Ripping Off College Students’ Economic Future Redux

Originally, I put this into print November 2013. I took from many sources to complete it. I think it meshes well and still stands the test of time. The student loan issues and debt are still in existence. The debt owed is fare larger now with much of it being accumulated interest on principle. The cause of much of this is largely due to Biden’s policies before he became President up though 2005. The numbers for those having student loans is far greater as is the debt also.

Previously, I had written on Fair Market Value and its use by the CBO’s Douglas Elmendorf to rate the risk of Student Loans as advocated by both The New America Foundation and the Heritage Foundation. A rebuttal answer to a partisan CBO, the right-leaning New America Foundation, and the conservative Heritage Foundation on the usage of Fair Market Valuation methodology in the same manner as what I would have used it for to rate the return on a piece of capital equipment is simple.

Fair Market Valuation is still inappropriate for student Loans. There is little or no risk to loaning students money which can not be discharged through bankruptcy. The news media has been pandering to students promoting a generational war by advocating the theft of student’s futures by such programs as Social Security, Medicare, Medicaid, etc. The real issue being student loans for millions of them. Alleviate the loans and there is a wealth of funds to be for homes, families, and retirement.

Social Security and Medicare can be fixed rather easily through various fixes and still maintain them as the third rail. Medicaid can be fixed also. I will get into that at a later time. I have a blog to run here and I am shy writers. We welcome people who can write.

The Tom Friedmans, James Freemans, and others suggest baby boomers are ripping-off the X, Y, and Z generations with these programs. From the well-heeled segment and do not have to work anymore 1-percenter population, we find Stan Druckenmiller, Pete Peterson, the Koch brothers, etc. spending portions of their $billions advocating the discontinuance of Social Security to save the country, students, and themselves. Some are taking to college campuses with false data and advising students to protest the rip-off of their futures in a Days of Rage manner. All tend to ignore the real threat to students and their future. The threat is not likely to come from Social Security, Medicare, etc.

What is threatening the future wealth and income of college students is the increasing debt taken on by students seeking the education necessary to have a chance in a global economy where investments are seeking fewer Labor-intensive opportunities. The increased funding necessary to go to college is the result of decreased governmental funding of schools, declining or stagnant household incomes, financial strategies delineating the increased risk of student loans (CBO, The New America Foundation, Heritage Foundation, etc.), and the increased cost of attending colleges and universities (which as Alan Collinge of Student Loan Justice Org. states cost increases have outstripped CPI and even Healthcare).

Student Debt has quadrupled from 2003 to 2013 going from ~$240 billion to > $1,000,000,000. Up from 41% in 1989, 66% of all students now have an average debt of ~$27,000. The rise in average student debt is due to a sharp decline in state funding (25%) of public colleges since 2000. And a stagnation and decline of household income for the vast majority of US households over a similar time span.

As Dr. Elizabeth Warren pointed out in “The Coming Collapse of the Middle Class” where a high school diploma and a sound work ethic were once the ticket to into the middle class, the college education and two incomes are now the surest way into the middle class. Even so, evidence of the high cost of a college education and the resulting debt from a college education has begun to extract its toll on the financial futures of graduates, especially minority and low-income students. For most young adults chasing a college education requires taking on student debt.

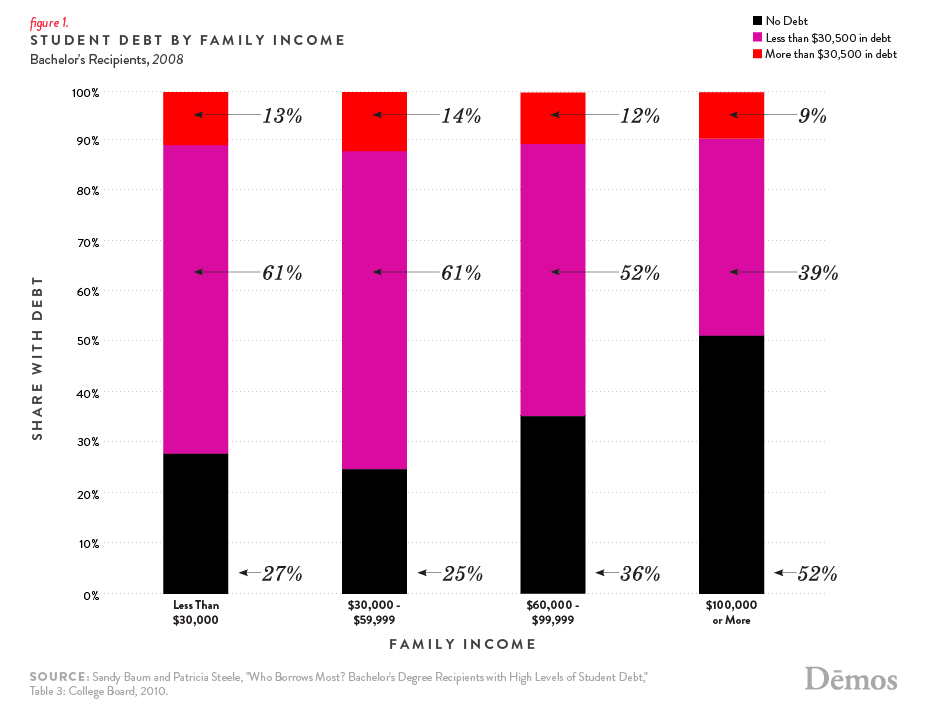

Reflected in an August 2013 study by Demos “At What Cost;” the amount of debt carried by student has not only increased, it also varies by amount of family income. 75% of all BA graduates coming from families with incomes < $60,000 have varying degrees of debt as compared to 48% of those coming from families with incomes >$100,000. 14% of all low-income students leave with loan debt > $30,000 as compared to 9% of students coming from higher income families.

80% of all African Americans graduates leave college with loan debt as compared to 65-67% of White and Latino students and 54% of Asian students. African Americans carry a higher level of debt as compared to students of other races.

The average debt load ranges from $20,200 – Public Schools to $33,000 – For Profit Schools with Private Non-Profit Schools at ~$28,000. The debt load resulting from For Profit Schools is 64% higher than at Public Schools.

Some at the Brookings Institute and The New America Foundation would argue interest rates do not matter as the incremental increase only accounts for a few more dollars monthly. Interest rates do matter over the long term as they extend the length of the loan over the 10 years or “more” needed to pay them off.

Brookings’ Matt Chingos dismisses first term Senator Warren’s idea of student loan interest rates being the same as what the FED Loan Rates to banks such as Goldman Sachs as being a cheap political trick. Senator Warren’s proposal does have merit and its only fault being it comes when the Fed is thinking of loosening Fed Policy. Perhaps, if Senator Warren was in office in 2008 the proposal to use Fed Rates for Student Loans would have come sooner. But then, maybe the crash would not have happened too? In any case, we would have been graduating one group of students with more manageable and less costly loans.

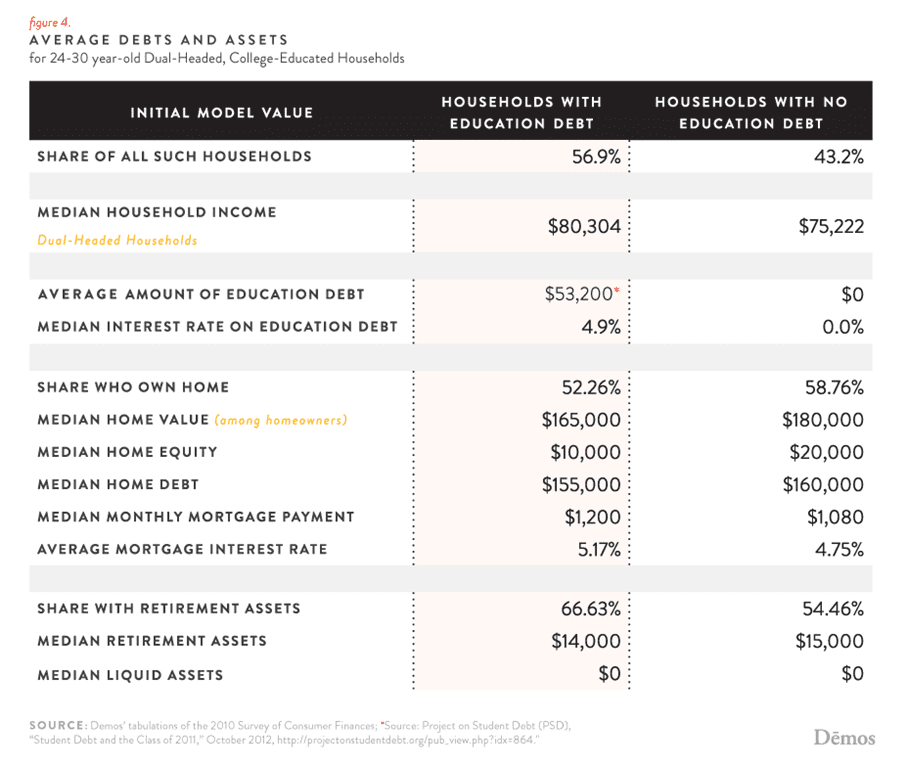

Young college educated students without student loan debt accumulate more retirement funds sooner, purchase homes sooner (more expensive homes), put down larger down payments, and paid lower interest rates.

“Households with education debt have higher average incomes than those without. This is consistent with other research on the incomes of young college-educated households.”.

Much of that difference comes from the preponderance on getting a higher salary to offset the loan. The next chart suggests the increased salary is more than offset by increased wealth of those without debt.

As I have pointed-out to some proponents of higher interest (went unanswered), higher interest rates do make a difference in the long run of 10 years or more. The month-to-month marginal cost of a loan is not the issue. The issue is the total cost of the loan over its lifetime.

For example, a loan or ~$26,600 to one student over 4 years would cost a student ~$32,000 over an 11 year period if the economy remained good. There is the chance of at least 1 recession if not two which would lengthen the loan repayment period. Elmendorf, Delisle, and Richwine are quick to point out the costs to the government and taxpayers of making lower interest rate student loans.

Druckenmiller is pushing the false argument the fully funded Social Security and funded Medicare programs are ripping off college students and their futures. All seem to miss the point the riskier assessment achieved through Fair Market Valuation of Student loans will result in higher interest rates costing students impacting theiir wealth and income over the decades.

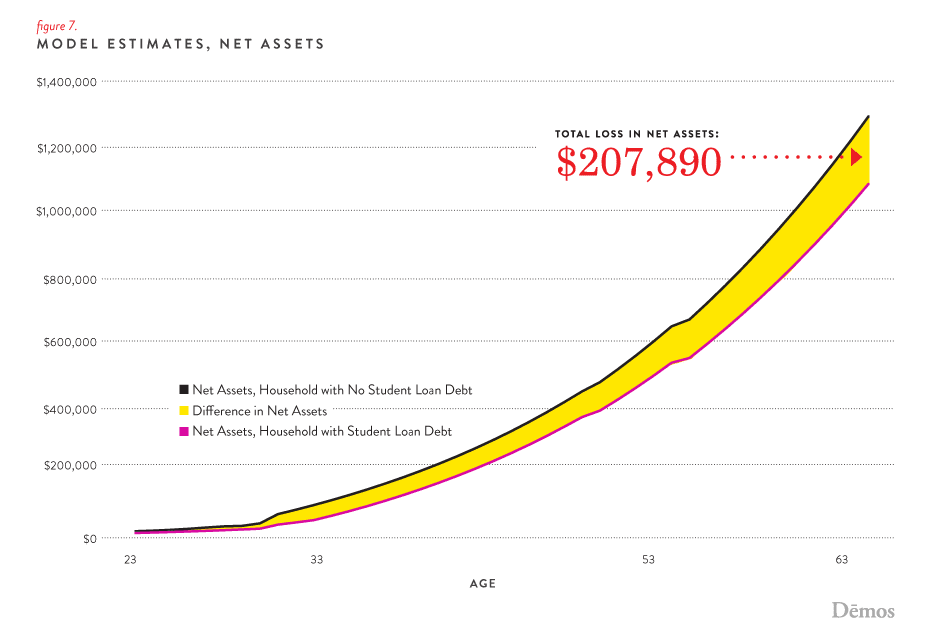

Burdened with student debt, a student can expect to lose lifetime wealth of ~$208,000 when compared to unburdened students. “’Nearly two-thirds of this loss comes from the lower retirement savings of the indebted household, while more than one-third ($70,000) comes from lower accumulated home equity; because of the two withdrawals from savings later in their lives, the liquid savings gap is just $4,000.’ In general, ‘it can be predicted a $1 trillion in outstanding student loan debt will lead to total lifetime wealth loss of $4 trillion for indebted households.’”

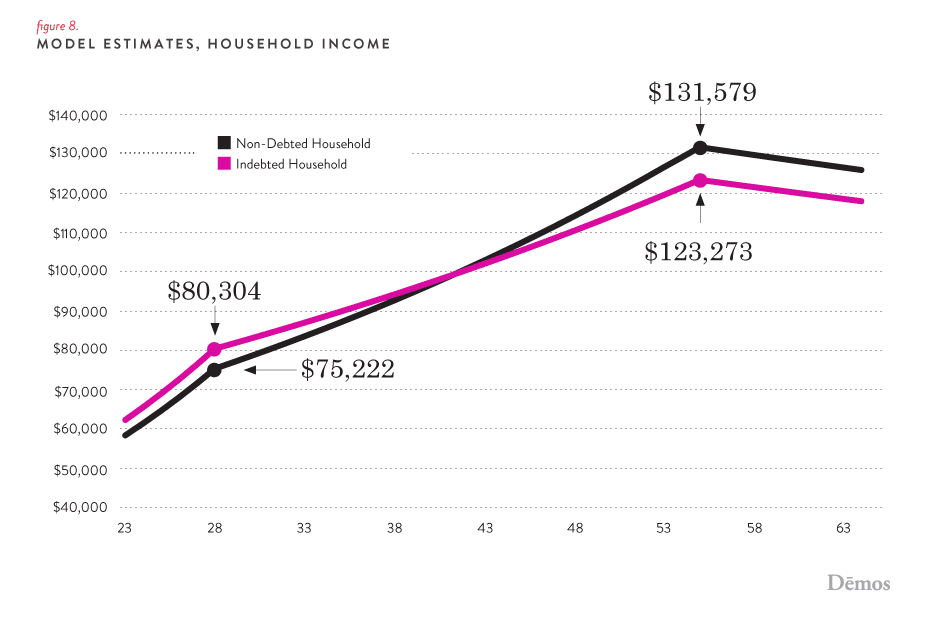

Besides an impact to accumulated wealth, there is also a difference in income as well. From 40 years of age onward the difference in income peaks at ~$8,000 annually. It continues until retirement between those carrying student debt and those without. In a demand led economy, the difference in incomes would impact purchasing power. ~57% of all households between the ages of 24 and 30 have some type of Student Loan Debt.

Are students being ripped off by government entitlement programs? Yes, they are being ripped off. It is not by Social Security or Medicare as Stanley Druckenmiller suggests. Nor are student loans costing the federal government and tax payers as much as the recent analysis of student loans done by the CBO’s Douglas Elmendorf. In reality, the risk to the government and taxpayers comes from these students being less successful in accumulating wealth and increasing income which as DEMOS has suggested would cost $4 trillion is wealth alone. Unburdening students from a lifetime of student loan debt would benefit the economy.

References:

Fair-Value Estimates of the Cost of Federal Credit Programs in 2013; Douglas Elmendorf

Fair-Value Accounting Shows Switch to Guaranteed Student Loans Costs $102 Billion; Jason Delisle

Sorry Kids, We Ate It all; Tom Friedman

Stanley Druckenmiller; How Washington Really Redistributes Income; James Freeman

Geoffrey Canada ’74 and Stanley Druckenmiller ’75: Generational Theft Stanley Druckenmiller;

Student Loan Justice Organization; Alan Collinge

The Coming Collapse of The Middle Class; Dr. Elizabeth Warren; http://www.soyouthinkyoucaninvest.com/2009/04/elizabeth-warren-coming-collapse-of.html

At What Cost; How Student Debt Reduces Lifetime Wealth; Demos, Robert Hilton Smith

Do Student Loan Interest Rates Matter?; Beth Akers

Ripping Off College Students’ Economic Future, Angry Bear

Oh what a bunch of utter nonsense. Colleges and universities should be the ones providing the loans. That would solve all the problems, because the lunacy of $100,000 per year of liberal arts and gender studies would never be funded by the academic institutions. They always want someone else to fund these left-wing utterly useless degrees. Meanwhile they pontificate from their tenured palaces about this and that and everything else.

Higher education needs to be torn down and rebuilt. Just like the disfunctional federal government.

well joe, if you say so . . .

Joe, what do you suggest? You babble on the problems and offer no solution.

“College graduates are half as likely to be unemployed as their peers who only have a high school degree. Typical earnings for bachelor’s degree holders are $36,000 or 84 percent higher than those whose highest degree is a high school diploma. College graduates on average make $1.2 million more over their lifetime.

How does a college degree improve graduates’ employment and earnings potential?

“The 2022 NACUBO Tuition Discounting Study . . . found that the majority of private colleges and universities clear the 50% mark in their tuition discount rates.

“The survey of 341 private nonprofit institutions found a 56.2% average institutional tuition discount rate in the 2022-23 academic year for first-time, full-time, first-year students and a 50.9% discount rate for all undergraduates — the highest rates recorded.”

Average Tuition Discounting Rates at Private Institutions Hit New Record High, NACUBO Report Finds

“Before adjusting for inflation, average 2023-24 published tuition and fees for full-time college students increased:

· 2.5% at public four-year colleges (in-state students): $11,260, $270 higher than in 2022-23.

· 3.0% at public four-year colleges (out-of-state students): $29,150, $850 higher than in 2022-23.

· 2.6% at public two-year colleges (in-district): $3,990, $100 higher than in 2022-23.

· 4.0% at private nonprofit four-year colleges: $41,540, $1,600 higher than in 2022-23.

“Taking a longer view, over the decade between 2013-14 and 2023-24, average inflation-adjusted tuition and fees declined by 6% at public two-year colleges and 4% at public four-year institutions. Across that same period, they increased by 5% at private nonprofit four-year institutions.”

https://www.forbes.com/sites/michaeltnietzel/2023/11/02/average-college-tuition-increased-less-than-inflation-for-2023-24/?sh=63260842496f

The problem with student loans isn’t the majors that students take in college. There are two major problems with student loans:

1. Just like with any debt, some people make bad decisions and get in over their heads. This happens with auto loans, home loans, business loans and credit card debt, it’s not unique to student loans;

2. Unlike other debt, though, student loans can’t be discharged through bankruptcy.

The laws on student loans should be changed to allow student loans to be discharged through bankruptcy, just like other debt. That would put the risk where it belongs, on the lender.

Keep in mind that student loans are fundamentally unsecured and mostly needed by people with little or no credit history. As long as our society is willing to live with the resulting credit market, sure let lenders lend against their credit risk standards and take their chances.

@Eric,

Not sure why the present system is superior. Why not have a system of national needs-based scholarships?

Eric:

Ninety-two percent of student loans are owned by the Gov. What is the risk? They are safer than Wall Street Investments. Student Loan Debt Statistics: 2024 – NerdWallet

There is even a market for these called SLABS

“With a global economy in which liquidity is increasingly important, securitization—the repackaging of assets into marketable financial instruments—has slithered into every market. While this affects the mortgage, credit, and auto loan markets, a less widely known space transformed by securitization is the student loan market. But just how safe is this market for investors?”

• Student loans make up more than $1.6 trillion in outstanding debt in the United States from over 43 million borrowers.1

• Packages of student loans are being marketed as asset-backed securities known as SLABS.

• SLABS have enticed investors due to some structural guarantees—some worry that these instruments may adversely affect the economy.

• There would need to be significantly more factors in play for student loan debt to have the same impact on financial markets as the Great Financial Crisis.

That is about two years of Defense spending. Potentially, the education of people has a return called “increased productivity.” And there are bad actors in the field of education.

SLABS implies risk to each layer. Investors are taking bets on their Slab paying off. Just think of its as a CDO.

I graduated from college in California in 1981 with a college debt of 2 grand. I lived in Hermosa Beach and Venice California during my college years and got through college as a waiter. Interest rates were very high back then but my BEOG rate was low, really low. My payments were 30 bucks a month.