“Where Assets (and “Money”) Come From”

Steve Roth — Wealth Economics

When you look at the left side of an entity’s balance sheet or its brokerage account statement, you see a list of things that the entity owns, with an estimate of what those assets are worth. The estimates are generally at current market value — what somebody would pay for those assets at that moment.

Looking back over a household’s year-in and year-out flows, plus revaluation/capital gains, it’s fairly easy to understand where that household’s (your) assets “came from.”

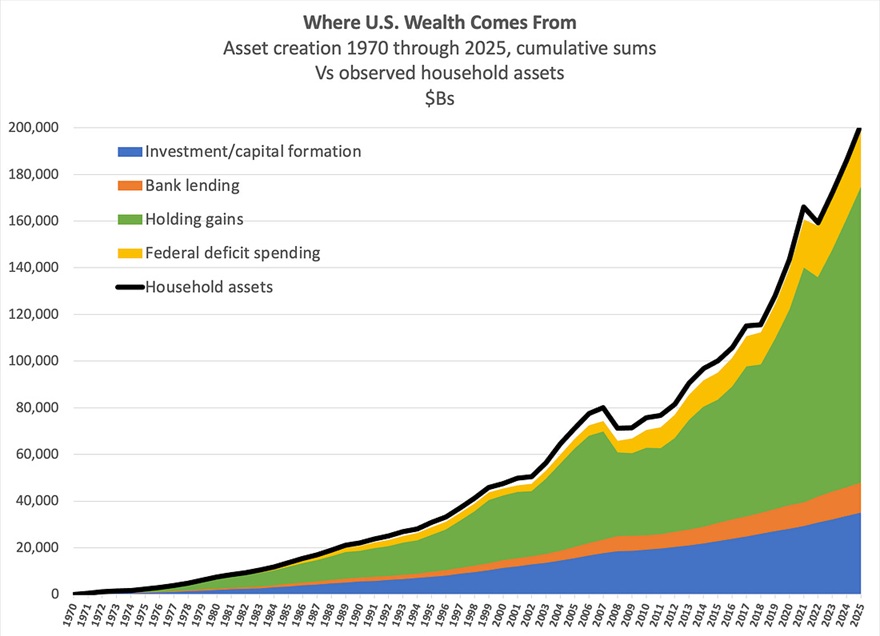

But for aggregate sectoral assets — the total for the US household sector or the total domestic sector including firms and government, the understanding is not so obvious. In the big picture there are four mechanisms that create new assets in the world — “out of thin air,” as the saying goes. Some of those new assets are “money,” but most are not.

The first thing to notice: the colored areas, summed, match the black line pretty darn well despite some measurement discrepancy. These four asset-creation mechanisms explain all the aggregate asset accumulation. The mechanisms are explained below.

But first, why are we looking at the household sector? Because, in an accounting sense at least, the household sector owns everything. It’s the top of the accounting-ownership pyramid. Firms can own shares in firms, for instance (ad nauseum), but ultimately households own it all.1

Because: households (and nonprofits) don’t issue equity shares. Nobody can own households. (Not since 1865, anyway.) It’s an asymmetrical, one-way ownership relationship. The household sector owns the firms sector, and in an important sense even the government sector.2 It’s where the ownership-accounting comes “home.” All the assets owned by other sectors are “telescoped” onto the household-sector balance sheet. That’s how the b.101 and s.3 household balance sheets work.3

With that understanding, let’s look at the four mechanisms of asset creation. Each works somewhat differently.

Investment. This is mostly done by firms (which are owned by households). In the national-accounting construct it’s done almost purely by firms (and government — local, state, and federal).4 When a firm spends — pays people or other firms to produce new, long-lived, real-world (productive) stuff, the payment itself does nothing to increase collective assets; it just moves them around. The payer has less assets, and recipient has more, netting to zero change in aggregate.

But! The payer now owns the newly created stuff, and posts its value to their balance sheet (generally at cost; it may later be marked to market, for instance when a remodeled building is re-appraised to get a loan, or it’s sold). That accounting event, posting the new asset to the balance sheet, means there are more assets in the world. Voila.

As that new stuff wears out, decays, ages, becomes obsolete, its value is depreciated on balance sheets; this is also called “consumption of fixed capital.” So the blue slice here is net investment/capital formation: gross capital formation minus capital consumption.

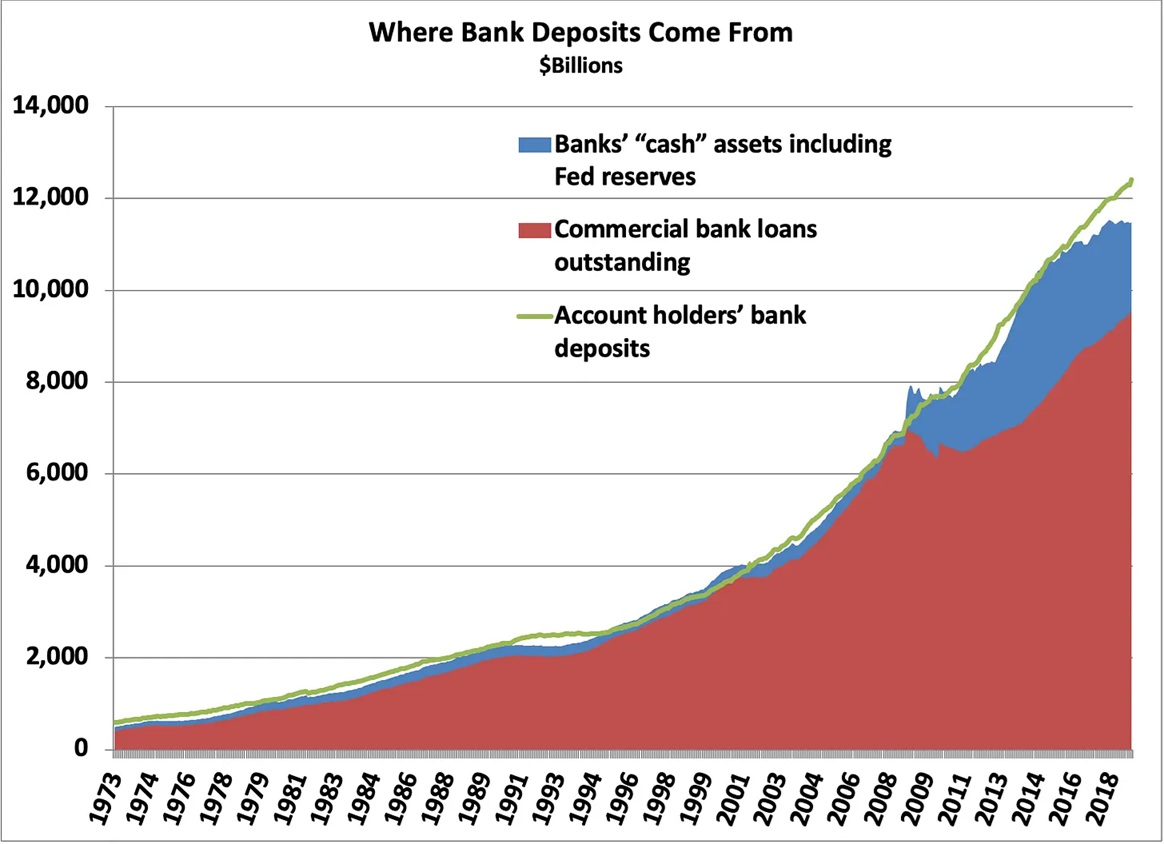

Bank lending. Borrowing adds asset and liabilities to the borrowers’ balance sheets, in equal measure. The borrowers issue new IOUs (assets for the banks), and the banks issue new bank deposits (assets for the borrowers). Loan payoffs do the same, in reverse. So net bank lending, the orange slice, creates new assets in nonbank private-sector accounts.

This, in fact, used to be the only way that new fixed-price “money” assets (bank deposits and an ignorable amount of physical cash) were created in aggregate. Quantitative easing starting 2008 changed the picture, but banks still “print” most of the new money assets, by lending.5 Before QE, only bank lending created bank deposits/money.

Government deficit spending. When government spends it quite literally deposits money assets into private-sector bank accounts — payments for goods and services, transfers, and etc. If its outlays are more than it receives in taxes etc., it issues the new “extra” assets out of thin air. (Those new assets are offset by liability entries on the government balance sheet.)

A key understanding, though: this mechanism doesn’t end up creating new private-sector “money” assets (bank deposits). Because, Treasury simultaneously and constantly issues new bonds to match the deficit spending and swaps them for all that new money (which vanishes). To paraphrase Milton Friedman, banks and governments have both printing presses and furnaces.6

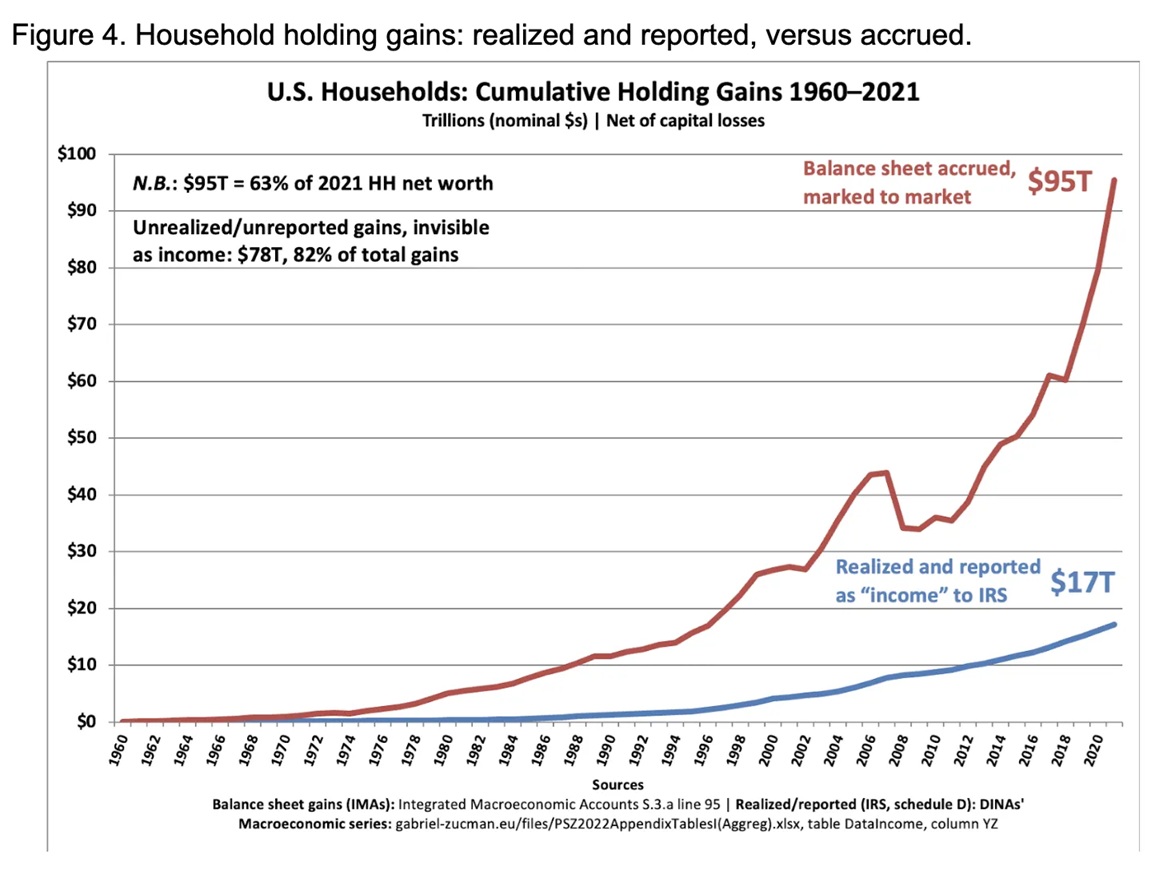

Holding gains. Also knowns as “capital” or “revaluation” gains. When a portfolio holder looks at their assets and compares them to previous years, they’ll almost always see (often extraordinary) asset increases that are unexplained by any flow measures across those years. Those increases come from pure accounting markup events: “marking assets to market.”7 Brokerage accounts do this constantly for portfolio holders, to show their current asset holdings’ total value. It’s immaterial whether the holders have “realized” any of those gains by swapping the appreciated assets for “money” assets. They’ve got more assets.

For me at least, this understanding of asset-creation mechanisms makes it much easier to think about some economic truths and truisms that you hear out there, many of which have never made sense to me (at all, or just “not quite”). I’ve highlighted three examples below. To keep this post short, and for those who might find it valuable, the links take you to questions I’ve asked of Claude AI, and its answers. I do not fully endorse those answers; they get some stuff wrong. But they get quite a lot right.

“The private sector can’t save unless the government runs a deficit.”

“Every asset has an offsetting liability.”

As always, I much appreciate comments, thoughts, and corrections from my gentle readers. Thanks for reading.

1 I’m ignoring the “rest of world” sector’s net ownership position in this explanation, for simplicity and clarity. There are significant conceptual and measurement issues to deal with there.

2 The problem here: unlike government’s liability side, the asset side of the government balance sheet is completely imponderable, impossible to calculate. What’s the (market) value of the judicial system? The Grand Canyon? The interstate highway system?

3 The B.1 table of “U.S. Net Wealth” (whatever that means) is an accounting Frankenstein monster. It presumes to tally the “real,” nonfinancial assets of each sector then sum them up. But for the firms and rest-of world-sectors, it just punts, unavoidably and necessarily using current equity market values rather than nonfinancial-asset values. (Its discrepancy from the B.101 net worth tally, BTW, is just the US Net International Investment Position.)

4 In the national-accounting system devised by Simon Kuznets & co in the 1930s, households are on the far side of the “production frontier,” so they pretty much can’t do investment spending. But some household investment spending aka “capital formation” is shoehorned into the household tables through back doors, via (actual and imputed) real-estate improvements by owners qua landlords, by accumulation of household durables (mostly vehicles) net of depreciation, and etc.

5 In QE, the Fed swaps newly-issued reserves for treasury bonds, with big banks’ broker-dealer departments effectively converting those reserves into fixed-price “money” assets (bank deposits) held by the nonbank private sector. This just changes that sector’s portfolio mix: more cash, less bonds, total assets unchanged. (With follow-on effects on prices of different asset classes, as portfolio holders try to react/rebalance/shed cash in a game of musical-money-chairs.)

6 When you lay down your credit card at a store, you and your credit-card company are “printing money” and sending it to the store’s bank account. When you pay off your bill, you’re burning money (and erasing your liability).

7 To see the quite massive accounting discrepancies that arise from ignoring these revaluation markup events, even (especially) at the highest levels of national accounting, see “Why the Flow of Funds Don’t Explain the Flow of Funds.” Focusing on the household sector specifically, see this recent release.