If I Were Looking for Structural Changes…

…I would not be likely to find them. But at least I know how to look. Start at the macro level and see if there is a noticeable shift in revenues:

|

| Source: BEA |

I decided that anything that didn’t have at least a 0.3% change in its effect on GDP over three years could not be defined as a Structural Change, especially by the people who claim a priori that the change is structural. This may be giving them too much credit, but that’s how we roll here in Dataland.

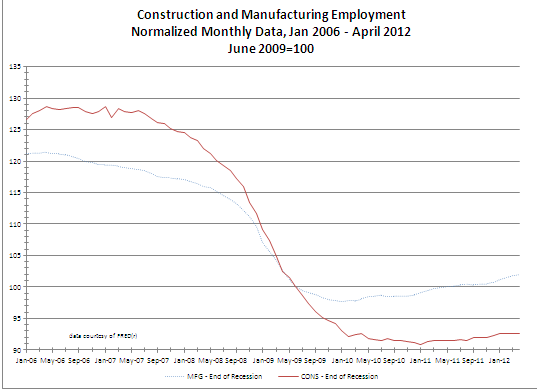

There are two basic areas that show effectively neutral shifts. The first is that there is a decline in Construction that is matched by a rise in Manufacturing.

If we look at employment in Construction, it peaks (as one might expect) in April of 2006. (Employment in Manufacturing in the United States peaked in June of 1979.)

If we normalize both Construction and Manufacturing to that peak, we might expect that Manufacturing hiring would increase while Construction hiring would decrease. (Indeed, having chosen the maximum point in Construction Employment to be early in the graphic, the general trend in Construction becomes inevitable.)

As expected (by definition, as it were), Construction plummeted, and now appears to have “leveled off” in the range of a 25-30% decline from its peak. But Manufacturing, even as it represents the shifted share-of-GDP also plummeted and has “recovered” only to about a 15% decline since the same point. So let’s see if we can see the shift if we measure employment in the two areas using the NBER-designated “trough” of June 2009 as our baseline. Then we have:

What we see here is that, while there has been a GDP ratio shift, there is not a notable hiring trend–an increase of less than 2% in nearly three years–certainly not enough of a trend (even adjusting for the difference in employment totals) that we can say that there is unsatisfied demand in the Manufacturing sector. And that is from a “trough” in the economic cycle.

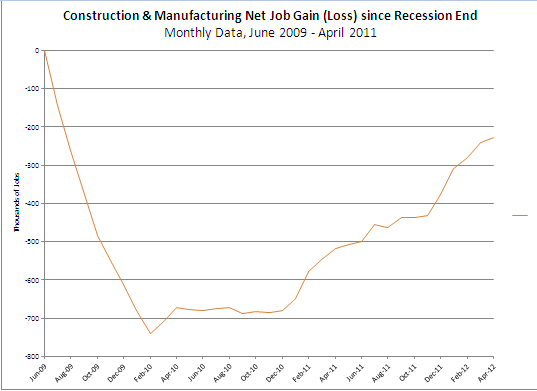

Looking solely at the net change in employment between the two sectors since the Recession ended makes it clear that there is a lack of demand, not supply:

.

As Johnathan Portes (h/t Brad DeLong) notes (of the UK, but the U.S. situation is the same)

“with long-term government borrowing as cheap as in living memory, with unemployed workers and plenty of spare capacity and…suffering from both creaking infrastructure and a chronic lack of housing supply, now is the time for government to borrow and invest. This is not just basic macroeconomics, it is common sense.”

I disagree with the borrow-our-way-back-to-prosperity idea.

It is just injecting adrenalin for a sucking chest wound.

The economy of 2002-2006 was a fake one, driven soley by consumer debt take-on:

http://research.stlouisfed.org/fred2/series/CMDEBT

or, more clearly, looking at annual consumer debt take-on over wages:

http://research.stlouisfed.org/fred2/graph/?g=7c6

showing that households were borrowing 20% of wages during the peak years.

This was a stealth stimulus that was simply unsustainable.

it drove our massive trade deficit and allowed millions to consume without having any wealth-creation to pay for it.

Now, if we could borrow to increase the productivity of this nation — “infrastructure” etc — that would be great.

But the problems this country faces are of our own making, really. Taxes are way too low and wasteful government spending is way too high. (Thanks, Ralph!)

Denmark and Sweden do not necessarily enjoy their very high tax to GDP ratios, but they pay them, and their economy is more sustainable thereby.

It makes no sense to manufacture anything here that China can make, given the order of magnitude difference in wages.

But the issue with the China trade is the $300B+ annual deficit that is coming with it, this is ripping velocity out of the paycheck economy.

Velocity is also being lost thanks to the massive rents in housing and health care, $500B/yr in housing and three times that in health sector.

This is loss of velcity is also visible in corporate profits:

http://research.stlouisfed.org/fred2/series/NFCPATAX

The System is running on tilt now.

Troy should write a song based on that old union song: “I’m Sticking To The Union” with a title; “I’m Sticking to Austerity”. Or even that one: “Solidarity Forever” only “Austerity Forever”. It would be fun to sing.

The borrowing Ken recommends is not, I think, for the purpose of plumping up the financial economy, but for the dual purpose of a) keeping Americans employed, and thus preserving their physical, mental and financial health, and b) using the excess capacity to do badly needed nation-building, infrastructural and demographic alike.

To force millions of people to wait for the “real jobs” the private sector portions out, in a system where employment is the only way for citizens to access a livlihood, is to sacrifice their energy and ability to an abstraction. It’s not only unworkable, but inhuman.

My preferred solution would be to return to Clintonian taxation for starters.

Cut the DOD expense in half.

Start raising medicare taxes.

Phase-out the deduction of interest, first for high incomes, then for all.

Insisting we have the taxation to pay for our government outgo is not ‘austerity’. It’s rationality.

Employed doing what?

What wealth and infrastructure does this country need?

If I were running things I’d spend $100B/yr building quality multifamily housing (on the nordic model) all throughout the nation. At a capital cost of $200,000 per unit that’s 500,000 units per year — 800 units per 500,000 people. I’d do that for 10 or 20 years until rents collapse in all areas where there’s a supply shortage.

The less money we’re forced to pay in ground rent the more we can pay for actual needs.

But, to be honest, I do wonder if such public housing would just end up totall fubar like the postwar colossal mistakes. This ain’t Sweden, and we aren’t really Swedish, alas.

I was thinking it’d be great if all mass transit — schoolbuses, taxis, and metro buses — ran on natural gas instead of diesel. Diesel sucks. While I don’t know how long our oversupply of natgas will last, it’s a decent energy delivery system at least.

And aside from that, maybe we can start working on smart transportation grids to reduce the waste in time and fuel in getting around town. Traffic shaping, inter-car communication. I think it’s a lock that later this century we’ll all have google cars driving us around, a la Minority Report.

Our $900B/yr defense expense is worse than just lighting that money afire. At least we’d get deflation if we did that.

But my larger point in my original was that the economy of 2003-2006 was a total sham economy. We can’t go back to that, that was just an artifact of households cashing out $1T+ in phantom home equity, $10,000/yr per household for 3-4 years.

Now, maybe we need a healthy dose of inflation to get the yuan down (up?) to 3 and the euro back at parity. I think that’s the solution the system is searching for, but with that solution is $10 gasoline, something our economy is not presently structured to adjust to all that gracefully.

Troy –

You fail to distinguish between public and private debt.

Ken is calling for federal borrowing to adress infrastructure issues – which are serious and growing.

Consumer debt overshadows fed debt – which is where he borrowing should be.

http://research.stlouisfed.org/fred2/graph/?g=7ev

Cheers!

JzB