There are two components of quarterly GDP that are long leading indicators, giving us information about the economy 12 months from now. If you think, as I do, that it is likely there will be a new Administration in Washington next year, which will competently follow the science, then there is every reason to believe that by 12 months from now the pandemic will have been contained, and so the long leading indicators are more likely to be valid.

In that regard, this morning’s Q2 2020 GDP was not grounds for optimism.

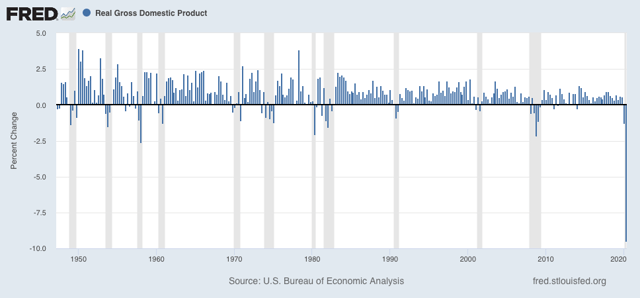

As an initial matter, the GDP decline of -9.5% annualized was the biggest decline since the Great Depression:

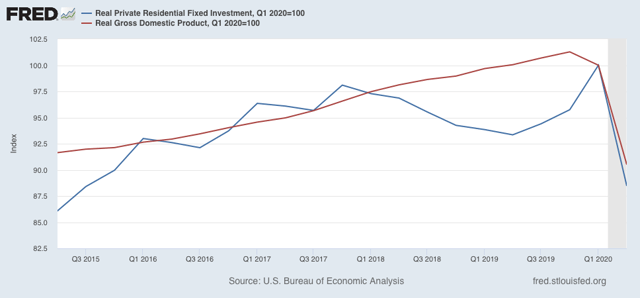

The two forward-looking components of GDP are (1) private fixed residential investment, and (2) corporate profits. Because corporate profits are delayed by one more month, I use proprietors’ income as a temporary proxy. Let’s look at each in turn.

Real private residential fixed investment decreased by over 10% q/q. Real GDP decreased a little less than 10%:

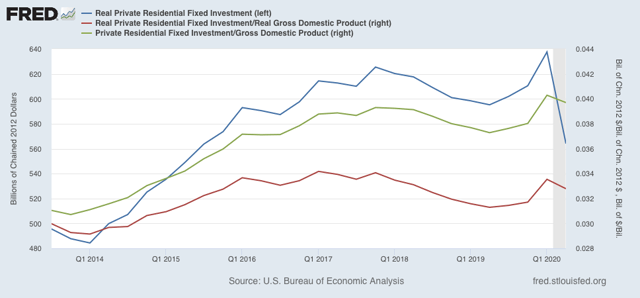

Thus real private fixed residential investment as a share of GDP declined slightly (red in the graph below) as did nominal investment as a share of nominal GDP:

This is a negative.

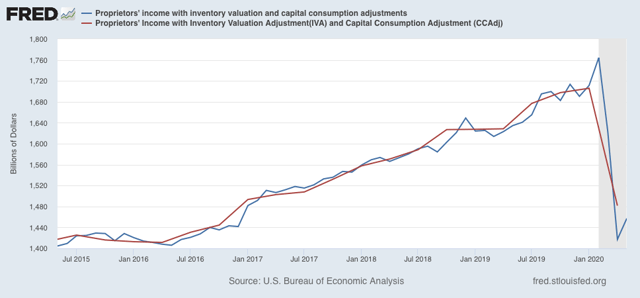

Meanwhile, proprietors income declined -13.2% in Q2:

Since the GDP implicit price deflator declined -2.1%, this was also a large negative.

In sum, both long leading indicators in the GDP report suggest that the economy will not be doing that well by summer 2021, even if the coronavirus is contained.

Again, where is the credible argument that a new federal President on January 20, 2021 is likely to make a significant difference in the evolution of this coronavirus pandemic in the United States? Competently follow the science? That is not an argument that any substantial federal policy changes will be forthcoming. I think the soundest assumption is that apart from messaging there will be no significant federal policy changes concerning this virus. Thinking that Trump’s response to date has been disastrous is totally understandable, but extrapolating to nearly a half year from now that there will be federal policies that would make a major impact if changed is not so likely. Yes it will make a huge difference for the future of the judiciary, for Iran policy, for federal oversight of state and local law enforcement and a lot of others. But it probably won’t make any significant difference if the number of cases and infection rates of March 20, 2021 are what concerns you. Do not freak out about coronavirus if Trump wins but you are welcome to do so in 20 other public policy areas.

Eric377: The credible argument is that the federal government can work with the states and media to get better control of COVID. Right now, we are on course for a million dead, maybe more, before we develop herd immunity, assuming such is possible. People will follow if someone will lead. Right now, our leadership in the Whitehouse is doing everything it can to encourage people to spread the virus and make it harder for those working against it.

It is still possible to use federal powers to onshore production of PPE. It is still possible to get OSHA, the USDA, the FDA and so on into developing and enforcing safe practices. It is still possible to get actual health officials and epidemiologists around the country to come up with a working plan. It is still possible to pressure governors to fight COVID as opposed to working to spread it.

Leadership is a strange skill. Leading is not quite the same as ordering people to do things, though certain types confuse the two. People actually want to follow. They know the power of working as a team. The problem is putting together a plan and a team that can win. (For a good study of this, read “Once An Eagle”, a cult classic in the officer corps.)

Right now, we have crap leadership. COVID is not going away for a while, but it can be rendered much less harmful. We know how to do it. Other nations have done it. The ones where the leaders are willing to fight do better than those that lay down arms. In the US, we have a president who doesn’t want to fight.

this is an interesting post, but i’m left wondering if normal ‘long leading indicators’ mean anything at all in this situation…

https://cepr.net/an-economic-survival-package-not-a-stimulus-package/

August 2, 2020

An Economic Survival Package, not a Stimulus Package

By Dean Baker

There continues to be enormous confusion about what we should be trying to accomplish in the next pandemic relief package. This is best demonstrated by Republicans’ obsession with getting people back to work, with a mixture of cuts to unemployment benefits and return to work bonuses.

Ignoring the questionable economic logic (there is zero evidence of large numbers of jobs going unfilled), this approach also ignores the reality of the pandemic. At the start of April, both houses voted nearly unanimously to support measures that were designed to make it possible for people to stay at home rather than work. At that time, we had roughly 35,000 new infections a day. Currently we are seeing well over 60,000 new infections a day, with the count crossing 70,000 in many recent days.

The comparison looks even worse if we pull out New York and New Jersey, both of which were overwhelmed by the pandemic at the start of April. Between them, they had roughly 15,000 new infections a day, which means the rest of the country was seeing close to 20,000. By contrast, at present both states have the virus relatively under control, which means that the new infection count in the country would still be over 60,000 a day, excluding New York and New Jersey.

This raises the obvious point: if Congress thought it made sense to allow, encourage, and possibly even require people to stay home rather than work at the start of April, how could it possibly make sense to push people to work at a time when the rate of new infections is more than three times as high, in areas outside of New York and New Jersey?

This is really a question of life and death. Tens of millions of workers have serious health conditions that mean they would be at considerable danger if they became infected. Tens of millions more workers would be putting into danger family members, with serious health conditions, if they became infected. As a result, a high percentage of the workforce has very good reasons for not wanting to return to work just now.

If we face the reality of the pandemic, we should not be designing a package to get people back to work, we need to design a package to keep them whole through a period in which tens of millions of people will still not be able to work because of the pandemic. This means that we want people to have the money to pay their rent or mortgage and to buy food and other necessary items. We don’t want them to be going out to restaurants and bars, to see movies or baseball games, or to fly away on vacations or go on a cruise ship.

There was considerable confusion on this point even back in March and April where many were referring to the bills passed by Congress as stimulus. Some were even pushing types of spending that could boost the economy. There was little reason to want to boost the economy back in April, nor should there be now. We want to make it so that people endure as little hardship as possible for now, and the economy to be prepared to start up as quickly as possible, once the pandemic is under control.

Of course, we should not be in this situation. Most of the economy was shut down from the middle of March to the middle of May, with major restrictions staying in place in the hardest hit areas well into June. These restrictions did largely bring the pandemic under control in places like New York, New Jersey, Maryland, Massachusetts, and Washington (both state and DC).

Unfortunately, many states did not take the need for restricting business seriously and began to open at the start of May. This is the reason that states like Arizona, Georgia, Florida, and Texas now have major outbreaks. California also now has a major outbreak, as lack of financial support from the federal government, coupled with political pressure orchestrated by Donald Trump in the form of “liberate California” protests, led the state to relax restrictions sooner than it should have.

It would be possible to talk about an economic reopening now, if we had been successful in bringing the pandemic under control, as is the case in Europe and East Asia, in addition to the Northeast in the United States. But we can’t make plans based on a reality that does not exist. The pandemic is more out of control than ever in most of the country. This means that we again have to plan for another period in which the economy will not be operating normally by design. We need to focus on keeping people whole.

The Shape of this Rescue Package …

August 3, 2020

Coronavirus

US

Cases ( 4,822,793)

Deaths ( 158,463)

https://www.nytimes.com/2020/08/03/nyregion/nyc-small-businesses-closing-coronavirus.html

August 3, 2020

One-Third of New York’s Small Businesses May Be Gone Forever

Small-business owners said they have exhausted federal and local assistance and see no end in sight after months of sharp revenue drops. Now, many are closing their shops and restaurants for good.

By Matthew Haag

If Biden Wins, He’ll Have to Put the World Back Together

The Atlantic – April 13, 2020

His post-pandemic agenda will have to be a master class in redesign.

If Joe Biden wins the election in November, he will likely be sworn in—perhaps virtually—under the most challenging circumstances since Harry Truman became president in 1945. The country will probably be in the end stages of a brutal pandemic and faced with the worst economy since the Great Depression. The Treasury will be significantly depleted. Millions of people will have lost loved ones, their jobs, much of their net worth. Hopefully a vaccine or an effective treatment will be closer to reality, and our national attention can shift to what comes next.

We judge our great presidents by how they managed harrowing trials and wars: Abraham Lincoln and the Civil War; Franklin D. Roosevelt and the Depression, followed by World War II; Ronald Reagan and the Cold War. But many of the bigger and less historically rewarding challenges are what come immediately after—how to rebuild and remake the country and engage in the wider world. Think about Ulysses S. Grant and Reconstruction, Woodrow Wilson and the League of Nations, Truman and the architecture to wage the Cold War, George H. W. Bush and the collapse of the Soviet Union. Some failed; others succeeded. All faced enormous obstacles explaining what just happened, what had changed, and how we must adapt. This is the category of presidency that Biden, or Donald Trump if he is reelected, will find himself in.

If Trump wins, the country can expect more of what we have seen in the initial phase of dealing with COVID-19—shifting the economic and health burden to the states and Congress, a lack of interest in international cooperation, and a refusal to critically scrutinize the response.

But what about Biden? The beginning of his presidency will have a unique logic and character that sets it apart from the early stages of the crisis. His first year will be shaped in various measures by the public reaction to the horrors of 2020, the national Rorschach test of seeing Trump’s silhouette finally from a remove, and a dawning reality of exceedingly difficult choices across the board.

Biden’s first and toughest challenge will be to address the badly frayed governance compact, in which citizens expect and trust the government to deliver on essential services. For decades, Republicans and Democrats have believed that the government needs fixing, albeit for very different reasons. Republicans tend to view much of the state apparatus, including regulatory bodies and social services, as inherently inefficient and run by entrenched, unaccountable bureaucrats. Democrats see our federal workforce as under-resourced and frequently subjected to quixotic and unreasonable demands from political leaders. However, many Americans, particularly those with means, have been shielded from the consequences of a broken government. The economy has generally been good, and the wealthy purchase better education and health care from the private sector. …

Biden Is Planning an FDR-Size Presidency

NY mag – May 2020

… Widely seen as a cautious, tradition-bound pol and intuitive centrist within the Democratic fold, Biden stopped his economic advisers in their tracks one morning in late April. On one end of the call, the economists discussed parallels between the landscape Biden might inherit in January and the devastated one of 2009. Eleven years ago, the newly elected vice-president oversaw the implementation of historic stimulus funding, and these days Biden is fond of bringing up his Great Recession–era work because of the similar effort required today and to remind voters of this experience. But now, he said into the phone, it was time they expanded their thinking. Sure, massive gobs of federal financial help have already been approved — unlike in 2008, he pointed out — but that still won’t be enough. Not while the magnitude of this crisis dwarfs the last one. His advisers agreed: If they were going to talk about lessons from history, their future calls might as well dive into the Great Depression and World War II.

“I think it’s probably the biggest challenge in modern history, quite frankly. I think it may not dwarf but eclipse what FDR faced,” Biden told CNN’s Chris Cuomo last month. “The blinders have been taken off because of this COVID crisis,” he said to a group of 68 donors who gathered on Zoom for a fundraiser a few weeks later. “I think people are realizing, ‘My Lord, look at what is possible,’ looking at the institutional changes we can make, without us becoming a ‘socialist country’ or any of that malarkey.”

Is this news to you? Or does the vice-president seem about as far from a transformational crusader of the left as could fit in today’s Democratic Party? Even during lockdown, Biden has been doing quite a lot of interviews and making a wide range of appearances from his basement studio — in many, signaling explicitly the new ambitions now demanded of an aspiring president. It’s just that with all eyes on Trump, and Biden struggling to seize attention even as he leads in national polls, nobody has really noticed. The candidate is not blessed with historic rhetorical skills — for decades, he’s been prone to gaffes and for months has been dogged by concerns spread by his opponents that he has slipped even further. The present crisis would seem to be an enormous opportunity for a politician (like his former boss) endowed with more expansive communication chops. Instead, Biden is bunkered down, campaigning relatively quietly, and now, suddenly, answering an accusation from his past. …

“The Treasury will be significantly depleted….”

At which absurd point there is no reason to read another word.

https://www.worldometers.info/coronavirus/

August 3, 2020

Coronavirus

US

Cases ( 4,835,120)

Deaths ( 158,577)

India

Cases ( 1,855,331)

Deaths ( 38,971)

Mexico

Cases ( 439,046)

Deaths ( 47,746)

UK

Cases ( 305,623)

Deaths ( 46,210)

Germany

Cases ( 212,114)

Deaths ( 9,227)

France

Cases ( 191,295)

Deaths ( 30,294)

Canada

Cases ( 117,007)

Deaths ( 8,947)

China

Cases ( 84,428)

Deaths ( 4,634)

August 3, 2020

Coronavirus (Deaths per million)

UK ( 680)

US ( 479)

France ( 464)

Mexico ( 370)

Canada ( 237)

Germany ( 110)

India ( 28)

China ( 3)

Notice the ratios of deaths to coronavirus cases are 15.1%, 15.8% and 10.9% for the United Kingdom, France and Mexico respectfully.

August 3, 2020

Coronavirus

US

Cases ( 4,843,704)

Deaths ( 158,666)

August 3, 2020

Coronavirus

US

Cases ( 4,853,182)

Deaths ( 158,755)

Well, focusing on this official Q1 to Q2 result can be misleading. Yes, largest quarterly decline ever recorded. But it compares the average GDP of the first quarter, 5/6 of which had high income before the economy “fell off a cliff” in mid-March, with average of Q2.

But economy turned around at end of April and has been growing now for over three months. Heck, even comparing Q1 and Q2, if one looks at the end of each quarter rather than the average over each quarter, what one finds is that US GDP was about 17.6 trillioin at end of March and about 18 trillion at end of June, a 2.2% increas, which is about a 9% increase at an annualized rate. Not too shabby.

Of course growth is slowing down now and could go negative again, but not yet. That depends more on what is happening now with the pandemic, not this somewhat misleading comparison between average GDP in Q1 and average Q2, which is already an old story, things keep changing so rapidly and unexpectedly.