Healthcare Costs – KFF

What you are getting here is a rundown of health insurance costs as measured in 2025. KFFdoes do an annual survey to back up its yearly numbers. I grabbed the early portion of the KFF report on Employer sponsored healthcare for its employees. This piece tells you what each grouping pays by size of firm, numbers of employees, age concentration, type of business, and even salary. It is a rundown.

Costs over the last five years? “Average family premiums have risen 26%, roughly in line with the cumulative increase in inflation (23.5%).” Not terrible for sure. It does take more from a family ;eainnot much for other costs.

“2025 Employer Health Benefits Survey”

KFF

Summary of What KFF Found in 2025 for Healthcare Costs

Employer-sponsored insurance covers 154 million people under the age of 65. To provide a current snapshot of employer-sponsored health benefits, KFF conducts an annual survey of private and non-federal public employers with ten or more workers. This is the 27th Employer Health Benefits Survey (EHBS) and reflects employer-sponsored health benefits in 2025.

This gets complex as you wade through the findings.

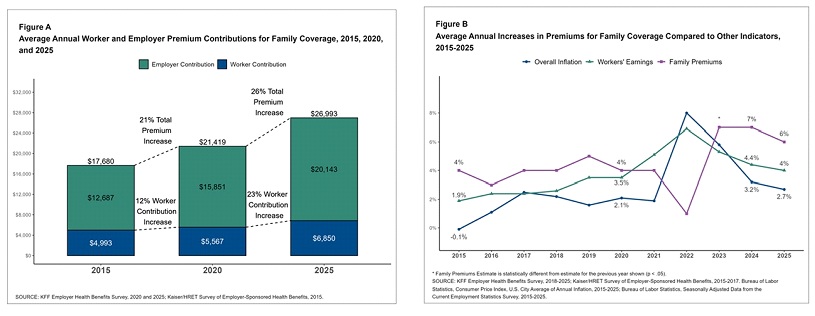

The average annual premiums for employer-sponsored health insurance in 2025 was $9,325 for single coverage and $26,993 for family coverage. Over the last year, the average single premium increased by 5% and the average family premium increased by 6%. Comparatively, there was an increase of 4% in workers’ wages and inflation of 2.7%. Over the last five years, the average premium for family coverage has increased by 26%, compared to a 28.6% increase in workers’ wages and inflation of 23.5% [Figure A, Figure B].

The average premium for smaller firms with 10 to 199 workers is comparable to the average premium at larger firms for covered workers. Single coverage ($9,211 and $9,361) and lower for family coverage ($26,054 vs. $27,280). The average premiums for covered workers in high-deductible health plans with a savings option (HDHP/SO) are lower than the overall average premiums for both single coverage ($8,620) and family coverage ($25,379). In contrast, average premiums for covered workers enrolled in PPOs are higher than the overall average premiums for both single ($9,818) and family coverage ($28,272).

Premiums also differ with firm characteristics. The average premiums for both single and family coverage are relatively low for covered workers at private for-profit firms and relatively high for covered workers in private not-for-profit firms.

The average premiums for covered workers at firms with larger shares of older workers (where at least 35% of the workers are age 50 or older) are higher. While the average premiums for covered workers at firms with smaller shares of older workers for both single ($9,599 vs. $9,068) and family ($27,699 vs. $26,332) coverage.

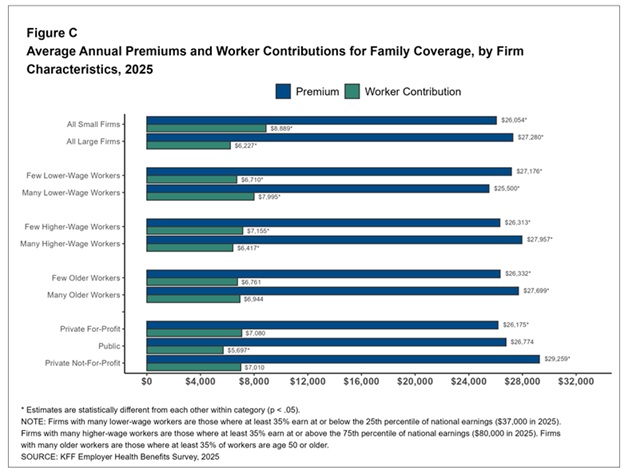

The average premiums for covered workers at firms with relatively large shares of higher-wage workers (where at least 35% of workers earn $80,000 a year or more) are higher than the average premiums for covered workers at firms with smaller shares of higher-wage workers for both single ($9,600 vs. $9,133) and family ($27,957 vs. $26,313) coverage [Figure C].

Figure C: Average Annual Premiums and Worker Contributions for Family Coverage, by Firm Characteristics, 2025

Most covered workers contribute to the cost of the premium directly. On average, covered workers contribute 16% of the premium for single coverage and 26% of the premium for family coverage, similar to the percentages contributed in 2024. The average contribution rates for single coverage are the same for covered workers in firms with 10 to 199 workers and in larger firms (16%) but the average contribution rate for family coverage is higher for covered workers in firms with 10 to 199 workers than for those in larger firms (36% vs. 23%). On average, covered workers at private, for-profit firms have relatively high premium contribution rates and covered workers in public firms have relatively low contribution rates for both single coverage and family coverage.

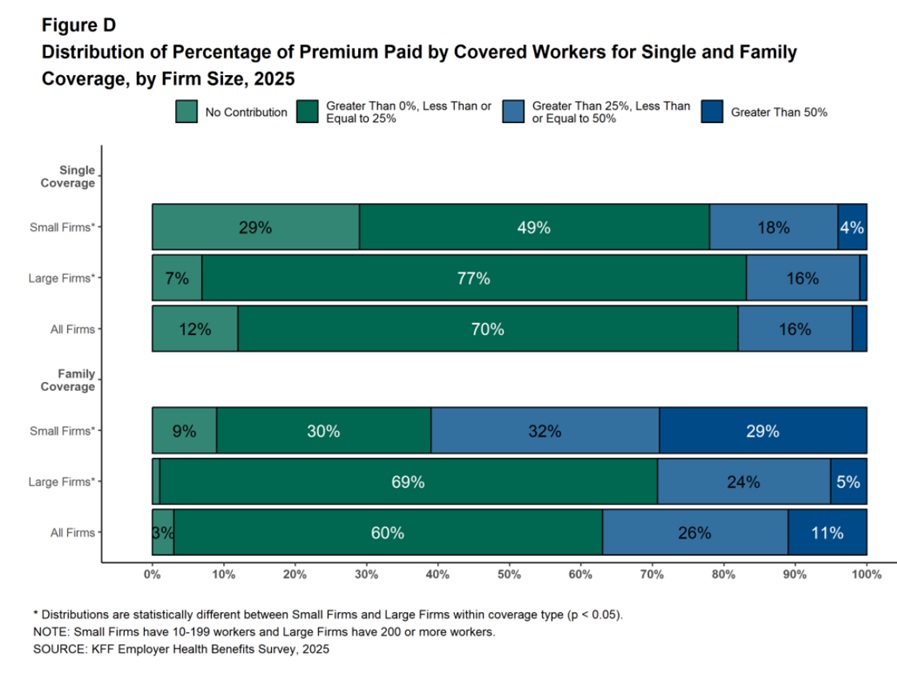

Twenty-nine percent of covered workers at firms with 10 to 199 workers are enrolled in a plan where the employer pays the entire premium for single coverage, compared with only 7% of covered workers at larger firms. In contrast, 29% of covered workers at firms with 10 to 199 workers are in a plan where they must contribute more than half of the premium for family coverage, compared to 5% of covered workers at larger firms [Figure D].

Figure D: Distribution of Percentage of Premium Paid by Covered Workers for Single and Family Coverage, by Firm Size, 2025

The average annual contribution amounts for covered workers are $1,440 for single coverage, similar to the amount last year, and $6,850 for family coverage, higher than the amount last year. The average contribution amount for family coverage for covered workers at firms with 10 to 199 workers ($8,889) is higher than the amount for covered workers at larger firms ($6,227) [Figure C]. Eleven percent of covered workers, including 28% of covered workers at firms with 10 to 199 workers, are in a plan with a worker contribution of $12,000 or more for family coverage.

Summation for now?

Average annual premiums increased by 5% for single coverage and 6% for family coverage in 2025. This is similar to the rate of growth over the past two years. Over the last five years, average family premiums have risen 26%, roughly in line with the cumulative increase in inflation (23.5%) and wage growth (28.6%) over the same period.

Early reports suggest that cost trends will be higher for 2026, potentially leading to higher premium increases unless employers and plans find ways to offset higher costs through changes to benefits, cost sharing, or plan design. One place where this story is playing out is coverage of GLP-1 agonists for weight loss. The share of the largest firms covering these medications for weight loss increased significantly in 2025, but many of these firms also reported higher than expected use, as well as a significant impact on prescription costs. Discussions with individual employers suggest that some have stopped covering these medications for weight loss, with a few even tightening up coverage for those with diabetes. While concerns over the negative health impacts of obesity remain, they are now in competition with concerns about the high cost and proper use of GLP-1 agonist medications, particularly at a time when other cost pressures may be growing. Whether and how to provide coverage for GLP-1 agonists will continue to be an important topic for employers and workers over the next few years.