No, Medicare is not running out of money

There are issues with Medicare which are easily fixed.

Maggie Mahar was writing on healthcare at Angry Bear. I did the editing. I picked up on the issues with her on healthcare and have portrayed writers such as Merrill, Kip Sullivan, Charles Gaba, Steve Early, Susan Gordon, Andrew Sprung, etc.

There are issues with healthcare such as cost. Then there are make believe issues such as Medicare being in trouble. The same is true of Social Security. A few tweaks here and there and the problems go away for 75 years.

Read on with Merrill Gooz.

~~~~~~~~

Calls for radical transformation of the program ignore the trust fund’s history, and how much it rapidly responds to policy and the economic changes.

Fellow healthcare writer Merrill Goozner at Gooznews . . .

The House Republican Study Committee last week unveiled its latest plan to cut Social Security and Medicare. Even some rightwing conservatives are tearing their hair out.

“What a terrible idea,” Sen. Josh Hawley (R-MO) told reporters on Capitol Hill. “If Republicans want to be in the minority party forever, then go ahead and endorse that.”

He was only referring to the plan’s call to postpone the retirement age to 67, which would force working class people to work more years at more physically taxing jobs before receiving benefits from a program they paid into for their entire working lives. People in the bottom half of the income distribution are much more dependent on Social Security for their retirement income than wealthier people.

Democrats, including President Biden, immediately pounced on the idea of cutting retirement programs, which was endorsed by at least 160 House Republicans. Biden . . .

“Not on my watch.”

One way to describe the soon-to-be-coronated Republican standard bearer’s position on the issue is that he consistently supports both sides. Here’s how Perplexity.ai described his position (I prefer it to ChatGPT as an artificial intelligence search engine because it gives sources for its responses, which allows the user to doublecheck and evaluate their quality ):

“Trump’s stance on this issue has been inconsistent, with his administration proposing budget cuts to Social Security and Medicare programs but also emphasizing protection for these programs during his campaign rallies.”

Its cited sources were CNN, NBC and The Hill, an inside-the-Beltway publication.

Blame the trust fund

Since I focus mostly on health care, let’s start with the Republican Party’s rationale for cutting Medicare.

The plan’s lead-in to its first paragraph on the issue said it all: “Looming insolvency” (bold face in the original). “The Republican Study Committee Budget would help save this critical program and protect seniors from the devastating 11 percent across-the-board cuts resulting from the Hospital Trust Funds insolvency in 2031.”

I first heard reference to the looming insolvency of the Medicare trust fund in the early 1980s. During the steep recession of the early Reagan years, the accumulated surpluses in the trust fund actually did face exhaustion. Increases in the payroll tax in 1983 and 1986 (signed into law by president Reagan) eliminated the threat.

This threat has been resuscitated nearly every election year since, thanks in part to the constant harping by the deficit hawks at the Committee for a Responsible Federal Budget, whose board includes a long list of retired conservative politicians and government officials (mostly Republican but a few Democrats).

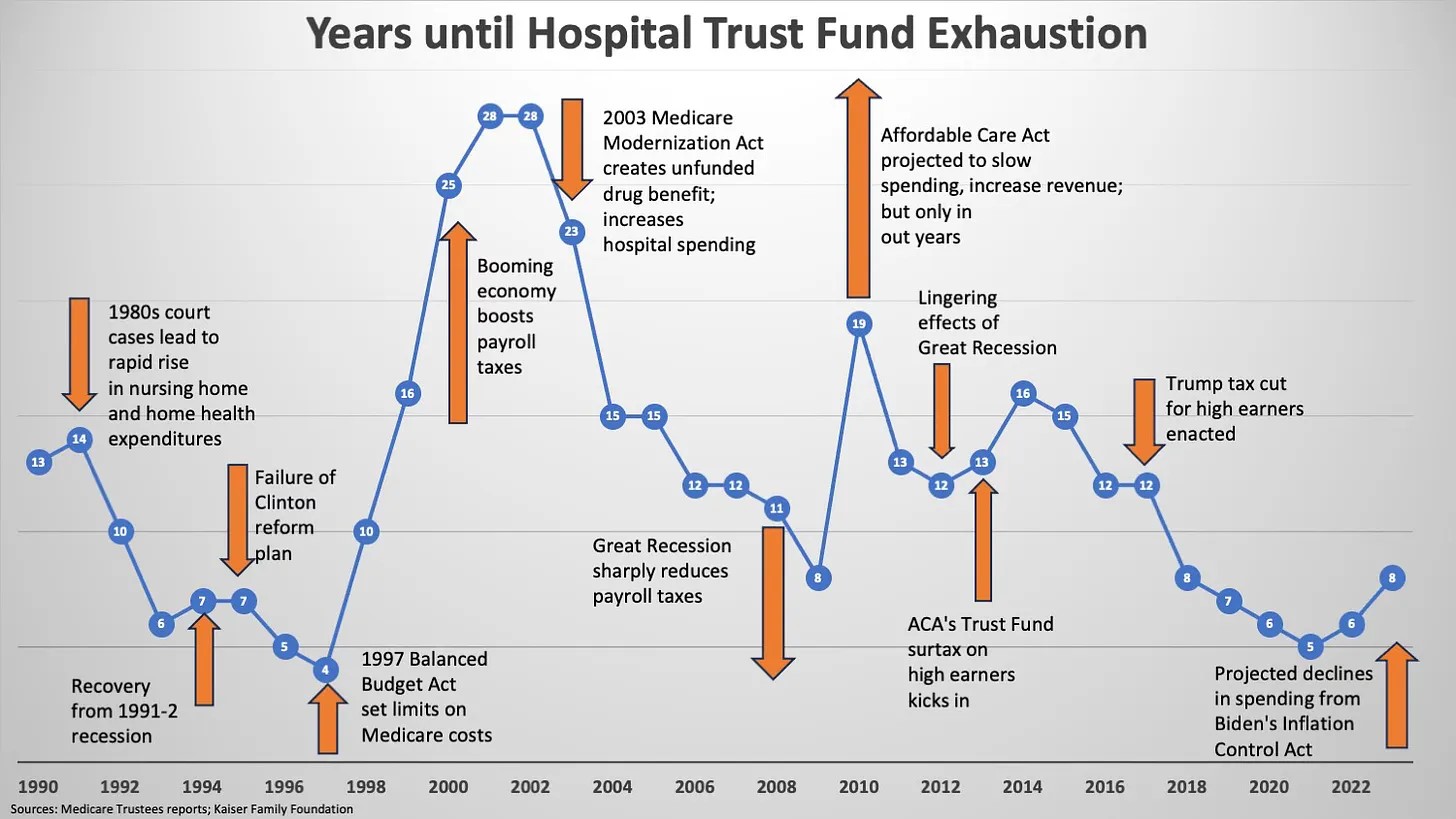

But is the threat real? Le’s review the history of the Medicare trust’s fund “exhaustion date” — now projected for 2031 in the most recent Trustees report. A new report is due by the close of business on March 31 — less than a week away.

What we see from the below chart is that the trust fund’s exhaustion date has swung wildly over the past 30-plus years, ranging from a high of 28 years in the future to as low as four years in the future. When one delves into the reasons offered each year by the trustees, one finds that that hospital trust fund solvency in highly responsive to changes in policy and changes in the economy.

A constantly moving goal post

It’s easy to understand how changes in the economy effect trust fund solvency. When the economy is growing and unemployment is low, tax collections — the Medicare hospital trust fund relies on the 2.9 percent payroll tax, half paid by workers and half paid by their employers — are high. The trust fund’s exhaustion date gets pushed farther into the future. During recessions, the opposite occurs.

But the trust fund’s solvency and projected exhaustion dates are also responsive to policy changes that affect how government dollars for health care are spent. The 1997 Balanced Budget Act signed by President Clinton slapped limits on hospital and physician reimbursement rates, which set the stage for a major extension of program solvency. The unfunded Medicare Modernization Act of 2003 that established the drug benefit, enacted under President George W. Bush to ensure his reelection, reversed that momentum.

Similarly, the Trump administration’s tax cuts for corporations and wealthy individuals in 2017 reversed the effects of the higher payroll tax collections that had been included in President Obama’s 2010 Affordable Care Act. The Biden administration’s Inflation Control Act, which included for the first time limits on some drug prices including some used in hospitals, pushed the exhaustion date farther into the future.

Indeed, if one wants to draw a general rule from the above chart, the solvency of the Medicare trust fund improves under Democrats and worsens under Republicans. The exception in recent decades was the first term of the Clinton administration, when his health care reform plan failed and Republicans led by Newt Gingrich won control of both houses of Congress.

What’s the plan?

The latest not-so-new plan from the House Republicans would turn Medicare into a voucher program, which they refer to as premium support. They plan to combine program’s hospital, physician and drug benefits (Parts A, B, and D, respectively) into a single plan, which would be offered by private insurance companies. Seniors would receive a legislatively determined level of support to purchase plans. The rest would have to come out of pocket.

The level of support could be set either as a dollar amount or as a percentage of the traditional Medicare plan, which would still be available to seniors. One way to describe it is “Medicare Advantage for All.”

That could turn out to be a disaster for the millions of seniors, a majority of whom are anxious to save money through reducing their upfront out-of-pocket health care costs. Wealthier seniors who remain in traditional Medicare would be able to buy supplemental plans as many do now. The less wealthy will continue to flock to MA plans for their lower up-front premiums.

But they could wind up being hit with huge out-of-pocket expenses when they become seriously ill. The size of those payments would depend on the level of premium support offered by the Republican Congress that enacted the plan. The lower the level of support, the higher the out-of-pocket expenses.

Do you trust the Republicans to set a generous level of support? If so, someone who owns Truth Social has some stock he’d like to sell you.

What about Social Security?

Last year, the trustees of the Social Security trust fund projected it will run out of money in 2034. That date has bounced around, but has been set somewhere between 2030 and 2040 for most of the past four decades. That’s because the demographics of the country — how many old people will be collecting benefits in future years — are easily calculated. The precise date is largely dependent on the state of the economy — how many people are working and paying the flat payroll tax.

And that’s why there’s an easy fix for the projected shortfall (which, if unaddressed, could reduce benefits by about 23% in 2034). All you have to do is apply the payroll tax, which is currently capped for people earning over $168,600 a year, to all income.

The growth in income inequality has made Social Security’s finances more precarious. As people in the highest income brackets took home a larger slice of the total income pie, less of the nation’s total income was taxed to provide retirement benefits for the elderly.

In 1977, Congress set the share of national income that should come under the Social Security payroll tax at 90 percent. Today, only 83 percent of national income is taxed, a reflection of a greater share of national income going to those in the highest brackets.

Eliminating the cap would end the trust fund’s gap for the foreseeable future. Even if we apply the tax only to those earning over $400,000 a year would stabilize long-term financing for the program, according to legislation introduced by Sen. Sheldon Whitehouse (D-Rhode Island).

Okay, now I’m confused a bit. You quote Sen. Hawley about delaying the retirement age to 67 and the further discussion of this in the paragraph concerns Social Security. But SS full retirement age is almost 67 now and will be 67 for anyone born after 1961. Are you sure he wasn’t talking about Medicare? That makes more sense since that age is a flat 65.

(The numbers are footnotes.)

As far as I can tell, the The Republican Study Committee Budget(pdf) does not actually say what they would do with the age.

They blame Biden for an issue which we have been discussing (including providing a solution) on Angry Bear for nearly 20 years and assert that it will be solved by bipartisan negotiation.

Arne:

I made the 1 tenth of 1% point on another site. All they can not get through their heads, the Altman solution which is tax the rich. Ok, tax the rich but use the funds to supplement income, provide healthcare, and more liberal quantities of food. As Dale argues 1 tenth of one percent is a dollar a week on $50,000 and people maintain control of SS. The same people the rich look down upon.

As far as Biden? Everyone knows he is old and senility has taken over.

@Bill,

I devoutly hope to be as “senile” as Biden is when I get to be his age.

Joel:

When you are overwhelmed with detail and pressure, your cognitive abilities may slip a bit. He delivered an excellent economy. Hope he continues.

Eric

someone misspoke. they want to raise it to seventy or something like that, or this article must have been written before 1983.

moreover “hard physical labor” is not the issue. living longer does not mean you will be able to work longer. and even if your physical health holds out, your mental health may not. being able to retire was once a luxury of the rich. FDR made it possible for the poor. That’sone reason why “we paid for it ourselves” is so important” and why scrapping the cap is a stupid idea. Oh, did I say “stupid” again? Well, stupid me, but it IS a stupid idea.

if you pay for it youself, there is no reason anyone should be able to tell you when you can retire.

Headlined this ~ pretty typical, Arne, Republicans not actually saying what they would do

They’re playing with fire, and I encourage them to …

Ten

they wo’t burn themselves. they will burn the house down.

Rube Goldberg strikes again

raise the cap to fund social security by turning it into welfare as we knew it….and it will not “end the problem,” at least no analysis i have seen shows raising the cap to actually solve the actuarial deficit caused by retirees living longer..but not able to work longer. old age, you know. it has nothing to do with arduous physical labor. it has everything to do with people’s desire to do something with the rest of their lives beside make money for the boss…and if they pay for it themselves, who should stop them?

…when you CAN fix SS forever by raising the payroll tax one tenth of one percent per year for workers and employers. thats about a dollar per week per year in today’s money…while real wages are expected to go up ten dollars per week per year.

we won’t “solve” SS as long as politicians are criminals and people are stupid.

Medicare is not my field, but the argument has long been that medical prices are too high in america.

even so, 2.9% of your income is not a lot to pay for health care when you are old…how much does private insurance cost today? or private insurance subsidized by government…paid for by taxpayers but not in a program with a “trust fund”?

if the “friends of Social Security and Medicare” would just get real we might actually fix the problems but we’d have to make congresspeople an offer they could not refuse.

There are topline numbers in the appendix.

SS Outlays ($B)

2025 -73

2026 -82

2027 -92

2028 -117

2029 -143

2030 -161

2031 -180

2032 -195

2033 -218

2034 -252

Still no indication of where the reductions in outlay come from. Since all politicians say no impact on near retirees, the numbers are not really consistent with a “simple” increase of the Full Retirement Age, so trying to infer a specific proposal is unwarranted. If the 1983 changes were used as precedent (in terms of giving advance notice), any “benefit” from increasing the FRA would not show up for a decade.

After reading it again, I suspect that the writer “explaining” Sen. Hawley simply was wrong about what Hawley was objecting to and that – probably – there is an element of age increase beyond 67 being contemplated.

Also interesting was the idea that the program was scoped in 1977 to capture 90% of payroll income and that’s down to 83%. But if the “missing” 7% has gone above the cap, shouldn’t the 83% still yield just about the same revenues anyway? Feels like the “missing” revenue has more to do with the distributions below the cap. Now that doesn’t mean that raising the cap won’t pick up revenues, just those high incomes are not the direct problem….it’s millions of wages below the cap that maybe people expected to be (wild guess) $15,000 higher by now. If that’s the big “problem”, how comfortable should we feel when Dale tells us that a few bucks now is unimportant because everyone will be swimming in pools of dollars a la McDuck in a few decades? Isn’t a significant part of this that whatever was modeled in 1977 was higher than what actually happened? Also, since 90/83 = 1.084, why would benefits drop by 23% instead of more like 8.4% when the Trust Fund is fully redeemed? So raise the cap to hit the 90% target, but looks like you still have about 63% of the gap left to cover. I’m a beneficiary and am fully aware that beneficiaries’ ability to react is much lower than a 36 year-old will usually have, but I don’t think that means my contribution to correcting this situation has to be zero. I paid for decades, but it’s actuarially the case that I didn’t pay enough.

Eric

you almost had me thinking you were making sense. i never said we’d be rich. i said wages were expected to go up one full percent per year while the tax need go up only one tenth of one percent.

your 90/83 calculation seems to leave out that the people in the top 7 % are making a lot more money than the average worker. but i agree raising the cap to capture that extra 7% of earners is not smart…those people at the top think they earned their higher wage and they won’t want to spend it on someone else’s retirement. [i am being lazy here…i’d have to stop and do some math to see what the real answer is, but note that raising the TAX 2% for workers and employers =4% of wages but =33% of SS taxes/then consider that 25% of benefits is NOT 25% of working wages, but 25% of benefit which are less than 50% of working wages.

if you are going to think, you must think about the whole problem, not just dicker around with whatever strikes your imagination and then shout eureka when you get an answer you like.

making sense, not making since…

but you can see why working into deep old age may not work out even if you are going to live longer and the work is not physically arduous.

fixed . . .

thanks Bill. now everyone will wonder what the hell i wa talking about. not that that is any different. i often wonder myself.

Aren’t we all waiting for Trump to regain office and right away institute his Long Awaited Really Great Improved Medicare, which will no doubt bear his name. Or perhaps just remove funding from the old, creaky one first, institute the new one once they’ve worked out who’s going to pay for it & how much. That way there’ll be added pressure to get it done.

Fred

we might as well be.