Global Manufacturing of Semiconductors

There is a lot of noise about the shortage of semiconductors. I am not going to explain it all here. You will find the explanation of manufacture in the articles. It takes weeks to grow wafers and then Fab semi-conductors. Not maintaining orders for semiconductors creates shortage when production starts up again.

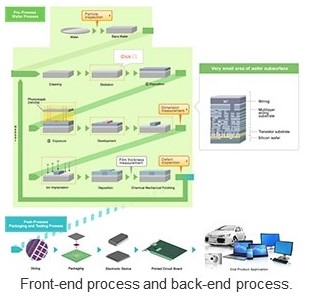

The purchase of semiconductors has changed since I was in it in 2008 chasing automotive OEM caused shortages. Growing the wafers could be done in the US. The fabrication also in the US. Th wafers could also be sent to places such as Malaysia, Philippines, etc. or closer. China is on the move to take over or impact the whole industry with its eye on Taiwan. This is a simplified depiction of a two-part process with many functions in each. Typically, this is done in two plants. One to grow wafers and the other to Fab semiconductors. Click on the images to enlarge.

Silicon substrate (wafer)

“Biden’s Uphill Battle to Restructure the Global Semiconductor Sector – The Diplomat, Tian He and Anton Malkin “Understand one term, fabless manufacturing is the design and sale of hardware devices and semiconductor chips while outsourcing their fabrication (or fab) to a specialized manufacturer or semiconductor foundry. The US is the leader in Fabless manufacturing, the design and sale of semiconductors. Biden’s plan necessitates the U.S. to pay attention to the middle and lower ends of the GVC (global value chain), the sourcing and manufacture pf semiconductors to US aligned countries and eventually the US. The administration’s plan is to build manufacturing facilities in the US and also attract foreign companies such as (TSMC, Samsung, etc.) to source manufacturing in the US.

This strategy is currently being pursued in two ways. The first is to ally with global semiconductor firms to re-shore production by building domestic manufacturing facilities. The second is the Biden administration’s intention to work with “like-minded” countries to build a more reliable semiconductor supply chain not involving China.”

“Strengthening a Transnational Semiconductor Industry” | Center for Strategic and International Studies (csis.org), James Andrew Lewis “the problem is China, its industrial policies, and its intentions regarding Taiwan, not offshore production.

Front and back-end process

The politics of the chip industry are generally favorable to the United States. One leading producer, South Korea, is a treaty ally and faces less risk of disruption from China than does Taiwan. Another leading producer, Japan, is one of the most important U.S. security partners and, with the United States, dominates the production of semiconductor manufacturing equipment (SME). ASML, another leading producer of SME, based in the Netherlands, is also an important ally. Singapore, while it would prefer not to be caught in a battle between giants, is also a dependable partner. These countries share democratic values and in many instances are treaty allies.

Taiwan Semiconductor Manufacturing Company, or TSMC, has a 50 percent share in the fabless market. However, TSMC’s proximity to China, which has routinely threatened to invade and absorb Taiwan, creates a potential security risk.”

“Semiconductor industry | Strategy&” (pwc.com) Strategies for growth in the Internet of Things era. The Internet of Things (IoT), once again transforming the semiconductor industry.

“The semiconductor industry is no longer dominated by a handful of the largest players. Companies must now follow a different path, competing not so much on their performance edge or lower price, but on making the best chips for specific purposes, what data capture and communications services their chips enable, and their ability to collaborate with other players across the IoT (Internet of Things) value chain.

This, in turn, is putting an increasingly large premium on how semiconductor companies decide to approach their markets — what their “way to play” is — and on the distinctive capabilities they deploy to carry out that approach. With the IoT, semiconductor innovation is no longer driven primarily by Moore’s Law. Moore’s Law predicted the rapid escalation in the number of transistors on each chip and the concomitant increase in performance speed and decline in cost. The value of the chips required to power the IoT is not measured in sheer speed; other factors, such as power consumption, miniaturization, software, configurability, and durability, are more important.”

A Deep Dive Into The Semiconductor Industry | Seeking Alpha, Kenneth Mell

“Most people are familiar with Moore’s Law, which I described in the previous section. However, fewer people are familiar with Moore’s Second Law, which states that the cost of a foundry doubles every four years. This law intuitively makes sense because as chips get smaller, they get more expensive and complex to create. For example, it now costs $150 million just to purchase an EUV machine from ASML. Not many startups have that kind of cash lying around, so the largest foundries have a narrow moat from that especially as chips continue to get more advanced.

Taken to its logical conclusion, Moore’s Second Law means there will be fewer and fewer foundries over time. This seems to be the case historically. An innovation called FinFET eliminated all but six foundries from mass producing chips in the aughts. Then in 2015, GlobalFoundries and UMC gave up on sizes smaller than 14nm, leaving only Intel, Samsung, and TSMC capable of mass-producing cutting-edge nodes. Intel’s recent struggles leave only two companies still on the cutting edge at 5nm: TSMC and Samsung.”

I hope this helps . . .

Back in the day, my (international) employer was told in no uncertain terms that unless they would invest large funding in local research facilities (and manufacturing plants), there efforts to do business in those countries would be constrained forthwith. They complied, as their business would suffer greatly if they refused.

The fundamental problem is that we as a country don’t have a coherent industrial policy. It’s worse than that because here the very idea of having a national industrial policy is considered in most quarters to be heresy. Actual strategic planning outside of the military is entirely absent. The prime imperative is to create a favorable climate for business and then, poof, magically everything that we need is going to be supplied by the market fairy. We have centuries of empirical evidence that the world does not work this way. But evidence has never been a very strong weapon when trying to convince people to support something that violates their religious tenets.

SW

I agree with your analogy of having a plan as opposed to waving the magic wand hoping thing will occur in a rational fashion. One of the imperatives as you state is to have a favorable climate for business. That is one of them. The other is to ensure business fits in with the social atmosphere of the area it relocates to and builds. Business has a habit of rolling over communities with its promises of tax dollars and jobs. A few years down the road and poof, they are gone leaving the infrastructure they built for the community to resolve. Communities typically give tax breaks to these companies.

Michigan Tax Breaks

Tax Credits

Actual Michigan Incentives

Much and many of these incentives are given to companies just to stay put. In 2009, GM raked in ~$3 billion from Michigan. The people have jobs and often times the community gets little more. And this is at the state level which has the wherewithal to negotiate better deals after getting community input. Sitting on a Municipal Planning Commission was an experience. I told one mall developer who was building an upscale mall, I would not vote for the Mall. The reason? I told him WalMart was not an example of an upscale store. We had a plan as developed by us and the builder. I was not going to deviate from it.

Religion be damned. Too many wars have been fought over religion. We are in the midst of religious beliefs driving the nations laws. These crackpots do not follow their religion as it is written. It is all a matter of control which will end when people have had enough.

Thank you for your comment.

The “religion” I was referring to is Free Market Fundamentalism, which is our true national religion.

State-of-the-art semiconductor development & manufacturing are rightly considered critical to Nat’l Defense, so it’s quite understandable why Washington & the MIC are concerned.

Yes, “national defense” is the carve-out of our state religion.

SW

I have no problem with your comment. Guns or butter . . .

Semiconductors are the basis for the fourth industrial revolution.

Chips are the backbone of our digital economy. We must rebuild the American chip industry or suffer the consequences

Manchin agrees to a new deal on climate and taxes

NPR – July 27