GDP and Housing

On Friday, the BEA reported GDP (advance) for the third quarter 2005. The BEA reported that Residential Investment was still robust at an annual rate of $761.5 Billion or 6.05% of GDP.

The following graph shows Residential Investment as a % of GDP for the last 40 years. The booms and busts of the housing cycle are very clear. Note: 2005 plotted at Q3 2005 percent of GDP.

Click on graph for larger image.

Residential investment as a % of GDP really took off in early 2003. Based on fundamentals, UCLA’s Dr. Thornberg argues:

… housing prices should have basically gone flat as of Q4 2002, and instead they have grown at an unprecedented pace. … we can guesstimate that property in California is now overvalued by something close to 35 or 40%.

I expect that Q3 Residential Investment will be the peak of the current housing cycle. This prediction is based primarily on rising inventories and slowing sales, but also on other factors like rising interest rates, the extensive use of ‘exotic’ mortgages (speculation), the negative savings rate and record household debt service and financial obligations ratios, even with low interest rates (See: Federal Reserve DSR and FOR).

How soon will the housing slowdown impact the overall economy? Dr. Thornberg argues that typically a housing slowdown spills over into the overall economy “within three to six quarters” after “inventories rise and sales start to fall”.

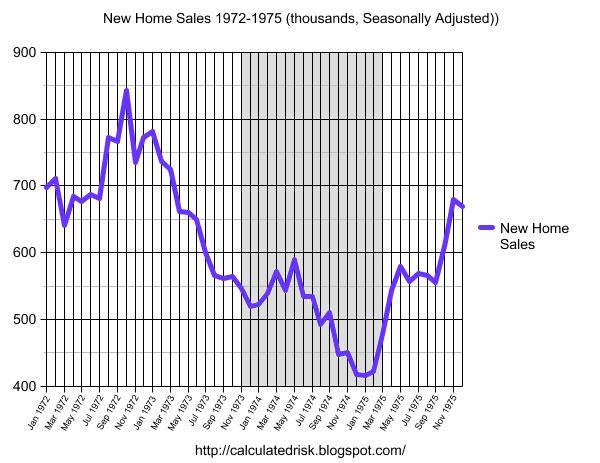

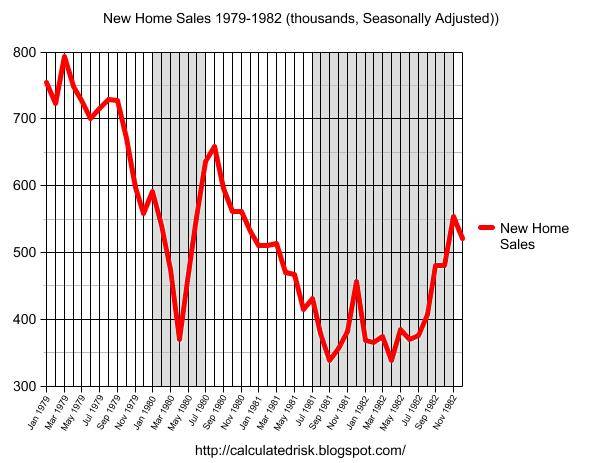

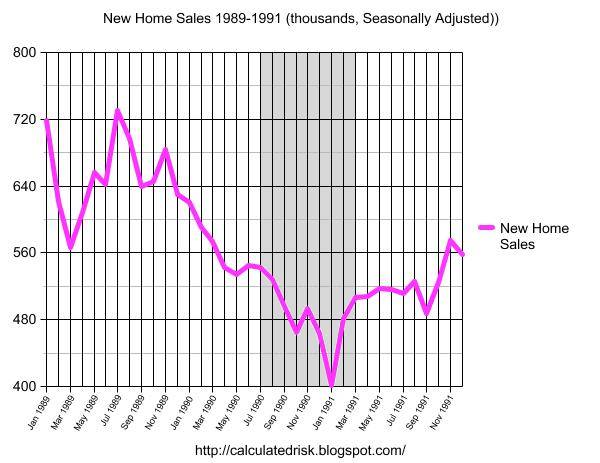

The following three graphs show New Home Sales and the last three consumer recessions (four counting the ’80s double dip). The gray area signifies that the economy was in recession based on the National Bureau of Economic Research’s cycle dates. Note: the graphs do not start at zero to better show the change in sales.

The previous housing slowdowns appear to support Dr. Thronberg’s view of a three to six quarter lag from the peak of the housing cycle to an impact on the overall economy.

For the current cycle, it appears housing sales peaked in July 2005.

Best Regards, CR Calculated Risk