1? You can easily do that in FRED.Personally I don’t think it tells us anything that Graph 1.1 doesn’t already tell us.

Now the BEA doesn’t actually provide Total Government Expenditures for before 1960 but it’s easy to compute it from the source data and what it reveals is the decline in Government Total Spending as a percent of potential NGDP over the last 11 quarters has been the greatest since 1956Q3 as a percent of peak spending share (8.8%), and has been the greatest since 1956Q1 as a percent of potential GDP (3.2%).

Now, is this the best measure of fiscal consolidation available? Absolutely not. It’s useful because such data goes all the way back to WW II and it comes in quarterly frequency. The biggest problem with it is that takes no account of the revenue side of things.

Probably the best measure is the IMF’s general government “cyclically adjusted primary balance” which can be found in the Fiscal Monitor. But it is available only in annual (calendar year) frequency and only goes back to 2006.

But the IMF also produces general government “structural balance” which goes all the way back to 1980 for the U.S. Unlike the cyclically adjusted primary balance it doesn’t take into account changes in net interest, however as the word “structural” implies it does take into account the business cycle. It can be found in the World Economic Outlook.

So since the structural balance is adjusted for business cycles any changes in it can be interpreted as representing changes in fiscal policy stance. And in fact it is the changes in the structural balance, not the structural balance itself, that matters, since that is what is supplying the fiscal policy impulse.

What the data shows is that general government fiscal policy stance was expansionary during 1981-86, 1990, 1992, 1999, 2001-03, and 2007-10. The largest increase in structural balance (the most fiscally austere) on record is 2012 (1.31% of potential GDP) and 2013 forecast to be worse (1.75% of potential GDP). The change in the structural balance during 2011-12 (2.11% of potential GDP) is the largest over any two year period. The forecasted change during 2011-2013 (3.86% of potential GDP) is the largest over any three year period going back to 1981.

If you want to focus on just the Federal budget the CBO publishes estimates of the cyclically adjusted federal budget balance which can be found in something called “The Effects of Automatic Stabilizers on the Federal Budget”. It was more clearly labeled until 2011 but I have a theory that the whole idea of cyclically adjusted Federal budget balances was sending the Republican House leadership into an apoplectic fit.

The March 2013 issue has cyclically adjusted Federal budget balances all the way back to fiscal year 1960. The change in the cyclically adjusted Federal budget balance during 2010-12 is 2.8% of potential GDP. The only larger change in the cylically adjusted balance in a period of three years or less is the one following FY 1968 which was 3.0% of potential GDP in 1969 alone and 3.3% of potential GDP during 1969-70. However the forecasted change during 2010-13 is 4.6% of GDP and is easily the largest Federal fiscal consolidation during any four year period on records going back to FY 1960.

Mark –

Thanks again for your thoughtful comments. There’s a lot here, and it will take me some time to digest it.

In all due respect though, I don’t see how someone can look at this statement: “a slowdown in aggregate demand growth has failed to materialize” and the following linked graph and not think something is wrong.

http://research.stlouisfed.org/fredgraph.png?g=j2q

As for low standard deviation – tiny numbers give a low std dev. That shouldn’t be a huge surprise, but it’s something I’ll have a closer look at.

Cheers!

JzB