Higher wage growth for job switchers: more evidence of a taboo against raising wages?

Higher wage growth for job switchers: more evidence of a taboo against raising wages?

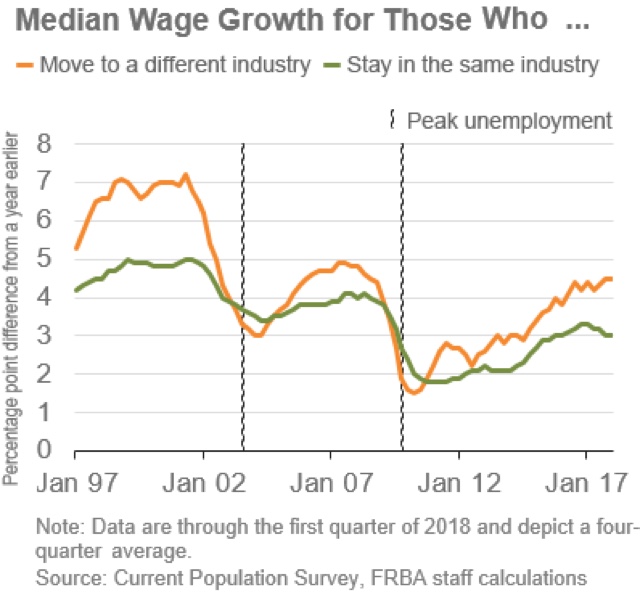

Yesterday the Atlanta Fed published a note touting the wage growth for those who quit their jobs and transfer to a different line of work, writing that:

Although wages haven’t been rising faster for the median individual, they have been for those who switch jobs. This distinction is important because the wage growth of job-switchers tends to be a better cyclical indicator than overall wage growth. In particular, the median wage growth of people who change industry or occupation tends to rise more rapidly as the labor market tightens.

The following graph was posted in support of this point:

Essentially the Atlanta Fed is highlighting the orange line as a “better cyclical indicator.”

Is it? There’s no doubt that wage growth among job switches declined first in the last two expansions. But I would want to see a much longer record before being that confident.

Because what I see in the above graph is a decline among job keepers (the green line) that is only matched by those declines presaging the onset of the last two recessions. Meanwhile the orange line, while still rising, has flattened.

In fact I think the Atlanta Fed’s graph mainly shows evidence of what I highlighted last week as an emerging “taboo” against raising wages — i.e., a stubborn refusal to raise wages even if it would lead to even higher output and gross profits for a net gain.

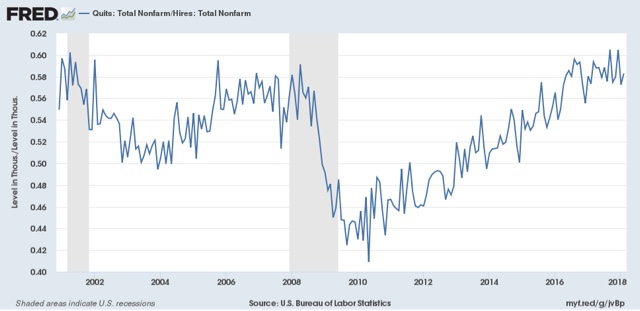

Once again the JOLTS data gives us a good proxy. If wage growth is increasing at a “normal” rate compared with previous expansions, there shouldn’t be an inordinate need to change jobs in order to get a raise, i.e., a rate higher than previous expansions. Thus the ratio of job changers who quit vs. the number of actual hires should be equivalent to similar stages in those expansions. If, on the other hand, employers have become inordinately stingy, quitting is almost essential to get ahead, in which case the ratio of quits to hires should be higher than normal.

Here is what the data shows:

For the last several years, Quits have been in the range of 58%-60% of hires, the highest since 2001, and specifically higher than the 56%-58% peak of the last expansion.

In other words, it looks like what the Atlanta Fed’s graph is showing is that employees are reacting to the taboo against raising wages by quitting their jobs and moving to employers in fields that are already paying more.

In my greater than 50 years of employment this has been truism: “In other words, it looks like what the Atlanta Fed’s graph is showing is that employees are reacting to the taboo against raising wages by quitting their jobs and moving to employers in (their fields other locales or) fields that are already paying more.” (My add since changing fields and improved wages are not a given.)

Changing jobs was the norm for faster wage increases.

I agree, it is typically much easier to get more money by changing companies than by staying inside a company.

Staying at your company is equivalent to an athlete taking “the hometown discount.”

You’ll be asked to make lateral moves that keep you in the same pay band, there are administrative processes to limit the number of jumps you can make (one company I was at encouraged people to move roles after 24 months, but wanted finance people to rotate between “pillars,” generally as a lateral move, and had a hard 6% increase limit internally on moves that had to be signed off by the equivalent of a business group CFO to waive it, and that could only get you 10%, merit increases were rubber banded, the same rating/performance would get you a larger % increase if you were at the bottom of a pay band than if you were near the top, none of these rules applied if you were coming from outside the company, and it was a fairly common maxim that if you liked the company and wanted more money it was a good idea to spend a year elsewhere then come back; another company I’ve been at encouraged moves every three years, but has less restrictive merit rules; both companies have strong HR limits opposing off-cycle pay increases), and lock-in to a career path can be higher then what would be suggested by your skills and education.

The alternate path is to make jumps externally around every 18 months for about 5 years then find a place that you like. If you can swing that scenario, you’ll definitely end up with more money than someone who stayed at the same company from the time they were out of college. The downside is that a series of short stints can be disqualifying if there is a large stack of resumes on the table.