Federal Debt Projections

I know Econofact is discussing various programs as being an issue. Social Security being one of them. That may be true for Social Security if the funds are not available to pay back what is owed to the Trust fund. The other issue being the decreases in taxes for upper income brackets which would have a gather impact on the deficit in increases. Ideally, you would want to cut the programs if you are going to reduce funding. There are no representative or senators who are going to do that first. Too much political risk.

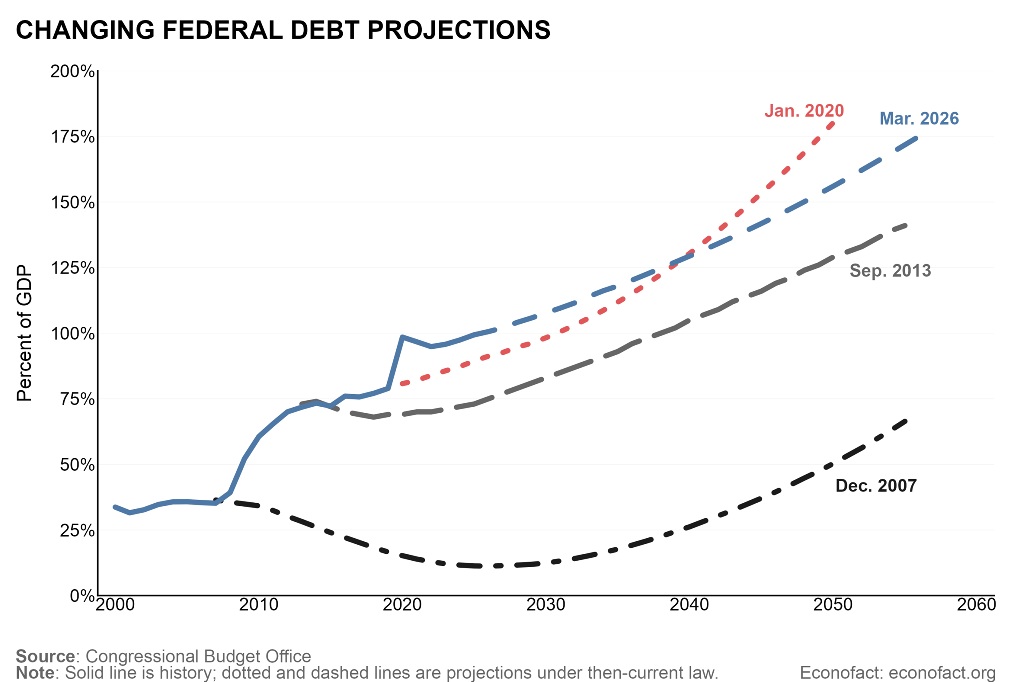

Debt exceeding tax income is the result of new tax cuts. Still this report and graph are accurate.

“The Problem of Rising Federal Debt”

Published at Econofact

“The Problem of Rising Federal Debt”

The debt of the U.S. government now exceeds national income, a situation not seen since the end of World War II. Unlike the post-war period, when the debt fell from over 100 percent of GDP to less than 40 percent in two decades, current projections have debt rising to 175 percent of GDP by 2050. What are the sources of this steep rise, and what are some possible consequences?

Annual fiscal deficits contribute to the government’s debt. Bill Gale points out in Are Growing Federal Budget Deficits and Debt Cause for Concern? Previous periods of high debt grew from deficits due to fiscal expenditures for wars or tax shortfalls because of economic downturns. In contrast, projected high deficits, even before the war in Iran, reflected rising spending in non-defense areas like Social Security and health care, and declining revenues resulting from the provisions of the 2017 Tax Cuts and Jobs Act. A team of IMF economists report, in the EconoFact memo The United States’ Fiscal Policy in a Global Context, that fiscal deficits in the United States began to rise in 2016, at a time when deficits were narrowing in many advanced economies. They note that IMF staff project fiscal deficits of around 6 percent of GDP by 2029, well above pre-pandemic forecasts.

Interest payments on the debt also contribute to fiscal deficits. Kenneth Kuttner offers an analysis of a key interest rate in The 10-year Treasury Rate: Why Is It Important and What Can Policy Do About It?. This interest rate affects not just the cost of government borrowing, but other borrowing costs as well since many mortgage and car loans are priced off this rate. The 10-year Treasury rate is currently about 4.5%, down from 4.66% in mid-May but higher than at any other time over the past 10 months. In Addressing Rising U.S. Debt, Karen Dynan notes that underlying economic forces, including the high level of debt and an aging population that will contribute to higher government spending, will likely lead to this rate rising over the coming decades.

In a recently published EconoFact Explainer, Dan Bergstresser analyzes the Interest Burden of the Federal Debt. He notes that annual net interest payments exceeded $1 trillion for the first time in 2025. This represents about 14 percent of total federal outlays and about $150 billion more than the government spent on defense in that year. He also points out that the projected growth in the debt and higher interest rates mean that the forecasted interest payments as a percentage of government spending will continue to rise, and this will contribute to a higher debt-to-GDP ratio.

Herbert Stein, who served as the Chairman of the Council of Economic Advisers under Presidents Nixon and Ford, observed “If something cannot go on forever it will stop.” In the EconoFact Chats podcast On Debt, Fiscal Crises, and AI, Greg Mankiw, who served as the Chairman of the Council of Economic Advisers under President George W. Bush, said that the unsustainable rise in the debt-to-GDP ratio could be halted through spending cuts or higher taxes. Faster economic growth could also help, although that is a less likely source of resolution. Another possibility is that the debt is monetized – the government effectively prints money to finance its deficits, but this would lead to inflation. In another new Explainer, Federal Debt and the Risk of a Fiscal Crisis, Karen Dynan and Douglas Elmendorf discuss the possibility that the lack of a resolution leads to spiking interest rates that would disrupt financial markets, raise borrowing costs, and reduce the provision of credit. The financial effects of a fiscal crisis would weaken output and employment, which could lead to a debt-deflation spiral in which the weaker economy contributes to higher debt, which in turn weakens the economy. They, and other EconoFact contributors on this issue, argue that these threats call for changing federal tax and spending policies sooner rather than later.