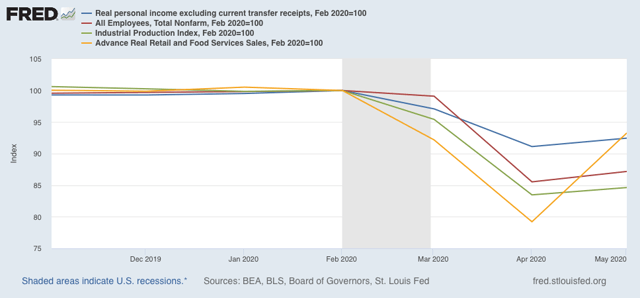

All 4 coincident indicators of recession improved in May vs. April

All 4 coincident indicators of recession improved in May vs. April

With this morning’s release of personal income and spending, we now have all 4 coincident indicators for May that the NBER uses to determine whether the economy is in a recession or recovery/expansion. And all 4 improved from their “most horrible” readings in April.

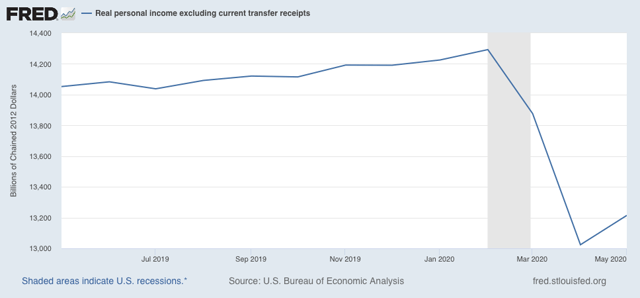

A recession is a generalized downturn in production, employment, sales, and income. The “income” metric that the NBER uses is “real personal income excluding current transfer receipts,” (basically, government program payments to individuals) and as shown in the graph below, it improved from April:

Still a horrible decline from February, but “less horrible” compared to April.

Since industrial production, nonfarm payrolls, and real retail sales also all improved in May from April, that makes it 4 for 4 among the coincident indicators:

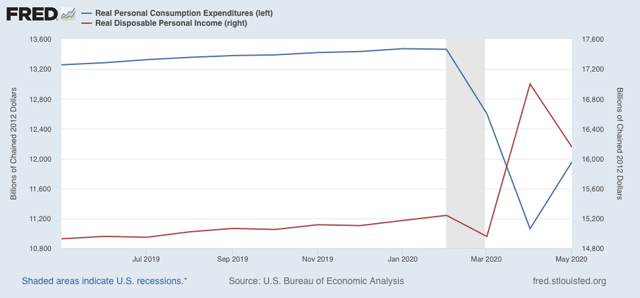

Real disposable personal income (red in the graph below) declined in May from April but was well ahead of previous months. This probably represents the delayed receipt and cashing of some of the one-time $1200 stimulus checks distributed by Congressional Act. Real consumption expenditures (blue), however, increased significantly, probably reflecting in part spending of that stimulus money by consumers, and partly spending by those called back to work:

In short, in May the situation was still horrible, but “less horrible” than April. That would qualify for the beginning of a recovery by economists’ definitions, *provided* there is no renewed downturn. And as the coronavirus continues to wreak more havoc in the States that have recklessly reopened – or simply let their guards down – a renewed downturn is very much a possibility, and almost a certainty if Congress does not extend the enhanced unemployment program by the end of July.

these are the inflation adjusted (2012 dollars) figures for personal consumption expenditures for the months October through May

13,388.3 13,419.9 13,433.2 13,471.6 13,463.2 12,602.0 11,062.2 11,954.8

that came from table 7 in the full release and tables pdf, which one accesses through the report’s main page

https://www.bea.gov/data/income-saving/personal-income

those figures represent ~69.4% of GDP for each month, and the BEA computes the quarterly change in PCE from a simple average of the 3 months in the relevant quarters….

hence, the 1st quarter saw PCE fall at a 6.8% rate, which accounted for 4.7 percentage points of the 5% drop in the 1st quarter’s GDP…

here’s the math for the 6.8% 1st quarter drop in PCE:

1- (13,179.0 / 13,413.8 ) ^ 4 = 0.06820

so, by averaging the 2012 dollar figures for April and May, 11,062.2 billion and 11,954.8 billion respectively, we can get an equivalent annualized PCE for the two months of the 2nd quarter that we have data for so far….when we compare that average of 11508.5 billion to the 1st quarter real PCE representation of 13,179.0 billion, we find that 2nd quarter real PCE has fallen at a 41.85% annual rate for the two months of the 2nd quarter we have data for at this point…(again, note the math used to get that annual growth rate: 1 – ((( 11,062.2 + 11,954.8) /2 ) / 13,179.0 ) ^ 4 = 0.418506)….that’s a pace that would subtract 29.06 percentage points from the growth rate of the 2nd quarter by itself, with that computation based on the unlikely assumption that there’d be no improvement in June PCE from the April-May average…but even if June’s PCE improves to pre-recession levels, we’re still looking at 2nd quarter PCE dropping at nearly a 30% rate and knocking 20 percentage points off of 2nd quarter GDP…

in addition to that, April and May’s trade figures are much worse than those of the first quarter, and will likely clip another 1 or 2 percentage points off 2nd quarter GDP….we may get a GDP boost from residential construction, but that will likely be more than offset by other investment declines, ie both well drilling and completions are the lowest on record, and the US rig count has fallen to 30% below it’s prior all time low…

point is, with a ~20% decline in 2nd quarter GDP already baked in, i can’t see NBER declaring that the recession ended in May, even as mistake prone the NBER has proven to be…

To counter the downtrodden economy, Trump exaggerates its pre-coronavirus greatness

Boston Globe – Jim Puzzanghera – June 27

Trying to revitalize his struggling reelection campaign, President Trump has been unequivocal in describing the robustness of the US economy under his watch before the coronavirus outbreak devastated it.

“We built the strongest and most prosperous economy in the history of the world,” he said at an Arizona rally on Tuesday.

Unequivocal, but untrue.

While the record-long economic expansion that began in 2009 continued under Trump and unemployment was near historic lows last winter, it wasn’t the best period in American history, let alone the world’s. Though economists say it’s difficult to declare the top US stretch, several were better, including the early 1950s, when growth approached 9 percent one year — triple the best annual performance under Trump — and the unemployment rate hit a record low of 2.5 percent.

By his own standard from the 2016 campaign — achieving 3 percent or more economic growth in at least one calendar year of a presidential term — Trump’s stewardship has been no better than Barack Obama’s.

“It was a good period. It definitely wasn’t the best in history,” Michael Bordo, an economics professor and director of the Center for Monetary and Financial History at Rutgers University, said of the pre-pandemic economy. “That’s a huge exaggeration.”

The frequent boasts by Trump are an attempt to run on an exaggerated characterization of the economy of the past instead of the downtrodden economy of the present. Trump warns that only he can lead a bounce-back and even claims that one one has already begun with the lifting of lockdowns he encouraged despite warnings from public health officials that relaxing social distancing and other restrictions could lead to the type of virus resurgence now taking place in numerous states.

“Unless my formula is tampered with, we will soon be in a stronger position than we were before the plague came in from China,” Trump said at a White House event on June 16.

There is another formula Trump is hoping to alter: defeat for presidents who deny economic reality.

“The American people understand what a bad economy is. They feel the pain,” said Allan Lichtman, a political historian at American University. “You can try to explain it away all you want, but it’s never worked well.”

Herbert Hoover prematurely declared the Great Depression over in 1930, and his vice president boasted that “good times are just around the corner.” They lost big in 1932 as the Depression continued to rage. George H.W. Bush said that “I happen to think the economy is better than most of the people in America think” as the country struggled with unemployment that rose to nearly 8 percent in 1992. He lost that year to Bill Clinton, whose campaign mantra was “it’s the economy, stupid.”

Lichtman has used a system of 13 metrics he calls “the keys to the White House” to correctly predict the winner of every presidential election since 1984. Short-term and long-term economic performance by the party in power are two of the keys. They were positives for Trump before the pandemic hit, Lichtman said, but now will most likely be negatives after second quarter economic data are released this summer.

“The keys are based on reality. They’re not based on what candidates say,” he said. “Good times don’t guarantee a win, but bad times pretty much guarantee a loss when combined with other factors.”

If those two economic metrics turn negative for Trump, they would join existing negative ones, including on social unrest, scandal, and lack of foreign policy success, to predict a loss in November, Lichtman said.

The US economy contracted at an annual rate of 5 percent in the first three months of this year, ending the longest expansion in US history. That was before the pandemic fully hit the country. Forecasts are that the economy has contracted at a stunning 35 percent annual rate from April through June. That would be by far the worst quarterly performance since the United States began tracking the figures in 1947 and virtually guarantee an overall economic contraction in 2020.

Unemployment shot up to 14.7 percent in April as nearly 21 million jobs were lost. The rate improved to 13.3 percent in May after the economy surprisingly added 2.5 million jobs. But the Bureau of Labor Statistics noted the rate likely was understated by about 3 percentage points because of a classification error that appears to be related to the challenge of conducting the household survey during the pandemic.

The downturn came as the economy remained stuck in a rut of middling performance despite Trump’s boasts. Growth was 2.3 percent last year and was expected to be about 2 percent this year before the pandemic. That was the same lackluster level as during most of the recovery from the Great Recession and alone gives lie to Trump’s claim that he presided over the greatest economy ever. …

https://cepr.net/airline-executives-have-problems-with-arithmetic/

June 26, 2020

Airline Executives Have Problems with Arithmetic!

By Dean Baker

It turns out that it is not just Donald Trump and economics reporters, but airline executives also have trouble with basic arithmetic. We learn this from a Washington Post piece * discussing the extent to which airlines are changing their practices to allow passengers to maintain some distance on flights.

The piece discusses various airlines policies and then concludes with some wisdom from the CEO of Jet Blue:

“ ‘You’re going to definitely have to sit next to a stranger again, I’m afraid, on a plane,’ JetBlue chief executive Robin Hayes said during a Washington Post discussion in late May. ‘Because of the economics of our industry, most airlines have a break-even load factor of 75 to 80 percent, so clearly capping flights at 55 to 60 percent, which is what we’re doing right now … is not sustainable.’ ”

The problem with Mr. Hayes assertion, as fans of arithmetic everywhere know, is that the “break-even load factor” depends on the price passengers are willing to pay. In the event that passengers are willing to pay a premium to not get a case of coronavirus with their flight, then an airline can break even with a lower percentage of its seats filled.

It may be the case that Hayes has evidence that people will not pay more to ensure their safety, but that is the central issue here. The piece is written as though people would not pay extra money for their safety, if this is really the case, then there should have been some discussion of the evidence.

* https://www.washingtonpost.com/travel/2020/06/26/airlines-tried-social-distancing-board-many-that-experiment-is-ending/

anne:

Having explored this on other occasions, there are other factors in play here. The damn planes are just too big. Airlines need to utilize more capacity in order to break even which is very difficult to do on large planes. I will be boycotting United and American and pay the extra cost in a cheap seat to have some degree of safety.

“Estimates are that operating A380s costs between $26,000 and $29,000 per hour. By contrast, an average flight on an American Airlines 737-800, which can hold 160-175 passengers and has a range of about 2,900 miles, costs $2,180 per hour.” Forbes, 2017

The Forbes article gives a hint, this issue is not new. The larger the plane the higher the operating cost requiring more passengers or freight to breakeven. A few decades ago, we went from smaller to bigger to minimize cost, reduced the numbers of flights, places flown and created hubs. Plague has changed the dynamics and people will not risk contracting Covid unless they are stupid which appears to be more the case witnessed by the spikes in contracting Covid over the last few weeks. Those who thought they would only be sick and survive are discovering Covid has a lasting impact on human organs.

Once again the CDC and the government has failed citizens by purposely minimizing the impact (due to age) on people who contract Covid. By destroying the supply chain for medical supplies, the manufacturing of medical supplies and pharma domestically, and justifying both using a cost driving analysis and blaming labor; we were again endangered by government sponsored corporate interests (spare me the neoliberalism attack. Over my 50 years in manufacturing and supply chain, I can explain in detail what has occurred. The rest of you spouting the Neo-BS hardly have a clue as to what started since Reagan).

I will be boycotting American and United and writing their CEOs on how they are placing us at risk. You should consider it also.

(How to fly during the present unpleasantness.)

Worried About Coronavirus? Turn to Private Jet Service!

NY Times – May 30

Commercial air travel has plummeted in the pandemic, but interest in private jet service is surging, particularly among people who have not paid to fly privately before.

For years, jet service providers have ferried corporate executives and wealthy leisure travelers who paid high fees for the privacy and security. Now, those same companies are shifting to meet rising demand from people worried about getting on a commercial flight. …

NetJets, the largest private jet operator in the world, is seeing a rush in interest from new customers, said Patrick Gallagher, its president.

“May is on track to be the best month of new customer relationships that we’ve seen in the past 10 years,” Mr. Gallagher said.

Competitors are experiencing the same rise. Magellan Jets has seen an 89 percent increase in new customers from mid-March to this past week, said Anthony Tivnan, its president. He added this was coming off a strong 2019, when the company’s revenue was up 34 percent from 2018. …

Sentient Jet, a private aviation company that offers flight hours, reported that it sold 5,000 hours in April, or the equivalent of about $30 million in flying time, significantly more than the $25 million it sells in a typical month. More than 2,500 of those hours were bought by people new to private aviation.

Andrew Collins, chief executive of Sentient Jet, said three-quarters of his company’s flights since March had been by individuals and families, up from 40 percent before the pandemic.

Mr. Collins said he had not expected the increase. In the 2008 financial crisis, private flying fell off quickly and took years to rebound. But the current crisis was set off by health concerns, not the financial markets, and demand for private flying has continued.

In April, he expected to book 200 to 300 flight hours, but flight time was actually just under 1,000 hours. “We’re seeing 50 percent new customers,” he said, as people buy cards to use now or save for later.

Worries over the environmental impact of flying privately may have taken a back seat as well.

“Concerns about opulence and concerns about environmental issues are gone,” said Mr. Gallagher of NetJets. Many wealthy people put up with flying commercial because they had benefits like first class, TSA PreCheck and a status that allowed them various perks. “But now,” he said, “there are a lot of people out there who don’t want to fly commercial if they’re part of an aging population or have underlying health concerns.”

A person on the average commercial flight has about 700 points of contact with other people and objects, according to a recent analysis by the consulting firm McKinsey, but private flights have only 20 to 30. …

Run:

“Estimates are that operating A380s costs between $26,000 and $29,000 per hour. By contrast, an average flight on an American Airlines 737-800, which can hold 160-175 passengers and has a range of about 2,900 miles, costs $2,180 per hour.” Forbes, 2017

The Forbes article gives a hint, this issue is not new. The larger the plane the higher the operating cost requiring more passengers or freight to breakeven. A few decades ago, we went from smaller to bigger to minimize cost, reduced the numbers of flights, places flown and created hubs….

[ Really interesting and important, and generally unknown to me although I was aware of the creation of hubs but never considered why they should be necessary. The logistics suddenly strike me as entirely problematic. ]

Run:

Interestingly, China has fully developed an airliner, the ARJ21, and begun delivery to domestic airlines, with orders by a number of foreign airlines. The ARJ21 is a 78-90 passenger craft, an efficient craft from what I have read, and I am suddenly wondering if China might change the logistics of flying from an American model.

Besides, I have never read of Chinese “hubs” and given the general logistics efficiency emphasis in China, hubs may not have been used even before the coronavirus changed the nature of flying.

What then of the domestic-developed ARJ21? Could this craft decidedly make for a different experience from the American model?

https://www.globaltimes.cn/content/1191238.shtml

June 10, 2020

Chinese carrier to buy 100 homegrown aircraft

________________________________

Chinese carrier China Express announced on Wednesday that it has signed a framework agreement with Commercial Aircraft Corporation of China (COMAC) to buy and operate a total of 100 planes – including ARJ21-700 planes, China’s first domestically made regional jetliner, and C919 commercial airliner planes – starting from 2020.

In addition, the two companies will cooperate in exploring overseas markets, in particular in markets along the route of the Belt and Road Initiative and in Africa. They will also integrate resources to build an industrial ecosystem for China’s homegrown civil airplanes, according to a filing China Express sent to the Shenzhen Stock Exchange.

Other areas of cooperation include jointly promoting the design and optimization of aircraft, and exploring new services and maintenance models, the filing noted. China Express said that the purchase will help the carrier to steadily expand capacity and market size.

Lin Zhijie, a veteran market watcher, told the Global Times that the agreement shows that China’s self-made airplanes have started market-oriented development and operation. “It has some special significance as China Express is a privately owned airline,” Lin noted.

An employee of China Express said that Chinese carriers should take the responsibility to support the development of homegrown aircraft, industry news website reported. “For an airplane’s market development, building and being used is equally important.”

On Wednesday, COMAC also delivered three ARJ21 airplanes to Chengdu Airlines, Jiangxi Air and Genghis Khan Airlines, respectively, news website yicai.com reported.

As of the end of April, COMAC has delivered 25 ARJ21 aircraft to the three aforementioned carriers. It is also expected to deliver to China’s three major carriers – Air China, China Eastern Airlines and China Southern Airlines – their first ARJ21 airplanes by the end of June, according to media reports.

So far, ARJ21 planes have flown on 50 routes, safely transporting more than 820,000 passengers.

Logistics efficiency in flying does not immediately strike me as meaning the use of a few hubs and transport of the largest number of passengers in a flight. China has just finished and is operating an independent satellite global positioning system. Chinese air transport is slated to be 5G determined this year, which means solving harder logistics problems.

I am just playing with ideas, but I wonder…

Things could return to ‘normal’ once

an effective covid vaccine is available.

Will airlines still be around then?

Otherwise, widespread flying, as we used

to use to travel far, is ill-advised, obviously.

Whether it’s 100 people on a packed plane

or 300.

Luxury private-jet based flying will be the

way to go across country. Perhaps also

across oceans. For those wealthy enough.

I calculated the other day that to cross the

US, from one coast to the other, should take

about 4 days, conservatively, sleeping in the

car presumably. Mrs Fred says we would have

to take our chances in an airliner. As if.

Fred:

If and when we sell our home, our new destination is 1700 miles away and occupied by rabid mask less Covid dummies. I agree traveling by plane used to be a pleasure. No cost for luggage. no cost for better seating. Fill the back of the bus first and going forward. All of that is changed as you take your life in your own hands by flying. On some airlines now you may be threatened more than on others.

We will probably drive and take our time. We are in no hurry for once and it may be our last time driving any long distances. We coulkd drive down there at half the cost of a one way ticket.

“occupied by rabid mask less Covid dummies” sounds like Arizona, run…

China is finishing testing and will soon have a larger passenger aircraft by the way, the C919:

http://www.xinhuanet.com/english/2020-06/29/c_139175394.htm

June 29, 2020

China’s C919 jet conducts high-temperature test flights in Xinjiang