On JOLTS, I continue to dissent

On JOLTS, I continue to dissent

The only two significant items of data in the second week of the month typically had been the JOLTS report and the Labor Market Conditions Index.

I say, “had been” because the Fed has discontinued reporting the LMCI. Here’s their explanation:

Although the LMCI was reconstructed back 50 years, it was only published in real time for the last few. I am disappointed. Even if the Fed believes the LMCI was not giving them the accurate information they were looking for, I wish they had at least continued to publish it in real time for one full economic cycle, because it may have given other valuable information — e.g., being a valid long leading indicator for the economy as a whole — that wasn’t on their radar.

Turning to JOLTS, I have been a dissenter about this data series for the last year. The typical commentator has focused on job openings, which have been trending higher strongly (as they did in today’s report for June):

Thus even Bill McBride calls today “another strong report.”

But openings are the one aspect of the report that are not “nard” data. They can just as easily be skewed by employers trolling for resumes, perhaps laying the groundwork for visas for cheap immigrant labor, or simply refusing to offer the wage or salary that would call forth enough actual applicants to hire. Hence the disconnect between “openings” and “hires.”

Rather, I prefer to focus on the “hard” data series such as hires, quits, and layoffs. And here, the story hasn’t been nearly so strong.

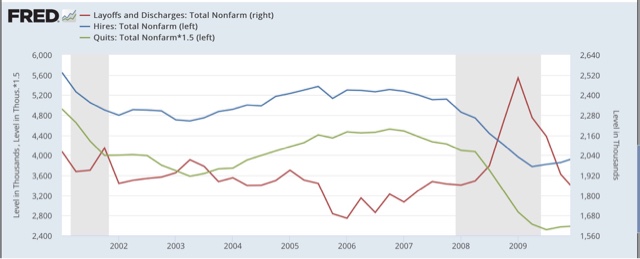

Let me start by comparing hires to total separations (averaged quarterly to cut down on noise):

We only have one full business cycle to compare, but since the outset of the series at the start of the Millennium, the trend has been for hires to slightly lead separations. And hires have been stagnant for going on 2 years.

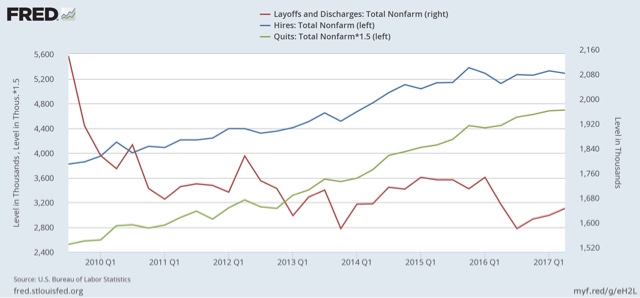

Let’s compare hires with voluntary quits and also layoffs and discharges. Here we see that in the last cycle, hires stagnated, and shortly thereafter involuntary separations began to rise, even as quits continued to rise for a short period of time as well:

And here is the current cycle:

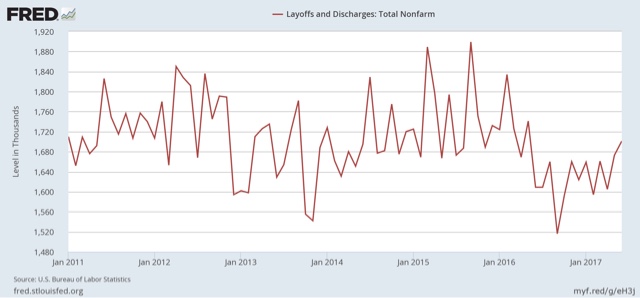

Once again, hires have stagnated. Perhaps even more significantly, even while quits have continued to rise, involuntary separations bottomed a year ago, and have risen on a quarterly basis ever since. In fact, on a monthly basis June’s level of layoffs was the highest in over a year:

Although FRED can’t show it, the three month rolling average of layoffs is also at a 12 month high.

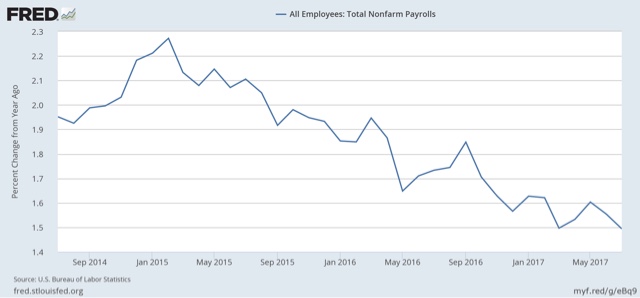

In short, despite the strong payrolls numbers of the last few months, JOLTS shows an employment situation that has been slowly decaying. And by the way, the same thing is shown in the YoY change in payrolls:

So I continue to dissent. I do not believe the JOLTS reports show strength, but rather have gradually trended weaker, even if they do not portend any imminent economic downturn.

Looks plenty strong to me. It also shows the jobs skill gap higher wages cannot solve.

Rising lay-offs most definitely do not show that there is a job skills gap that higher wages cannot solve.

First comments go to moderation. Welcome to AB.

I agree the hard data is what counts… “openings” are highly misleading.

But what is more relevant are the ratio’s of hires to quits and quits to layoffs in time series — probably as a running n period average.

Of course getting the ratio’s requires downloads of the FRED data and then roll your own calcs, followed by charting the results rather than just using FRED charts… far more time consuming.

But you can also automate the downloads “on demand” or by time intervals, with standard automated calcs, and automate thel your own charts if you go to the trouble.

You can do calculations in Fred, so you can plot ratios there. Edit the graph. Add a series. Then type in a formula relating the two series as ‘a’ and ‘b’, e.g. ‘a/b’.

https://fred.stlouisfed.org/graph/?g=eK0a

Job growth has rocketed during the end of 2016 and into 2017, especially earlier in the year which has led to a across the board drop in unemployment. It also gave the illusion of softening wage growth because of all the new entries into the labor force during that runup without offsetting raises. Of course now those workers are getting the raises which drove up wages in July and probably will be firmer year over year compared to last year due to lower unemployment. Here is the key. If we go through another surge in 17-18 like we had late last year, is there enough “slack” left keep wages steady. My guess, there is not. LFPR is at the same level as the Carter peak in 79 and I would argue the labor market is even tighter now than was then(which featured embedded inflation and huge losses in real wages due to BW’s collapse).

I see way to much “trying to tell my biased story” rather than what is really going on. This expansion has been pretty steady with its surges and ebbs. There are only so many surges it can take and frankly, based on unemployment and how past cohort levels reacted to how the current labor market reacted, I think the U-6 going down to 7.6% by next year will simply be to much. 8-8.2% is probably the slashing the throat line for employers.

Karlberg is correct. Ratio’s and other formula’s can be used to relate one series to another as well as modify the y-axis units with the result charted on a a single FRED chart. I use this method occasionally as well if and when I’m sure of what it is I want to understand with the data. Otherwise I find downloading the data and doing my own exploratory analysis is faster and more direct.

I don’t know how this the use of multiple series FRED chart formula’s can be automated though and it can’t be used for rolling time series n unit means of one or multiple relationships. I find rolling average of n unit time series to be highly informative (seeing forest through the trees or getting the signal from the noise)- especially to identify clear trends to differentiate the outliers or extremes from the normal excursions..

Bert,

Pay close attention to where the job growth is and has been. I find too much of it (proportionately) is in the lowest wage sectors which is a response to employment growth in the higher wage and salary brackets.

The lowest wage sectors require little (no?) education and training is fast and cheap so the supply for labor in those sectors is much larger … and thus little and even no labor supply constraint. In effect that labor supply source is spare supply, drawn on as needed without much wage pressure to increase hiring.

Those sectors are the first to fire and lay-off, and go to part-time employment as the higher wage & salary sectors of employment stop or reduce hiring or even start cutting back.

For those reasons I don’t think you can relate Carter era 1979 LFPR to the present times — mostly because the middle class medium income wages and salaries were proportionately a greater proportion of employment than in recent years. Much of that middle class sector has disappeared .. most falling into the now lower wage service sectors which only respond to the higher wage / salary sectors.