Why negative transportation indexes don’t support a recession call

Why negative transportation indexes don’t support a recession call

Every month for at least the past half year there is a spate of bearish economic commentary that relies upon one or both of two metrics: AAR rail carloads and/or the Cass Freight Index.

I have a post up at Seeking Alpha showing why the first measure is not a representative slice of transport as a whole, and the second has a history of being very volatile and with a slew of negative readings in the teeth of continuing expansions.

As usual, clicking on the link and reading helps reward me with a $ or two for my efforts.

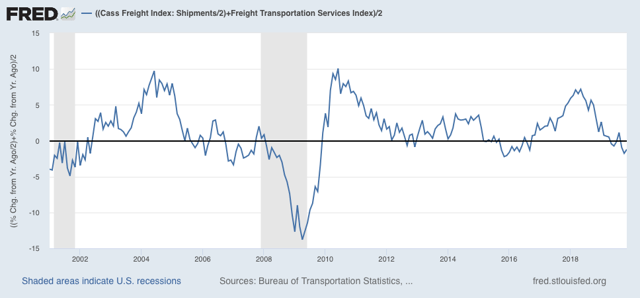

Addendum: after I put together and posted the article, I came up with the idea of averaging the Cass Freight Index and the Dept. of Transportation’s Freight Index after adjusting for the former’s volatility (shown below). It gives us an even less noisy overview of the transportation sector, although it still does go negative during slowdowns without there being a recession. In any event, none of the current negative readings are sufficiently below zero to accord with recessionary readings over the indexes’ short history:

Have you thought about how the rapid growth of online shopping impacts the transportation incidences.

With online shopping the final stage is shipping directly to the consumer rather than the retail outlet. I ‘m an old man that takes probably too many different drugs. But I now get them online and have them shipped

to my home rather than going to the drugstore.

Amazon now has numerous warehouses and/or transshipping facilities so it is obviously large enough to significantly impact the data. Tesla does not even have a chain of car dealers.

So the fundamental question is whether or not the shipping indices are measuring the same universe that they did in earlier cycles.

Bad core real final demand ain’t good. 4th quarter was the worst in 4 years. Bodes not so good in the 1st quarter.