New Deal democrat’s Weekly Indicators for July 6 – 10, 2026

My “Weekly Indicators” post is up.

The high frequency data continues to confirm my Big Picture outlook that after a near-miss or possible “mini-recession” late last year, the economy is rebounding. In particular, the YoY improvements, already Booming, in consumer spending are accelerating even more. Some of this is probably the wealth effect from stock portfolios, and some may be big tax refunds to upper income households due to last year’s Billionaire Bust-out Bill.

As usual, clicking over and reading will bring you up to the virtual moment as to the state of the economy, and reward me for putting it all together for you with a little gas money for summer excursions.

Some more data this week: Weekly Indicators:

Consumer Spending Continues to Blow Its Stack”

Jul 11, 2026 08:00 AM | State Street SPDR Dow Jones Indust Avg ETF Trust(DIA) | By: New Deal Democrat

- All timeframes remain positive, with no recession signals across long leading, short leading, or coincident indicators.

- Yield curve steepening and robust corporate profits are primary long leading supports, while the leverage index warrants ongoing caution.

- Short leading indicators are buoyed by stock market highs, low jobless claims, and positive manufacturing and service activity.

- Coincident data highlights exceptionally strong consumer spending, though tax withholding has been weak for three consecutive weeks.

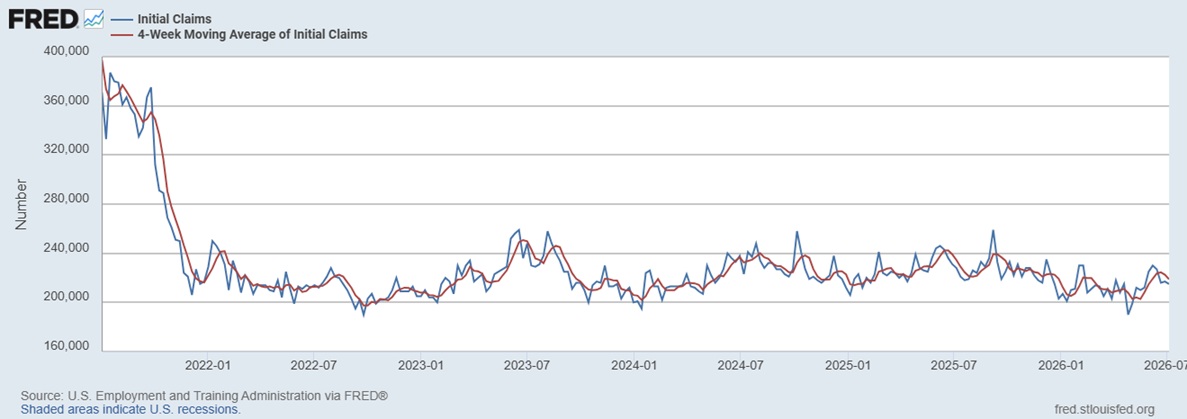

Initial jobless claims

- 215,000, down -2,000 w/w, down -5.7% YoY.

- 4-week average 218,750, down -3,750 w/w, down -6.7% YoY.

(Graph at St. Louis FRED.)

Jobless claims were positive for most of 2025, except for hurricane-influenced weeks during the autumn. Then they turned moderately negative through midyear this year. But since the beginning of last July, more often than not, readings have been lower YoY, generally turning this metric positive. They may be affected by the disappearance of some immigrant employees.

All time frames continued positive again this week.

Among the long leading indicators, positive term spreads in the bond market plus booming corporate profits remain the driving forces. Yield spreads steepened again this week, mainly as long rates rose. The leverage index continues to be one source of longer-term concern.

The short leading indicators also continue to be positive, driven by stock prices and very low new jobless claims. The manufacturing and services regional Fed indexes are positive, confirmed by the monthly ISM manufacturing and services indexes. Commodity prices firmed, which may be a byproduct of renewed hostilities in the Middle East. Meanwhile, for the fiftieth week in a row, gasoline usage was negative.

The coincident indicators continue to show *very* strong consumer spending, while tax withholding was weak for the third week in a row.