Income Driven Student Loan Repayments

All three of mine had student loans which they were capable of repaying. At the same time, we pitched in to pay for them off too. Student loan are like dead weight. They are with you until death. On the other side of the spectrum, there are many other examples of business entities being granted relief from loans. Both Biden and Trump forgave business loans after a recessional period. Trump’s plan is smaller payments and eventual relief.

There must be something unique about young students which exempt them from loan forgiveness. This does take away from the nation’s productivity.

“All Student Loan “Income-Driven Repayment” Plans are Cruel, Life-long Jokes”

– by Alan Collinge

Both existing- and proposed- plans disqualify the overwhelming majority of borrowers out.

Since 1995, a confusing array of Income-Driven Repayment programs (IDRs) have been foisted on the public by the Department of Education for federal student loans, each promising to cancel student loan debt after borrowers pay based upon their incomes for varying time periods. These include Income Contingent Repayment (ICR), Income Based Repayment (IBR), Pay-As-You-Earn (PAYE), and Revised Pay-As-You-Earn (REPAYE), and most recently, President Biden’s ill-fated “SAVE Plan”, which was, hilariously, a “revised” version of the “Revised Pay-As-You-Earn” plan. The Public Service Loan Forgiveness Program (PSLF), while not technically a repayment program, is also mixed into this alphabet soup.

Confused yet? It gets better. There is now yet another IDR in the offing from the Republicans, dubbed the “Repayment Assistance Plan” (RAP), which is slated to become law and replace several of the existing plans (ICR, PAYE, REPAYE) with the passage of the “One, Big, Beautiful Bill”.

Reader: Do not be afraid! I will not abuse you by taking you through these programs in detail. I’ll leave that to the legions of “student loan lawyers”, student debt coaches, counselors, and other predators who profit (at the borrowers expense) by baffling and bamboozling vulnerable and desperate borrowers into loan rehabilitation, consolidations with the carrot of what these IDR plans promise as bait.

Thankfully, there is no need to try to navigate this hopelessly complicated labryinth, because these plans all share a common characteristic that make further analysis unnecessary:

All of these IDR’s are being run by a Department of Education which has no desires or intentions of cancelling any loans. The vast majority of borrowers are being expelled from the programs, and will not only not be getting the loan cancellation promised; they will be left owing far more than had they never tried in the first place.

The Chronicle of Higher Education reported in 2015– under the Obama-Biden Administration- that 57% of those enrolled in IDR programs had been disqualified in one year alone for failure to “verify their income”, an annual, onerous exercise required of the borrowers- and one of many ways the Department has to disqualify people out of the programs. Given that around 30% of the income verification forms are rejected in a typical year, simple calculation shows that the probability of making it through 20 consecutive years shrinks to 0.08%- a vanishingly small percentage. This goes even lower for 25-year terms.

Also: of millions of people who enrolled in the Income Contingent Repayment Program (ICR) since 1995, only 32 people had made it through as of 2021. For the Public Service Loan Forgiveness Program (PSLF), the disqualification rate was 99% as of 2018.

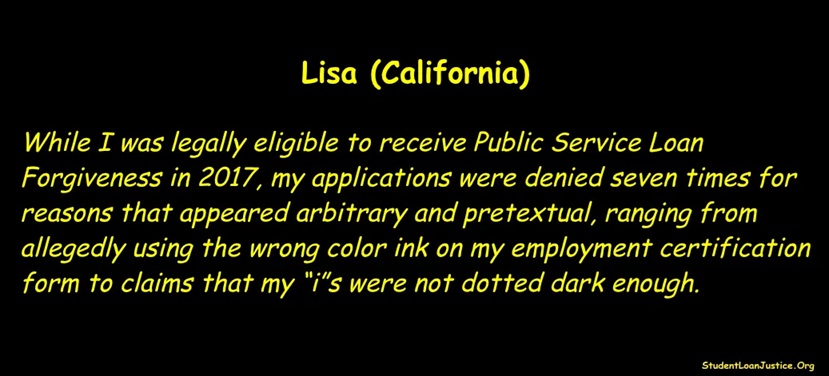

Some people saw their annual recertification forms rejected, literally, for not “dotting their I’s”. on the paperwork. This, from Lisa in California:

This is debt peonage.

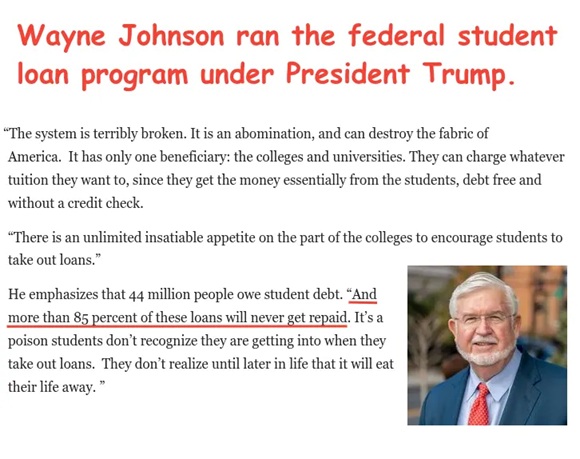

According to A. Wayne Johnson, who ran the federal loan program 2017–2018, 85% of all borrowers will never be able to repay their loans.

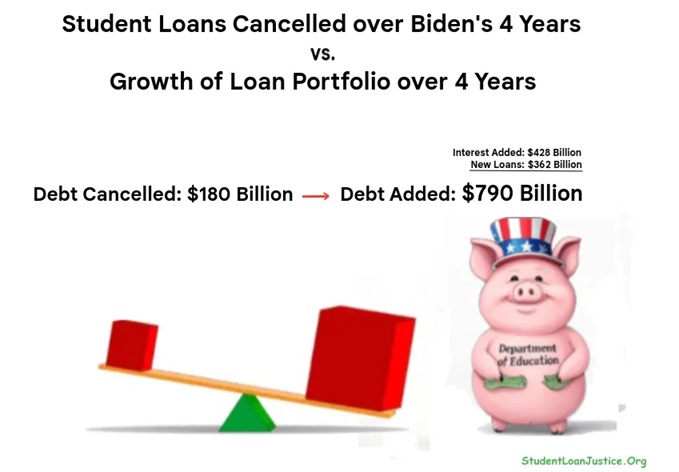

On Joe Biden’s watch, loan cancellations through the various IDR’s increased somewhat, but the impressive-sounding $180 Billion in cancelled debt on his watch (mostly through the PSLF program) still pales in comparison to the growth of the federal student loan portfolio over 4 years (Covid pauses notwithstanding).

The Department of Education could do loan cancellation like what we saw under Biden forever, and with interest and new loan originations, the federal student loan portfolio would still grow by about $1.6 Trillion over ten years.

But it almost surely won’t. On Trump’s watch, it is obvious that we’ll go back to the “bad old days” where the Department will get back to disqualifying the overwhelming majority of borrowers out of the IDR’s, and processing of loan cancellations will- like during his first term- come to a grinding halt. Particularly as he injects more chaos into the fray by falsely claiming to be shutting down the Department of Education, moving the administration of the loans to the SBA (another false claim), and otherwise letting the predatory student loan sharks in Washington do what they want with this already failed, collapsing loan scam, where the large majority of borrowers are now unable to make payments.

A cruel irony: Most people enrolled in IDR’s have increasing loan balances throughout the term of their repayment. When they are disqualified out of these programs, they are usually left owing a far larger balance than had they never tried in the first place. At least on the books- the Department of Education is almost surely booking a profit rather than incurring a cost due to these non-functioning IDR plans. The cost and harm that these vicious, predatory IDR’s have caused the citizenry has been incalculably large.

The Department of Education clearly has no desires or intentions of actually cancelling any loans if a reason can be found not to, and this has always been true. The bad faith with which the Department runs this lending program has been obvious for decades.

Since the constitutional right of bankruptcy protection was stripped uniquely from the loans, they have become increasingly predatory, hyper-inflationary, and the institutional culture of administering the loans with an eye towards disqualifying as many borrowers out of the IDR’s as possible has only become more vicious and blatant.

This problem solves itself with the return of standard, constitutionally enshrined bankruptcy rights. With the threat of bankruptcy returned to federal student loans, however, this bad-faithed, cruel administration of the lending program will be forced to end at long last. Just the threat of bankruptcy- without anyone actually having to file- will compel the Department of Education and Congress, pre-emptively, to:

- Immediately stop all the bureaucratic tricks and traps being sprung on borrowers enrolled in the various IDR plans, where currently, the vast majority are being baffled and bamboozled endlessly, and the vast majority are ultimately disqualified out of the programs.

- Restrain lending, push the colleges to lower their prices to rational levels, decrease the time to graduate, increase the quality of the education they provide.

- Act to prevent defaults, rather than encourage them.

- Lower interest rates.

- Negotiate fair and reasonable workouts with borrowers whose lives have been wrecked for their entire adult lives due to this debt.

- Clear old, uncollectible debt.

- Behave with a minimal level of good faith as other lenders must for all other loans.

As demonstrated, the Department fights tooth-and-nail behind the scenes to keep constitutional bankruptcy rights away from the loans, and this has not changed with the “new” bankruptcy process announced last year. As long as this vital protection remains gone, the un-elected, un-appointed bureaucrats there will continue to abuse the borrowers, extract obscene- and ever-increasing amounts of unearned profit from them.

This never-ending parade of designed-to-fail IDR’s only perpetuates this unconstitutional, catastrophically failed loan scam into the future, and quite frankly, looks very much like indentured servitude at this point, which, along with slavery, was outlawed in 1865.

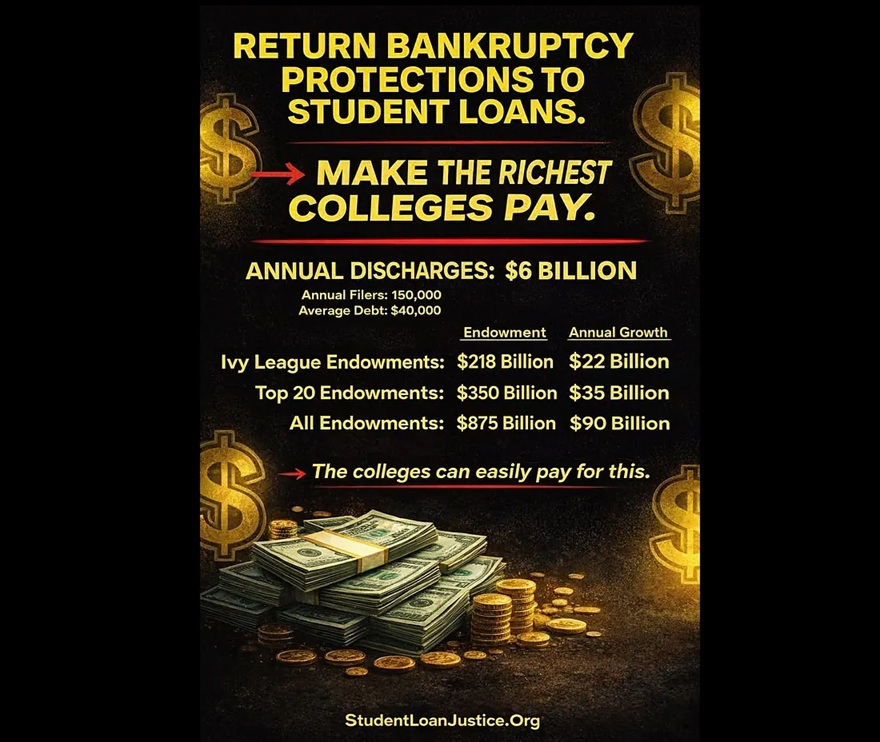

Student loan borrowers should not be timid in pushing back. They should be demanding the return of constitutional bankruptcy rights to the debt, perhaps with the wealthiest colleges in the country paying for discharges, which they can easily afford to do. Frankly, they should not feel obligated to pay on their student loans unless/until this constitutional right is returned to them.

The Founders called for uniform bankruptcy rights ahead of the power to raise an army, declare war, and ahead of every right listed in the Bill of Rights!

The Student Loan lending system has failed. The loans should be cancelled entirely. Cancellation for the good of the citizens burdened by them and the economy. A fairer, less costly and damaging model for providing education for citizens should be put in it’s place.

Such cancellation will be an economic stimulus going forward.