Mortgage Payments and the Vibecession

Mortgage Payments and the Vibecession: Homeowners’ “Cost of Living”

Mortgage payments are most owner-occupiers’ biggest monthly cash outlay. And they’re way up.

Steve Roth — Wealth Economics

I came across a pretty eye-popping economic fact recently: The typical payment on a new mortgage for an average American residence has ~doubled since 2019.1 It was $913 in Dec. 2019; it’s $1,789 today. (Causes: increased home prices, and the Fed’s 2022/23 rate increases driving up mortgage interest rates.) For comparison, the headline “consumption” price indexes (CPI and PCE) have gone up 23% and 20% respectively.

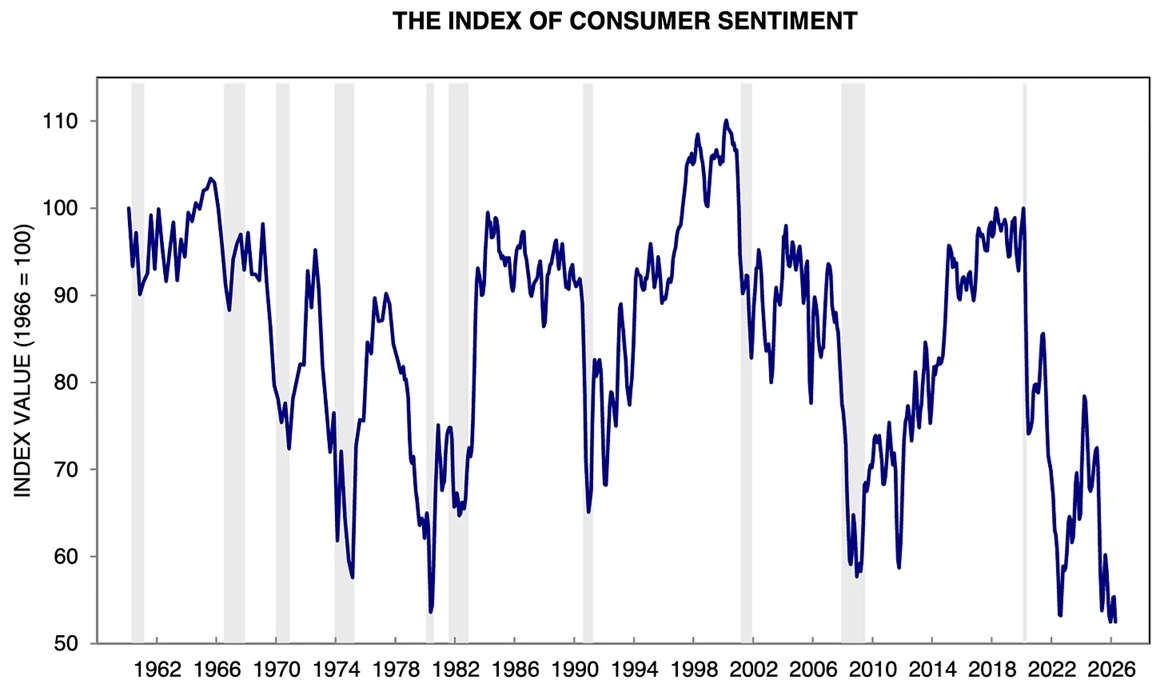

I wondered if this might help explain the much-discussed “vibecession” — consumer economic sentiment at its lowest level in history.

But mainline economic indicators suggest the economy’s doing okay. (Average mortgage payment is not among those indicators.)

Interest and principal payments — the biggest monthly cash outlay for a typical homeowner — don’t count as consumption spending (for good reasons), so that big runup is pretty much invisible in the inflation indexes. But it looms large in homeowners’ lived experience, paying the bills every month.

To be clear: this big cost increase applies to people who bought since the Fed’s rate increases (ca. 10M households), along with concurrent home-price runups. (Plus those with variable-rate mortgages, ~1.8M.) But it presumably also affects those who want or wish or need to buy and can’t attain their aspirations — whether they’re renters or current homeowners. Plus: their children? (One revealing fact here: the typical first-time home buyer in 2000 was ~30 years old. Today they’re ~40.)

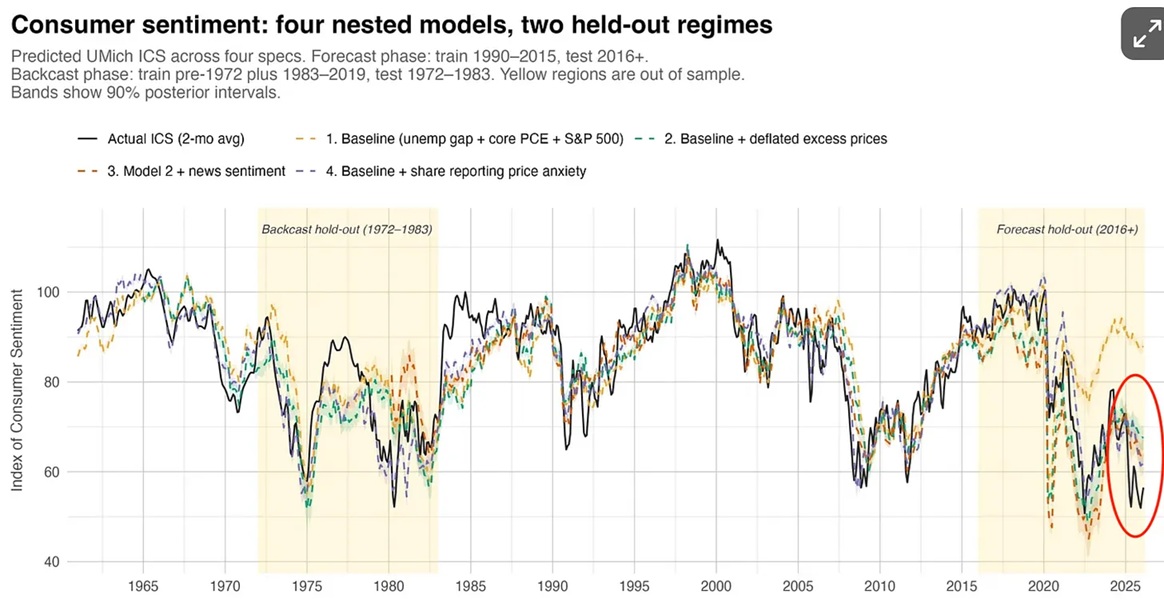

G. Elliott Morris is doing the most rigorous work I’ve seen trying to explain the vibecession, but even his best, newest model doesn’t explain it all. See the remaining gap above the black line here:

I wonder if a mortgage-payment data series added to these regressions might help close that gap.

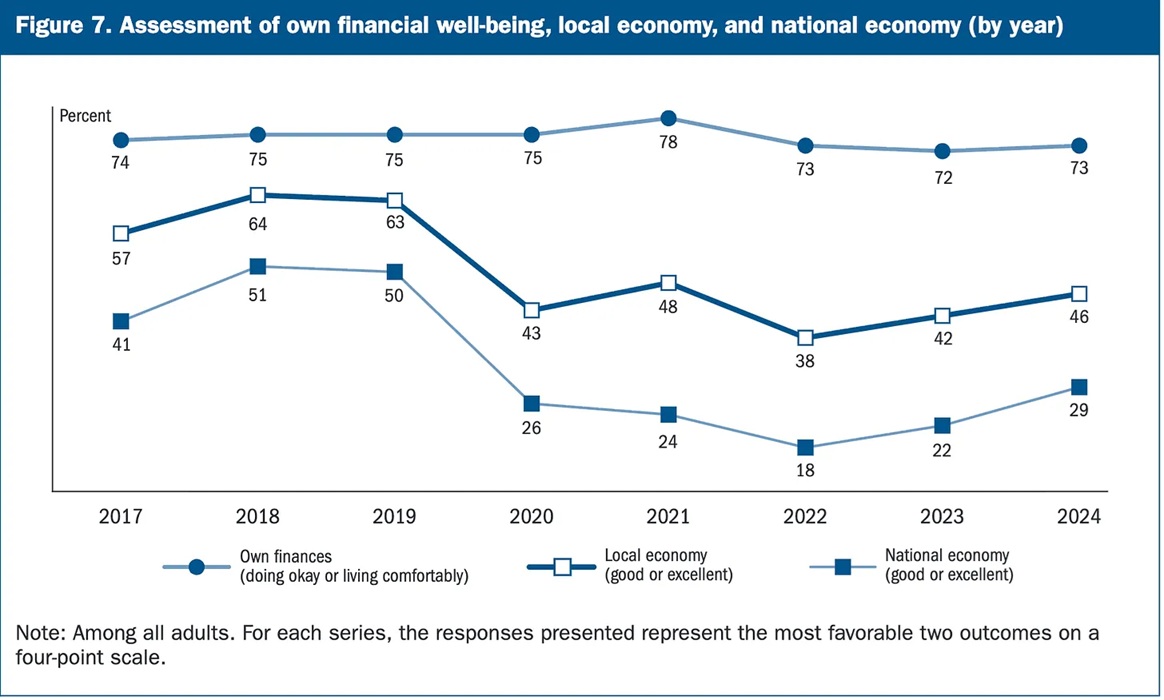

Before leaving this topic, I think it’s important to highlight a conundrum in the vibecession conversation. Consumer economic sentiment is at its lowest level ever. But when asked about their personal financial situation, at least in late 2024 people were pretty copacetic about it. (Hat tip Matt Darling.) And that is very different from their views on the local and especially national “economy” (whatever that word means to normal folks). Do with that what you will.

I was tempted to get into the excruciating methodology behind “imputed owner-occupied rent” in the national accounts, vs CPI/PCE methods, but I’ll spare you. I just thought it worthwhile to foreground a very big move in a very big (and ~invisible) part of millions of homeowners monthly “nut” — the bills they’ve actually gotta pay to keep their lives rolling along. It’s very much part of their “cost of living” even if it does settle out in the wash over a lifetime.

1 “The monthly cost of a mortgage payment when using a 20% down payment to purchase a home priced at the Zillow Home Value Index, using the monthly average mortgage rate for a 30-year fixed rate loan.” ZHVI is a “weighted average of the [price of] the middle third of homes.” Data: zillow.com/research/data/ “Mortgage Payment: 20% down, all homes, smoothed & seasonally adjusted time series.” Includes principal, interest, and mortgage insurance. Does not include homeowner’s insurance, property taxes, or maintenance costs.