Q2 Update: Delinquencies, Foreclosures and REO

by Bill McBride

Calculated Risk Newsletter

Intro: Former Angry Bear writer Bill McBribe taking up the issues of Mortgage Delinquency, Foreclosures, and Real Estate Owned (REO) foreclosed housing. The value of which decreased in the second quarter to (what Bill calls) a historically low total. Read on.

We will NOT see a surge in foreclosures that would significantly impact house prices (as happened following the housing bubble) for two key reasons: 1) mortgage lending has been solid, and 2) most homeowners have substantial equity in their homes.

Last week, CoreLogic reported on homeowner equity: CoreLogic: US Homeowners See Equity Gains Continue to Climb, but at a Slower Pace in Q2

The report shows that U.S. homeowners with mortgages (which account for roughly 62% of all properties) saw home equity increase by 8.0% year over year, representing a collective gain of $1.3 trillion and an average increase of $25,000 per borrower since the second quarter of 2023, bringing the total net homeowner equity to over $17.6 trillion in the second quarter of 2024. . . .

From the second quarter of 2023 to the [second] of 2024, the total number of homes in negative equity decreased by 15%, to 1.1 million homes or 2.0% of all mortgaged properties.

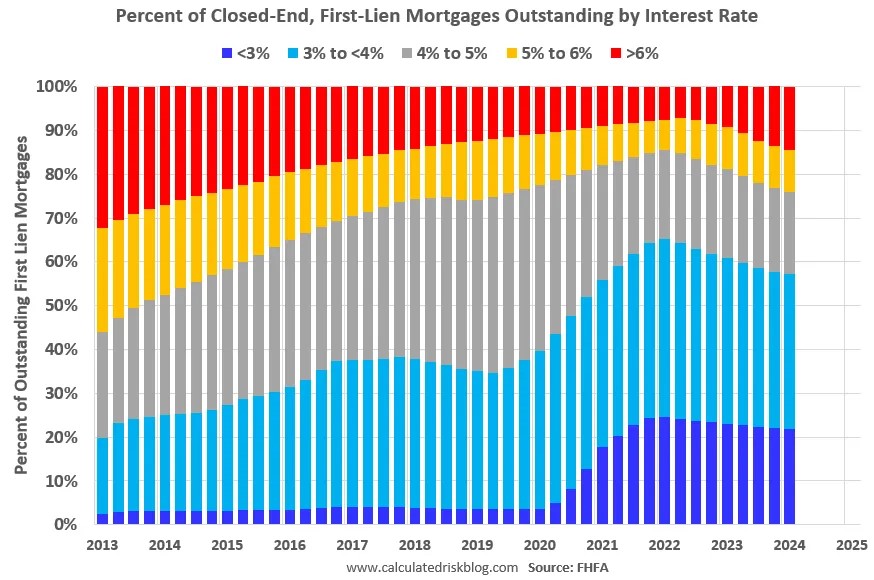

This shows the surge in the percent of loans under 3%, and also under 4%, starting in early 2020 as mortgage rates declined sharply during the pandemic. Currently 21.9% of loans are under 3%, 57.3% are under 4%, and 76.0% are under 5%.

With substantial equity, and low mortgage rates (mostly at a fixed rates), few homeowners will have financial difficulties.

Some simple definitions (for housing):

Forbearance is the act of refraining from enforcing mortgage debt.

Delinquency is the failure to make mortgage payments on a timely basis.

Foreclosure is when the mortgage lender takes possession of the property after the mortgagor failed to make their payments. “In foreclosure” is the process of foreclosure.

REO (Real Estate Owned) is the amount of real estate owned by lenders.

Here is some data on REOs through Q2 2024 . . .

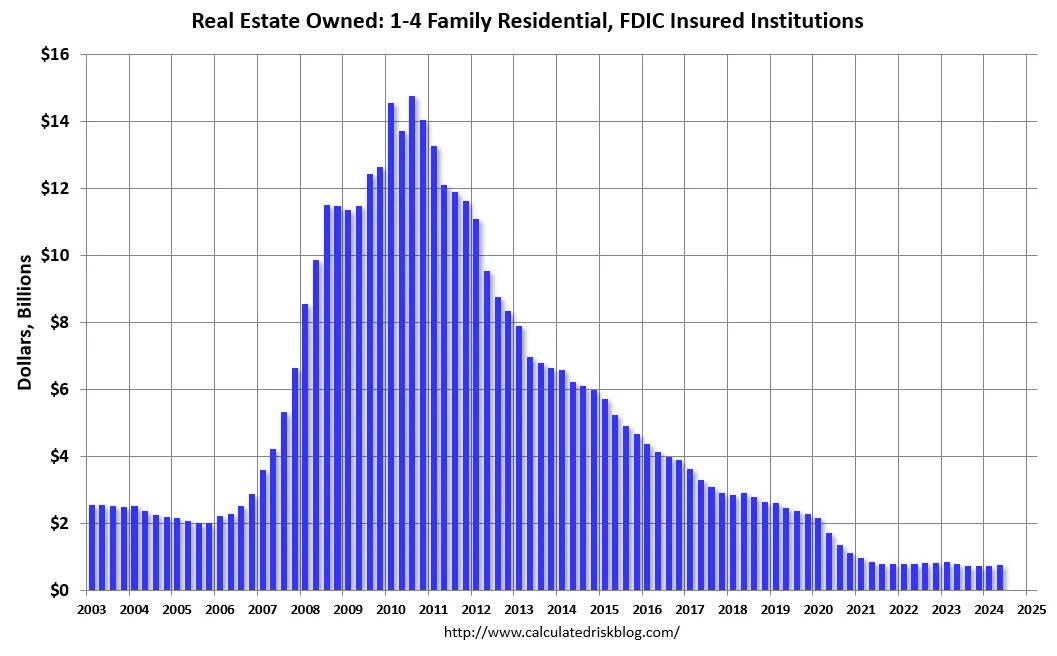

This graph shows the nominal dollar value of Residential REO for FDIC insured institutions based on the Q2 FDIC Quarterly Banking Profile released earlier this month. Note: The FDIC reports the dollar value and not the total number of REOs.

The dollar value of 1-4 family residential Real Estate Owned (REOs, foreclosure houses) decreased from $794 million in Q2 2023 to $766 million in Q2 2024. This is historically extremely low.

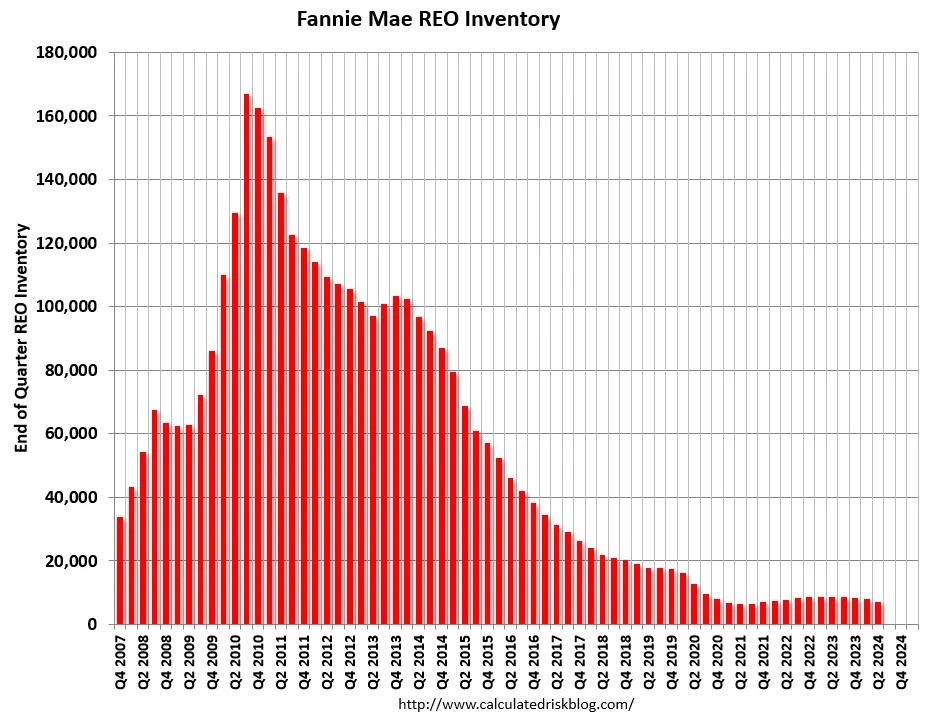

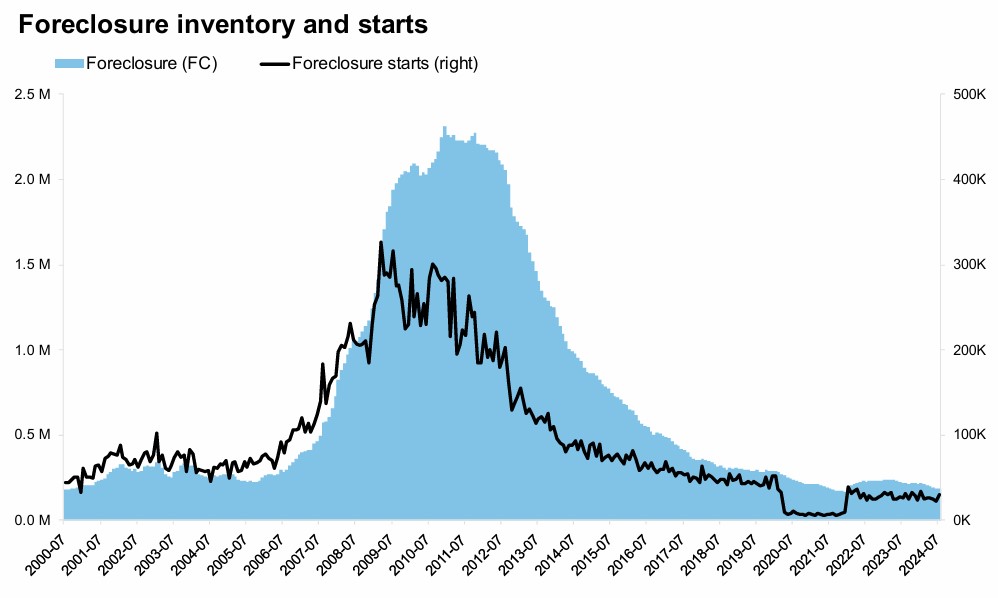

Fannie Mae reported the number of REOs decreased to 7,179 at the end of Q2 2024, down 10% from 7,971 at the end of the previous quarter, and down 17% year-over-year from Q2 2023. Here is a graph of Fannie Real Estate Owned (REO).

This is very low and well below the pre-pandemic levels. REOs are a lagging indicator. REOs increase when borrowers struggle financially and have little or no equity, so they can’t sell their homes – as happened after the housing bubble. That will not happen this time.

Here is some data on delinquencies . . .

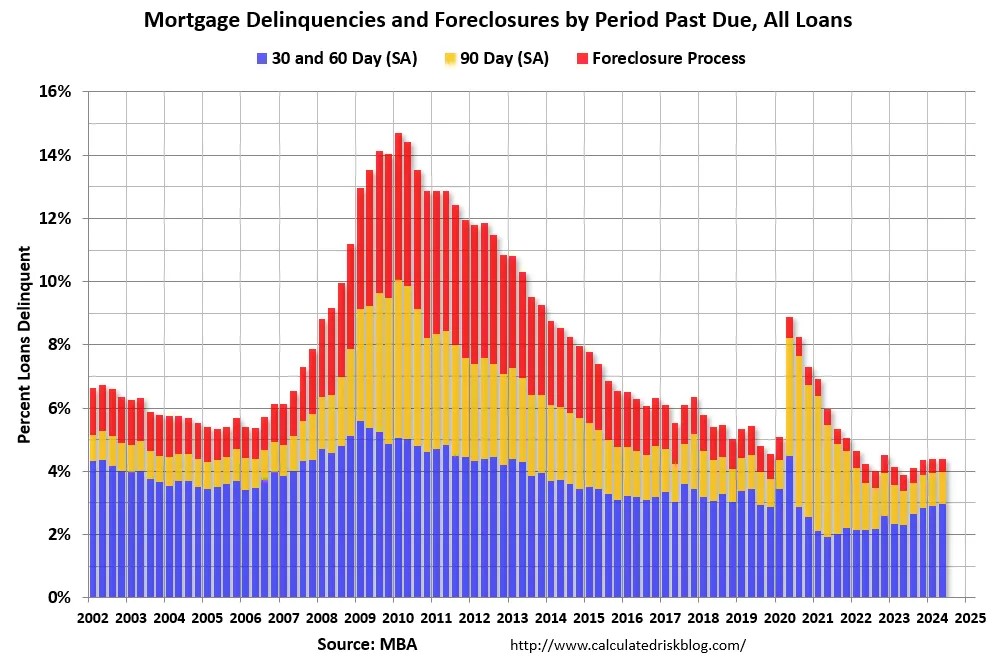

The percent of loans in the foreclosure process decreased year-over-year from 0.53 percent in Q2 2023 to 0.43 percent in Q2 2024 (red) and remains historically low. Loans in forbearance are mostly in the 90-day bucket at this point, and that has declined recently. From the MBA:

Compared to last quarter, the seasonally adjusted mortgage delinquency rate increased for all loans outstanding. By stage, the 30-day delinquency rate increased 1 basis point to 2.26 percent, the 60-day delinquency rate increased 3 basis points to 0.70 percent, and the 90-day delinquency bucket decreased 1 basis point to 1.01 percent …

The delinquency rate includes loans that are at least one payment past due but does not include loans in the process of foreclosure. The percentage of loans in the foreclosure process at the end of the second quarter was 0.43 percent, down 3 basis points from the first quarter of 2024 and 10 basis points lower than one year ago.

emphasis added

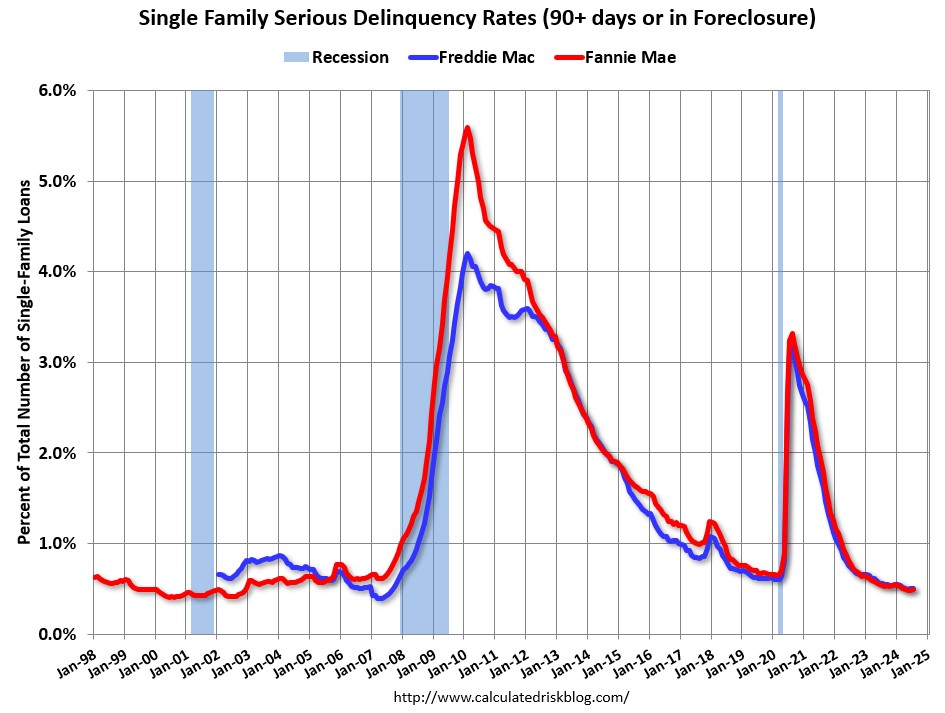

Both Fannie and Freddie release serious delinquency (90+ days) data monthly. Freddie Mac reported that the Single-Family serious delinquency rate in July was 0.51%, up from 0.50% June. Freddie’s rate is down year-over-year from 0.56% in July 2023. This is below the pre-pandemic lows. Freddie’s serious delinquency rate peaked in February 2010 at 4.20% following the housing bubble and peaked at 3.17% in August 2020 during the pandemic.

Fannie Mae reported that the Single-Family Serious Delinquency increased to 0.49% in July from 0.48% in June. The serious delinquency rate is down year-over-year from 0.54% in July 2023. This is below the pre-pandemic lows. The Fannie Mae serious delinquency rate peaked in February 2010 at 5.59% following the housing bubble and peaked at 3.32% in August 2020 during the pandemic.

This graph shows the recent decline in serious delinquencies:

The pandemic related increase in serious delinquencies was very different from the increase in delinquencies following the housing bubble. Lending standards have been fairly solid over the last decade, and most of these homeowners have equity in their homes – and they have been able to restructure their loans once they were employed.

And on foreclosures . . .

ICE reported that active foreclosures have decreased are near the records. From ICE: ICE Mortgage Monitor: Rate drops make August most affordable month since February, as home price growth cools to 12-month low

- Foreclosure starts jumped by 32% in July, but that spike appears to be more a sign of volatility in monthly referral volumes after coming off a post moratorium low in June than a signal of broader risk in the market

- Fewer than 30K loans were referred to foreclosure in the month, which is still more than 30% below 2019 levels, with the number of seriously delinquent mortgages also continuing to run historically low

- Active foreclosure inventory nudged higher (+2K), but remains at its second-lowest level since January 2022 and is still 34% below pre-pandemic levels

- July foreclosure sales (5.5K) increased +3.7% month-over-month, but were down -9.6% from last year and still less than half of 2019 averages

- The national foreclosure rate edged modestly higher in July as well, a month after hitting its lowest level on record outside of Q4 2021 at the tail end of the national foreclosure moratorium

The bottom line is there will not be a huge wave of foreclosures as happened following the housing bubble. The distressed sales during the housing bust led to cascading price declines, and that will not happen this time.