More on the bifurcation between the booming stock market and the bust of an economy

More on the bifurcation between the booming stock market and the bust of an economy

I wrote that new stock market highs in the face of the worst US economic downturn since the Great Depression were primarily a function of a few stocks that are particularly tied to the global economy rather than tethered to the US; that those stocks also benefited from delivering online content or physical stuff to homebound consumers; and that the background long leading indicators favor an expanding economy once the pandemic is behind us.

In addition to Paul Krugman, here are two more commentators who have weighed in on the issue, making much the same points as I did.

“[I]t’s not rare for a small group of stocks to account for a large percentage of the S&P 500. What is important is the relative performance of those 10 stocks to the other 490 stocks. The ratio fluctuates based on which group is outperforming, resulting in a continuous battle between mega cap stocks and the merely large and mid-sized stocks.

“What makes 2020 so unique is the externality of the pandemic and societal-wide lockdown. The economic impact hasn’t been evenly distributed. Large international tech companies essential to remote office work and people stuck in their houses have thrived. Add to that how much better the rest of the world has managed its response to the pandemic versus the U.S.’s bungled response. One would be hard pressed to find another era when circumstances led these two groups of companies to diverge as much as they have of late.”

Ritholtz links to an earlier piece from about a month ago:

“Yet, maybe tech isn’t all that dependent on growth in the U.S. Compared to the rest of the world, and for the first time in ages, many wealthy industrialized countries are doing better — and in some cases, much better — than the U.S. Nations such as Japan, South Korea and Germany not only have managed to contain the pandemic, but their economies are well ahead of the U.S.’s into their re-openings.“For the past five years, a small group of tech stocks has had an outsized influence on U.S. markets. Two-thirds of the gains in the S&P 500 have been driven by just six U.S. companies — Facebook, Amazon, Apple, Netflix, Google (Alphabet) — the so-called FAANG stocks — and Microsoft. An index of those six stocks is up more than 62% since the March lows, while the S&P 5001 is up about 40%:

“Overseas markets may very well be a key reason shares of the biggest U.S. tech companies are powering higher. These tech companies derive a surprisingly large share of their revenue from foreign markets. According to Standard & Poor’s, companies in the S&P 500 derived 42.9% of their sales from overseas markets in 2018 (2019 data is not yet available).

“But this share is much higher for the big tech companies: Apple generated more that 55% of its revenue outside the U.S. in the year ended in September; in some quarters, overseas accounted for as much as 60% of revenue. International accounted for 54.5% and 53.8% of Facebook and Alphabet revenues, respectively. For Microsoft and Netflix, the split is about half domestic and half overseas (49.0% and 49.4%, respectively). Amazon is the Big Tech exception, generating a sizable majority of its revenue within the U.S.

“It isn’t a coincidence that these companies that are so reliant on the rest of the globe have seen their stock prices do well. The Covid-19 numbers suggest that much of the world is way ahead of the U.S. not only in terms of managing the pandemics, and that their economies are recovering faster.”

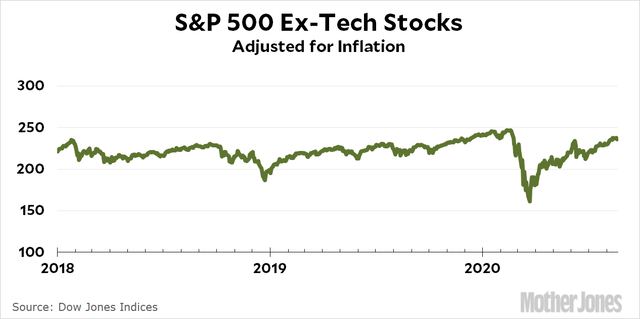

“This is an S&P 500 index with tech stocks removed and adjusted for inflation. You can see two things. First, over the past three years it’s not very impressive. Second, it plunged in March thanks to COVID-19 and has never recovered completely.

“(And that’s even though this index includes powerhouses like Amazon, Google, and Facebook, none of which are categorized as “information technology.”)

“You can always remove the top performer from a broad stock index and produce a weaker looking trend. Still, this is more dramatic than usual. This isn’t just weaker looking, it’s practically flat. The collective performance of literally everything in the United States is kind of dismal except for companies like Microsoft, Apple, and Oracle.

“So when someone asks why the stock market is doing so great even though we’re in the middle of a massive pandemic, this is part of the answer: it’s not doing so great. Aside from tech stocks, the market has been ho-hum over the past few years and is still down 4 percent from its pre-pandemic level. Investors obviously have some confidence that the economy will rebound once we approve a vaccine and the pandemic is finally sidelined—as they should—but they’re hardly being cheerleaders for the overall economy. They just like tech stocks.”

Dow kicks out Exxon, Pfizer, Raytheon in biggest shake-up since 2013

Bloomberg via @BostonGlobe – August 24

Exxon Mobil Corp, Pfizer Inc., and Raytheon Technologies Corp. were kicked out of the Dow Jones Industrial Average as part of the stock benchmark’s biggest reshuffling in seven years, actions that will boost the influence of technology companies that have dominated the 2020 stock market.

Salesforce.com, Amgen Inc. and Honeywell International will enter the 124-year old equity gauge a week from today, its overseers said. The moves were prompted when Apple Inc.’s stock split effectively reduced the sway of computer and software stocks in the price-weighted average.

While any change to the Dow is notable, the ejection of Exxon Mobil — the world’s biggest company as recently as 2011 — marks a particularly stunning fall from grace, reflecting the decline of commodity companies in the American economy. Worth $525 billion in 2007 and more than $450 billion as recently 2014, the stock had fallen in four of six years before 2020 and is down another 40% since January.

“Those changes are a sign of the times – out with energy and in with cloud,” said Chris Zaccarelli, chief investment officer for Independent Advisor Alliance.

The latest reshuffling is more testament to the ascent of technology companies, a trend amplified by this year’s Covid 19 lockdowns. While the Dow average is still 4.2% off its February record, the tech-heavy Nasdaq 100 is almost 20% above the pre-pandemic all-time high. …

Kevin Drum:

“This is an S&P 500 index with tech stocks removed and adjusted for inflation. You can see two things. First, over the past three years it’s not very impressive. Second, it plunged in March thanks to COVID-19 and has never recovered completely.”

What nonsense and how deceptive. The point being that stock market gains since 2017 have been impressive and the recovery of the market from the March decline has been impressive.

https://fred.stlouisfed.org/graph/?g=r4vw

January 15, 2018

Wilshire 5000 Total Market Index, 2017-2018

(Indexed to 2017)

https://www.nytimes.com/2020/08/20/opinion/stock-market-unemployment.html

August 20, 2020

Stocks Are Soaring. So Is Misery.

Optimism about Apple’s future profits won’t pay this month’s rent.

By Paul Krugman

On Tuesday, the S&P 500 stock index hit a record high. The next day, Apple became the first U.S. company in history to be valued at more than $2 trillion. Donald Trump is, of course, touting the stock market as proof that the economy has recovered from the coronavirus; too bad about those 173,000 dead Americans, but as he says, “It is what it is.”

But the economy probably doesn’t feel so great to the millions of workers who still haven’t gotten their jobs back and who have just seen their unemployment benefits slashed. The $600 a week supplemental benefit enacted in March has expired, and Trump’s purported replacement is basically a sick joke.

Even before the aid cutoff, the number of parents reporting that they were having trouble giving their children enough to eat was rising rapidly. That number will surely soar in the next few weeks. And we’re also about to see a huge wave of evictions, both because families are no longer getting the money they need to pay rent and because a temporary ban on evictions, like supplemental unemployment benefits, has just expired.

But how can there be such a disconnect between rising stocks and growing misery? Wall Street types, who do love their letter games, are talking about a “K-shaped recovery”: rising stock valuations and individual wealth at the top, falling incomes and deepening pain at the bottom. But that’s a description, not an explanation. What’s going on?

The first thing to note is that the real economy, as opposed to the financial markets, is still in terrible shape. The Federal Reserve Bank of New York’s weekly economic index * suggests that the economy, although off its low point a few months ago, is still more deeply depressed than it was at any point during the recession that followed the 2008 financial crisis.

And this time around, job losses are concentrated among lower-paid workers — that is, precisely those Americans without the financial resources to ride out bad times.

What about stocks? The truth is that stock prices have never been closely tied to the state of the economy. As an old economists’ joke has it, the market has predicted nine of the last five recessions.

Stocks do get hit by financial crises, like the disruptions that followed the fall of Lehman Brothers in September 2008 and the brief freeze in credit markets back in March. Otherwise, stock prices are pretty disconnected from things like jobs or even G.D.P.

And these days, the disconnect is even greater than usual.

For the recent rise in the market has been largely driven by a small number of technology giants. And the market values of these companies have very little to do with their current profits, let alone the state of the economy in general. Instead, they’re all about investor perceptions of the fairly distant future.

Take the example of Apple, with its $2 trillion valuation. Apple has a price-earnings ratio — the ratio of its market valuation to its profits — of about 33. One way to look at that number is that only around 3 percent of the value investors place on the company reflects the money they expect it to make over the course of the next year. As long as they expect Apple to be profitable years from now, they barely care what will happen to the U.S. economy over the next few quarters.

Furthermore, the profits people expect Apple to make years from now loom especially large because, after all, where else are they going to put their money? Yields on U.S. government bonds, for example, are well below the expected rate of inflation.

And Apple’s valuation is actually less extreme than the valuations of other tech giants, like Amazon or Netflix.

So big tech stocks — and the people who own them — are riding high because investors believe that they’ll do very well in the long run. The depressed economy hardly matters.

Unfortunately, ordinary Americans get very little of their income from capital gains, and can’t live on rosy projections about their future prospects. Telling your landlord not to worry about your current inability to pay rent, because you’ll surely have a great job five years from now, will get you nowhere — or, more accurately, will get you kicked out of your apartment and put on the street.

So here’s the current state of America: Unemployment is still extremely high, largely because Trump and his allies first refused to take the coronavirus seriously, then pushed for an early reopening in a nation that met none of the conditions for resuming business as usual — and even now refuse to get firmly behind basic protective strategies like widespread mask requirements.

Despite this epic failure, the unemployed were kept afloat for months by federal aid, which helped avert both humanitarian and economic catastrophe. But now the aid has been cut off, with Trump and allies as unserious about the looming economic disaster as they were about the looming epidemiological disaster.

So everything suggests that even if the pandemic subsides — which is by no means guaranteed — we’re about to see a huge surge in national misery.

Oh, and stocks are up. Why, exactly, should we care?

* https://www.newyorkfed.org/research/policy/weekly-economic-index#/interactive

https://en.wikipedia.org/wiki/SKEW

SKEW is the ticker symbol for the CBOE Skew Index, a measure of the perceived tail risk of the distribution of S&P 500 investment returns over a 30-day horizon.[1] The index values are calculated and published by the Chicago Board Options Exchange (CBOE) based on current S&P 500 options market data.

SKEW is similar to the VIX index, but instead of measuring implied volatility based on a normal distribution, it measures an implied risk of future returns realizing outlier behavior. The index model defines such an outlier as two or more standard deviations below the mean, which would characterize a black swan event or market crash.[2] The index value typically reflects trading activity of portfolio managers hedging tail risk with options, to protect portfolios from a large, sudden decline in the market.[3] A SKEW value of 100 indicates the options market perceives a low risk of outlier returns; values increasing above 100 reflect an increased perception of risk for future outlier event(s).

——

The value is now 147 which is a very high tail risk.

Skew means the index is not a well rounded bell curve. A value of 147 is a nearly useless index. In other words, I could select an index at random and do just as well.

The DOW is well managed, avoids skew. The others, especially the Wilsure, NASDEQ and Sp500 do not manage the index well.

The short answer is that investors expect ten years of Fed taxes, and they are finding ten year investments in companies who are immune to Fed taxes. These are usually the large caps.

“The DOW is well managed, avoids skew. The others, especially the Wilsure, NASDEQ and Sp500 do not manage the index well.”

I look at the Dow and SP500 every day. They invariably track one another. So if the DOW is well-managed and the SP500 isn’t, I guess that doesn’t matter.

IMO, what’s going on on Wall Street is entirely

about the Wealthy getting wealthier. Pay no attention…

However…

Trump threatens to kill Social Security if reelected

LA Times – August 10

With his four executive orders purportedly aimed at relieving Americans of the burdens of the coronavirus, President Trump spun the theme of his administration — the Art of the Con — up to a higher level.

The orders he signed Saturday include a supposed moratorium on evictions and foreclosures, a deferral of student loan payments and an extension of federal unemployment benefits.

The moratorium is unlikely to stop a single eviction or foreclosure, however. The deferral of student loan payments is short-term and narrower than what Congress put in place in May, and that has expired.

The extension of unemployment benefits reduces the federal share to $300 a week from $600, will last only four to six weeks and imposes insurmountable barriers on states to achieve even that much.

But the most potentially far-reaching order concerns the payroll tax, which funds Social Security and part of Medicare. This order, along with comments Trump made at the signing ceremony, poses a mortal threat to the 64 million Americans who currently receive Social Security benefits and the hundreds of millions more who will receive benefits in coming decades.

If he’s reelected, Trump said, he will “terminate” the payroll tax. Make no mistake: He’s talking about bankrupting Social Security.

It’s rare that a president has made such a compelling case for his own electoral defeat. Yet his campaign was so proud of this threat that it tweeted out Trump’s words within minutes.

Social Security advocates weren’t nearly so sanguine.

“This is all a very well thought-out campaign to undermine Social Security and Medicare,” Wiliam F. Arnone, chief executive of the National Academy of Social Insurance, told me. The order threatens to “erode the economic security of millions of Americans, without bringing meaningful relief for unemployed workers or employers.” …

—–

President Trump has not said he will terminate Social Security

USAToday – August 15

… One of the Aug. 8 executive orders instructed the Treasury Department to allow employers to defer payment of payroll taxes for employees who make less than $100,000 each year.

The deferrals, which may start Sept. 1 and extend through 2020, are intended to allow Americans to use the totality of their income amid the pandemic’s hardships.

The order also instructed Treasury Secretary Steven Mnuchin to “explore avenues, including legislation, to eliminate the obligation to pay the taxes deferred” — a goal Trump reiterated in remarks after he signed the order.

“If I’m victorious on November 3rd, I plan to forgive these taxes and make permanent cuts to the payroll tax,” Trump said, per the Washington Post. “I’m going to make them all permanent.”

“In other words, I’ll extend it beyond the end of the year, and terminate the tax,” he added. …

The U.S. In real terms is poorer than the Soviet Union. Paper only goes so far Anne. The market is trash much like the Federal Reserve system.

75k airline employees will lose their job over the next month. So much winning!!!!!!!

Please go through my work on Anthropological Economics. Must become one of the pillars of Economics in the 21st Century.

Sujay Rao Mandavilli

@Bert Schlitz

“…Paper only goes so far…”

[Yes, only so far for the economy, but plenty far for securities traders. Some believe in the wealth effect, but traders believe in upwards mobile money. It is the old Colossus rather than the new that inhabits Wall Street trading.]

“Give me your tired, your poor,

Your huddled masses yearning to breathe free,

The wretched refuse of your teeming shore.

Send these, the homeless, tempest-tost to me,

I lift my lamp beside the golden door!”

[…but traders just want the money.]

I’m surmising that what’s going on on Wall St

is all about the high-tech megacorps (Apple,

Microsoft, Google, Facebook, Amazon), Trump’s

tax breaks & repatriation of overseas cash,

the stay-at-home impact of Coronavirus, and

how the Wealthy (& Near-Wealthy) are reacting.

After all, the megacorps are offering products

and services that are essential to those who

are housebound & have disposable income.

it could be that the stock market is predicting a quicker recovery than anyone anticipates.

i just reviewed today’s income and outlays report, and am quite surprised how much it suggests a V shaped recovery…real PCE fell 34.1% in the second quarter, but it rose 36.6% in July….that means that even if July’s real PCE growth does not improve from the July level during August and September, growth in PCE would still add more than 25 percentage points to the growth rate of 3rd quarter GDP…

use tables 7 and 8 in the full pdf: https://www.bea.gov/data/income-saving/personal-income

comparing July’s inflation adjusted PCE of 12,778.2 billion (2012$) to the 2nd quarter’s real PCE of 11,819.6 billion, you’ll find that July’s real PCE has grown at a 36.605% annual rate from the 2nd quarter

hate to say it, but Larry Kudlow might be the stopped clock that’s right this time…

I read that the Fed is concerned these days about unemployment.

Generally, what they do seems to of more benefit to the

Wall St crowd, so maybe they are broadening

their horizons somewhat?

Fed Chair Sets Stage for Longer Periods of Lower Rates

NY Times – August 27

Jerome H. Powell said the central bank would focus its efforts on fostering a strong labor market while tolerating higher inflation.

Jerome H. Powell, the chair of the Federal Reserve, announced a major shift in how the central bank guides the economy, signaling it will make job growth pre-eminent and will not raise interest rates to guard against coming inflation just because the unemployment rate is low.

In emphasizing the importance of a strong labor market and saying the Fed will tolerate slightly faster price gains, Mr. Powell and his colleagues laid the groundwork for years of low interest rates. That could translate into long periods of cheap mortgages and business loans that foster strong demand and a solid job market. …

Mr. Powell’s announcement codifies a critical change in how the central bank tries to achieve its twin goals of maximum employment and stable inflation — one that could inform how the Fed sets monetary policy in the wake of the pandemic-induced recession.

The Fed had long raised rates as joblessness fell to avoid an economic overheating that might result in breakaway inflation — the boogeyman that has haunted monetary policy ever since price gains hit double-digit levels in the 1970s. But the Fed’s updated framework recognizes that too low inflation is now the problem, rather than too high. …

(Some recovery.)

More US jobs lost to coronavirus pandemic are disappearing permanently

… A growing number of jobs lost due to the coronavirus pandemic are disappearing forever.

A new analysis of payroll data published by Gusto found that less than half of furloughed employees have returned to work since March, and often for less money than they were earning pre-crisis.

The findings show that only 37% of workers furloughed in March, and 47% of those laid off in April, returned to their jobs as of July. A quarter of the workers furloughed in March who were re-hired and went back to their jobs had their wages slashed by 10% or more.

Just 14% of workers who returned to work are earning the same amount of money that they were previously making.

Of the millions of workers furloughed between March, when the COVID-19 outbreak triggered an unprecedented shutdown of the nation’s economy, and June, 22% have been permanently laid-off.

The Labor Department’s July jobs report released at the beginning of August showed that employers added 1.8 million jobs last month, sending the unemployment rate down to 10.2%.

While it marked the third consecutive month of job growth in the millions, the economy has so far added back less than half — about 42% — of the 22 million jobs it lost during the pandemic. Permanent losses reached 2.9 million in July, the report showed. …