2023 ACA Open Enrollment Period

November 1st is the start of the official 2023 ACA Open Enrollment Period (OEP) for anyone who needs quality, affordable healthcare coverage. Charles Gaba at ACA Signups has a very detailed rundown on what is happening this year. Because of President Biden, there have been improvements to the ACA.

What I have done below is a brief rundown of Charles Gaba’s Open Enrollment post. It is not as detailed as his post. If you are serious about using the ACA for healthcare insurance, you may want to go to his site. Charles has more detail there than I have placed here.

“It’s That Time Again! Here’s 12 important things to remember before you #GetCovered for 2023!” ACA Signups, Charles Gaba.

One Commenter: “My ACA plan to cover my wife and I and three children is about the same as what we pay for internet and TV. It’s less than a car payment now with the enhanced subsidies!! Thanks Uncle Joe!!”

DON’T DELAY; GET COVERED SOONER RATHER THAN LATER!

The official 2023 Open Enrollment Period runs from November 1st through January 15th in most states. There are some exceptions at both ends. Idaho already launched their OEP on October 15th. New York doesn’t kick theirs off until November 16th. Check ACASignups for specific dates for each state.

At the opposite end, several states have later final deadlines, including California, DC, Massachusetts, New Jersey, New York and Rhode Island…but there’s also two states which end their OEPs earlier (Idaho and Maryland).

ONLY ENROLL VIA AN OFFICIAL ACA HEALTH EXCHANGE OR AN AUTHORIZED ENROLLMENT PARTNER.

ACA financial subsidies are available to millions more Americans than were before. The subsidies are only availalble to eligible enrollees who sign up through an official ACA exchange or an authorized 3rd-party exchange entity, known as an Enhanced Direct Enrollment (EDE) entity. List of state logons on ACASignups.

Watch out for the scammers!

IF YOU’RE ENROLLED OFF-EXCHANGE, SEE IF YOU CAN ENROLL ON-EXCHANGE INSTEAD.

Somewhere between 2.3 – 3.0 million Americans are still enrolled in OFF-exchange, ACA-compliant individual market policies. Historically, the main reason for this has been that they didn’t qualify for financial help. They didn’t see the point of filling out any additional forms by enrolling on-exchange.

As many as half or more of those 2.3 – 3.0 million people will be leaving hundreds or thousands of dollars on the table if they don’t make the switch!

MILLIONS OF AMERICANS CAUGHT IN THE “FAMILY GLITCH” MAY NOW BE ELIGIBLE FOR UP TO THOUSANDS OF DOLLARS IN SAVINGS!

As explained here and here. Due to how the U.S. Treasury Dept. and the Obama Administration interpreted an obscure provision of the Patient Protection & Affordable Care Act regarding employer coverage affordability thresholds, there were several million people who really should have been eligible for ACA subsidies for years now and who have not been.

As of October 2022, this is no longer an issue for many. Check to see if now eligible for a less costly plan.

OTHERS WHO DIDN’T USED TO QUALIFY FOR FINANCIAL HELP NOW QUALIFY AS WELL!

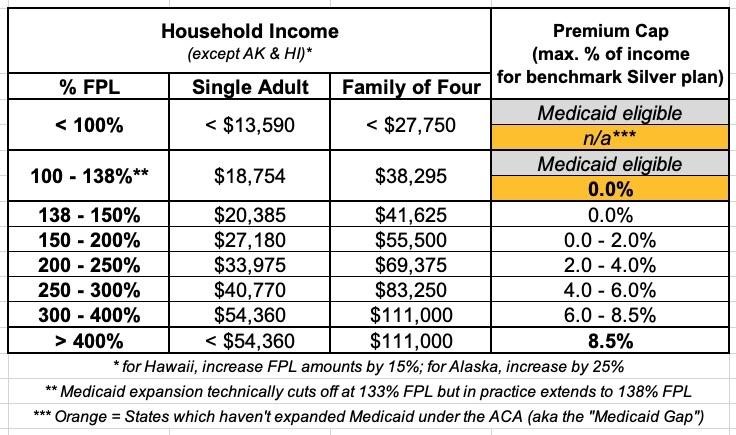

Prior to the Biden’s Inflation Reduction Act, ACA subsidies were on a sliding income scale to enrollees earning between 100 – 400% FPL (roughly $54,000/year for one person or $111,000/year for a family of four this year). If you earned more than 400% FPL, you had to pay full price no matter how expensive the premiums.

The ACA’s infamous “Subsidy Cliff” has been killed at last (through at least the end of 2025.

TEN STATES ARE OFFERING *ADDITIONAL* SAVINGS *ON TOP OF* THE EXPANDED ARP SUBSIDIES!

I am not going to detail what the ten states are offering as additional saving. Charles Gaba’s ACASignups has more detail under item #6. It is better to read about it there.

MILLIONS OF PEOPLE ARE ELIGIBLE FOR FREE “SECRET PLATINUM” PLANS (LABELED AS SILVER)!

Detail Here: If your household earns less than 200% FPL in any state (around $25,500/yr if you’re single; around $52,000/yr for a family of four), choose a SILVER plan! “ACA’s Cost Sharing Reductions (CSR)” system, will give additional financial help lowering your deductible, co-pays, and coinsurance. It effectively transforms Silver plans into Platinum plans!

The premiums for these “Secret Platinum” plans are much lower for anyone earning under 150% FPL and max out at just 2% of your annual income from 150 – 200% FPL! Again, check detail at ACASignups.

VIA SILVER LOADING, SOME SUBSIDIZED ENROLLEES MAY BE ABLE TO GET FREE GOLD PLANS!

As explained “here:,” Due to a long, strange series of events, subsidized enrollees earning 200% FPL or more may end up getting a Gold plan for less than Silver, or a Bronze plan for free!).

THE INDIVIDUAL MANDATE IS STILL AROUND IN FIVE STATES!

The single most controversial part of the Patient Protection & Affordable Care Act was the Shared Responsibility Provision, commonly known as the “Individual Mandate Penalty.” Check detail at ACASignups Item 9.

MANY STATES & COUNTIES WILL HAVE MORE CARRIER & PLAN CHOICES THAN EVER.

Every year, changes occur on the ACA markets as new carriers enter or expand their coverage areas to more counties/states. Or as currently participating carriers pull out of them. In addition, existing carriers often add new plans or phase out current ones. Check detail at ACASignups. Item #10.

THE NAVIGATOR PROGRAM IS BACK AT FULL STRENGTH

Trump Administration gutted both the ACA’s marketing/outreach budget (slashing it down by 90%) as well as its “Navigator” program. Dozens of organizations around the country are available helping ACA enrollees left to find their way through the world of health insurance enrollment (as well as those needing guidance to get into Medicaid, CHIP and other healthcare programs).

WHATEVER YOU DO, *DON’T* LET YOURSELF BE PASSIVELY AUTO-RENEWED

It’s always a good idea to actively shop around the ACA marketplace each Open Enrollment Period to see whether there’s a better value for the upcoming year, but it’s even more important now. See the reasons why at ACASignups.

“Fixing the Family Glitch for 5.1 million People” Angry Bear