Hospital Pricing Rising Faster for Private Insurance?

Private healthcare insurance polices and pricing is more varied than Medicare. No surprise there. The only thing you may deal with in having Medicare is Supplemental. The ACA should be similar to Medicare pricing. ACA Marketplace plans and Medicare differ significantly in costs and pricing (Supplemental). Too much freedom or leeway was given to the ACA based upon costs and profits, The market place is not doing a good job in price control and neither is competition.

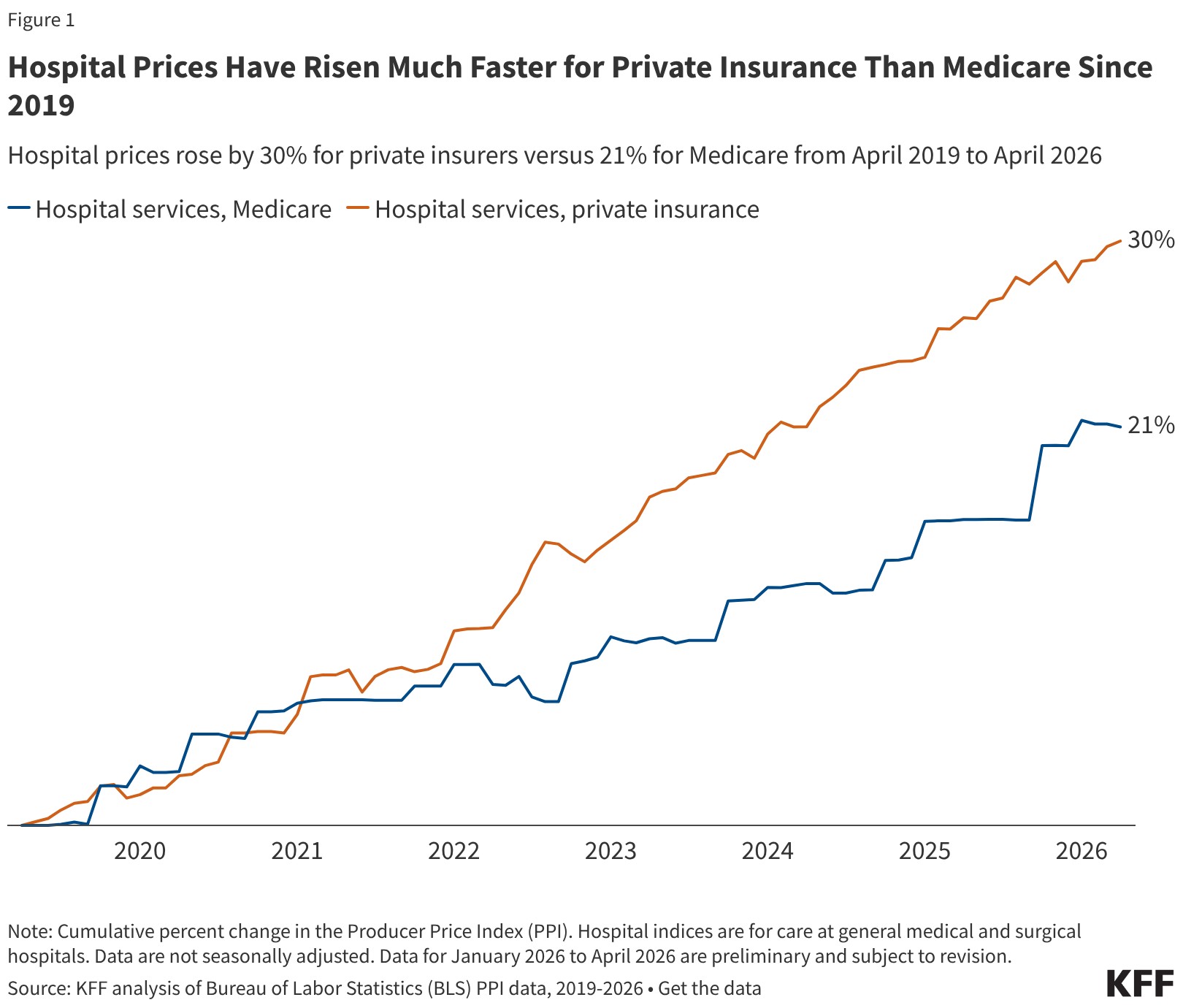

It is no or little surprise, hospital pricing is rising rapidly for Private Insurance users. No surprise there either. Medicare has greater control over pricing. Read on . . .

Hospital Prices Have Risen Much Faster for Private Insurance Than Medicare Since 2019, KFF

by Jamie Godwin and Zachary Levinson

May 18, 2026

Health care costs are a top concern for the public, and there is widespread interest among lawmakers in making health care more affordable. Attention has increasingly focused on hospitals, which represent nearly one third of total health care spending and accounted for 40% of spending growth from 2022 to 2024. Hospital spending reflects both the prices paid for services and the volume and intensity of care delivered, and trends in both factors have implications for affordability and spending growth. The prices paid by private insurers are higher than Medicare rates on average—e.g., nearly double traditional Medicare rates for hospital services when averaging across studies, according to a prior KFF review. The prices also vary across regions and across hospitals and payers within regions. These high prices affect households through higher premiums and cost sharing obligations and reduced wages for those with employer-sponsored health coverage.

There has been some discussion at both the national and state level about policies that could rein in hospital prices. One set of policies aims to do so by promoting competition and reducing consolidation in provider markets. A substantial body of evidence shows that hospital market consolidation has contributed to higher prices, with unclear effects on the quality of services provided. Another set of policies would rein in prices more directly, such as by capping the prices that providers can charge. For example, Indiana recently enacted a law that will eventually cap private insurance prices for the state’s nonprofit hospitals, and Oregon has capped hospital prices at 200 percent of traditional Medicare rates for its state employee plan since 2019.

To inform policy discussions related to hospital prices and price regulation, this brief describes the growth of prices paid by private insurers for hospital care relative to increases in Medicare payment rates from April 2019 through April 2026, using data from the Bureau of Labor Statistics (BLS) Producer Price Index (PPI). The analysis begins in 2019 to fully capture changes in prices during the pandemic. See Methods for more detail.

Private insurance prices for hospital care rose 30% from April 2019 to April 2026 compared to a 21% increase in Medicare rates (Figure 1). Put differently, private insurance prices grew 47% more quickly than Medicare rates over this 7-year period. Private insurance prices grew at a similar pace as Medicare rates from April 2019 to April 2020, but grew more quickly than Medicare rates each year from April 2020 to April 2025, before increasing less quickly than Medicare rates from April 2025 to April 2026. These patterns are broadly consistent with prior research that finds faster price growth for private insurance than Medicare over time, with some variation across time periods. Private plans pay much higher rates than Medicare for hospital services according to prior research, and this analysis suggests that the gap has increased over time.

Private insurance prices for hospital care are the result of negotiations between hospitals and insurers. Increases in private prices over time can reflect changes in the cost of providing care and in the bargaining power of hospitals relative to insurers, among other factors. Hospital markets have become increasingly consolidated, with one or two health systems controlling at least 75% of the market for inpatient hospital care in the large majority of metropolitan areas (83%) in 2024, according to KFF analysis, contributing to higher prices. Large increases in labor and supply expenses during the pandemic have likely pushed providers to negotiate for higher prices (economy-wide inflation jumped in March and April 2021 before reaching a peak in June 2022). However, contracts between hospitals and insurers are only periodically renegotiated, and often last for multiple years, meaning there may be a lag before any effects of higher input costs are fully reflected in higher prices.

In contrast, traditional Medicare hospital prices are updated annually by the Centers for Medicare and Medicaid Services (CMS), primarily through the Inpatient and Outpatient Prospective Payment Systems (IPPS and OPPS). These changes are based on factors and methods described in law and regulation. Medicare IPPS and OPPS updates are based partially on estimates of increases in hospital services input costs, which are affected by overall inflation. There is some evidence that rates paid by Medicare Advantage plans for hospital services (incorporated with other private Medicare plans in the Medicare but not private insurance PPI) are generally close to rates paid by traditional Medicare. Increases in prices paid by Medicare Advantage insurers have likely been aligned with changes in traditional Medicare rates over time.

One factor that slowed Medicare growth is that the program underestimated inflation in recent periods when prospectively setting rates (e.g., inflation in 2022 was much higher than expected when hospital rates were set for that year), according to the hospital industry and others. Nonetheless, CMS has noted that its forecasts have tended to be close to actual inflation on average when looking over longer periods for the IPPS hospital market basket (see Methods for more detail).

Various other factors may have restrained Medicare price growth during the study period, such as the productivity adjustments enacted under the Affordable Care Act, which reduce the growth in traditional Medicare rates over time under the assumption that hospitals are becoming more efficient at delivering care. As another example, sequestration, which is an automatic reduction in Medicare payments required under budget rules, was temporarily suspended during the pandemic beginning in May 2020 but gradually reintroduced in April and July 2022, likely contributing to the increase and decrease in the Medicare PPI during those periods.

I have been hashing through the issue of healthcare for a few years now. I am starting to see mor articles on healthcare costs. If they are of reasonable length, I will bring them to Angry Bear. I do prefer articles with graphs and tables. They go a long way in making a point on the issue being presented.

The late Uwe Reinhardt offered cogent, deeply informed analysis of the US healthcare system. I don’t think his conclusions have been superseded by anything that has happened since his death. If anything, his understanding of the commodification and monopolization of healthcare services has been proven more germane over time.

DEb:

Are you traveling a lot? I see several numeric locations ie(fake one: 123.22.344.95) and no-reply as location. The system may be confusing you as a hacker, etc. I have not banned you or kicked you out. It might be the systems location determination which is treating you like a first time commenter..

DEb:

It has been a while since I looked at healthcare. But as usual, costs are outstripping income in percentage of increase.