Medicare Advantage

“Medicare premiums are being pushed by rising payments to Medicare Advantage plans,” Social Security Report

In 2026, Americans who use Medicare Part B to pay for their doctor’s visits can expect to see premiums increase by nearly 12% to $206.20 a month, according to a Medicare Trustees report. Yet while the government-run health program’s premiums are expected to go up, premiums for subsidized private health insurance plans under Medicare Part C, also known as Medicare Advantage, are expected to go down — from an average of $16.40 a month in 2025 to $14 a month in 2026, per an announcement from the Centers for Medicare & Medicaid Services (CMS).

The cost of Medicare Part B has jumped because premiums are being pushed by rising payments to Medicare Advantage plans, according to a March 2025 report from the Medicare Payment Advisory Commission (MedPAC), a non-partisan healthcare advocacy group. Per this report, Medicare will spend about 20% more on Medicare Advantage enrollees than those using regular Medicare in 2025, an amount equivalent to $84 billion.

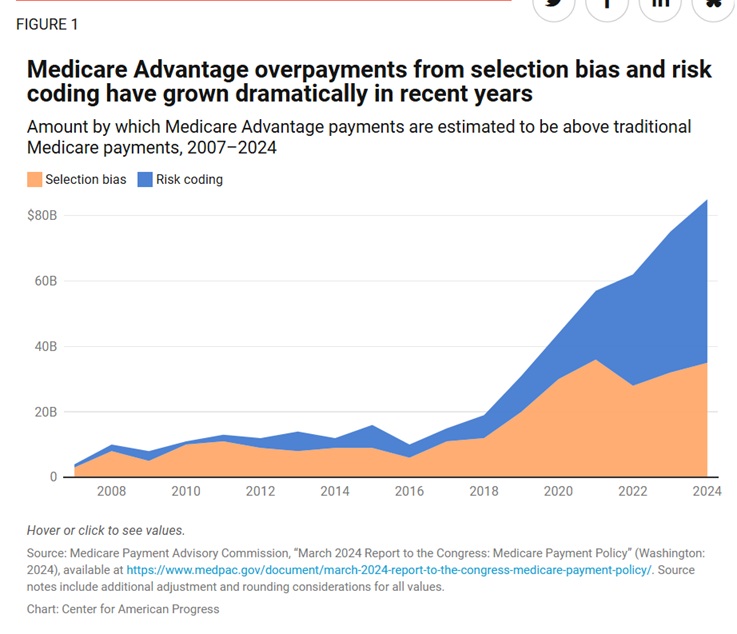

But that’s not all. According to another report from the Center of American Progress (CAP), insurance companies used upcoding (making their policy holders appear sicker than they really are for more compensation) and selection bias (private companies gearing plans and coverage toward healthier patients) to obtain between $83 billion and $127 billion in Medicare Advantage overpayments in 2024 alone. Without reform, CAP added, Medicare risks allocating up to $2 trillion in overpayments to insurance companies in the next decade.

“Ending Overpayment in Medicare Advantage” CAP

The Drivers of MA overpayment

Upcoding or risk-score gaming

CMS uses a risk adjustment process to determine how much to pay an MA plan for any given patient, as patients have varying health needs. A key factor in determining risk scores is a patient’s diagnosis codes.21 As a result, MA plans have an incentive to maximize the number of diagnosis codes attributed to each patient—and to push the limits in terms of which codes can be legitimately assigned to a given patient.22 The more lucrative the code, the higher the payment. In the traditional Medicare program, there is no comparable incentive to misuse diagnosis codes or to maximize the entry of valid codes; the process of finding and entering codes can be tedious and burdensome and distract from patient care.

This contrast is clearest when a patient moves from traditional Medicare to MA. Upon this transition, an MA plan can submit many more diagnosis codes to demonstrate how “sick” a patient is.23 Medicare then pays more for that patient because of these extra diagnosis codes, even though the patient is not any sicker, nor are their expected medical costs any higher than while they were covered by traditional Medicare. This “upcoding” in MA plans is a key source of overpayment: MedPAC estimates that MA risk scores will be inflated by approximately 20 percent in 2024.24 To partially account for this, CMS applies a “coding intensity adjustment” of slightly less than 6 percent. However, this still leaves overpayment levels of approximately 13 percent.25

Selection bias

MA plans tend to enroll beneficiaries who are healthier and more profitable than beneficiaries who choose traditional Medicare, even after accounting for risk scores.26 Health plans have a significant and obvious financial incentive to enroll beneficiaries who are healthier than average at the same risk score. As a result, plans employ a variety of business strategies to attract healthier beneficiaries. One classic example is through offering gym benefits, which tend to be of value to people who are relatively healthier, thus attracting to MA those who have fewer health needs.27

Another strategy is to limit network access to comprehensive cancer centers, which could make MA less attractive to patients with cancer and complex medical needs.28 MA plans can also deploy their significant marketing efforts to selectively target more profitable patients.29 From a patient perspective, traditional Medicare guarantees access to a broad network of providers, while MA plans come with more restricted networks.30 People with fewer health needs are more likely to accept MA’s restrictions on care.

The result of these practices is that MA enrolls patients with lower-than-average spending at any given risk score, leading to further overpayment to MA plans, which then get paid as if their members are sicker than they are. Further evidence of this comes from a KFF analysis that found patients who switched from traditional Medicare to MA spent less in the prior year than those patients who remained in traditional Medicare—emphasizing that patients who move from traditional Medicare to MA tend to be healthier.31

It is worth noting that selection bias also happens in the opposite direction: Patients who switch from MA to traditional Medicare have higher risk-adjusted spending than those patients who stay in MA.32 For instance, a patient in MA who receives a serious diagnosis such as cancer might face considerable difficulty finding an in-network cancer center or dealing with prior authorization requirements for recommended scans. Therefore, they may choose to switch to traditional Medicare, which provides better access to care.

MedPAC estimates that in 2024, favorable selection will cause MA plans to be overpaid by approximately 9 percent.33

Quality bonuses and county adjustments

The MA quality bonus program is intended to incentivize and reward high quality among MA plans. As detailed in a recent Urban Institute report, however, the net impact of the program is overly generous payments to MA plans absent any clear impact on quality.34 Furthermore, as designed, the MA quality bonus program exacerbates health inequities. The program assigns each MA contract a rating of 1 to 5 stars based on performance across dozens of measures. Notably, MA plans with higher star ratings—and, as a result, higher bonus payments—appear to have larger racial disparities than lower-rated plans.35 Plans in metropolitan areas with high MA enrollment and low traditional Medicare spending are also eligible to receive lucrative MA “double bonus” payments, but those payments have been found to worsen racial disparities without improving plan quality.36 One study found the net effect of double bonuses was to increase payments for Black beneficiaries by $60 per year, compared with $91 for white beneficiaries.37

In addition, the MA quality bonus program is not budget neutral, unlike other Medicare quality incentive programs. The program functions through an add-on payment that boosts spending to awarded MA plans above traditional Medicare levels. MA plans with higher star ratings receive a 5 percent bonus to their payment benchmark, and in those counties where a double bonus is available, plans receive a bonus of 10 percent to their benchmark.38 In 2024, spending on the MA quality bonus program is estimated to reach $15 billion.39

In addition to the MA quality bonus program, Congress has legislated that MA payment benchmarks be increased in counties with lower traditional Medicare spending. To calculate county benchmark adjustments, counties are split into quartiles; those counties with the lowest traditional Medicare spending receive 15 percent increases to their benchmarks, and counties with the highest levels of traditional Medicare spending have their benchmarks decreased by 5 percent.40 The original motivation for this payment adjustment was to protect against MA plans not entering counties with historically low traditional Medicare spending—and therefore lower payment benchmarks against which MA plans would have to bid.41 However, as more than half of all Medicare beneficiaries are now enrolled in MA (and as that share continues to grow),this extra incentive is arguably no longer needed. The effect of the payment adjustments as they exist today is unnecessary inflation of MA payments.42

MedPAC estimates indicate that in 2024, quality bonuses and county adjustments will inflate benchmarks by approximately 8 percent.43

The two overpayment estimates presented in this report classify this increase in different ways:

- The lower estimate does not include quality bonuses and county adjustments as a direct source of overpayment, instead considering these payments to offset savings that would otherwise accrue due to MA bids being below the traditional Medicare benchmark.44

- The higher estimate, in contrast, classifies payments resulting from quality bonuses and county adjustments as a form of overpayments. Because plans receive a rebate that is a portion of the difference between their bid and the benchmark (typically 65 percent) this report’s higher estimate concludes the inflated benchmarks resulting from quality bonuses and county adjustments lead to overpayments of approximately 5 percent.45

The effects of supplemental coverage on traditional Medicare benchmarks

When MA plans submit their bids to CMS to be compared against traditional Medicare benchmarks, they do so based on their expected cost of covering the traditional Medicare benefit package (services covered by Parts A and B). However, traditional Medicare benchmarks are not set based on Medicare’s spending on beneficiaries with Medicare Parts A and B alone. They also account for enrollees’ supplemental coverage, which facilitates increased use of Parts A and B covered services. Roughly 90 percent of traditional Medicare beneficiaries carry additional supplemental coverage, including Medicaid or private “Medigap” plans. This reduces out-of-pocket cost exposure for Parts A and B covered services.46 In effect, MA bids are benchmarked to total traditional Medicare spending, which includes standard Parts A and B coverage and any supplemental coverage a beneficiary has.47

Why is this problematic?

Supplemental coverage lowers beneficiaries’ out-of-pocket cost exposure, facilitating increased use of care that is baked into the benchmarks used to set MA payments. Literature historically has referred to this increased use of care as “induced utilization.” Perhaps it is better described as alleviating the depressed utilization patients experience when out-of-pocket cost exposure is high.

If Traditional Medicare alone is to be considered the baseline, the effects of supplemental coverage in benchmark calculations can be considered a source of overpayment to MA relative to traditional Medicare. A recent estimate suggests that the effects of supplemental coverage increase traditional Medicare benchmarks by approximately 18 percent, which implies approximately 12 percent in overpayments.48

Leaping to the end and a conclusion which I will explore later.

MA plans are significantly overpaid compared with what traditional Medicare spends on beneficiaries. There are no or little (being generous), without any clear improvements in the quality or affordability of care. MA overpayments threaten the financial sustainability of the Medicare Hospital Insurance Trust Fund. MA puts the traditional Medicare program at risk and undermines the goals of the Medicare program overall.

AMAC medicarereport.org – Your source for breaking news and informational reports on health care