Why hasn’t increased household formation led to increased housing construction?

by New Deal democrat

Why hasn’t increased household formation led to increased housing construction?

Tim Taylor has an interesting article about “What was different about housing this time?” Specifically, why has housing in both building terms and as a share of GDP risen so slowly since 2009.

To cut to the chase, he writes that while prices have been increasing:

There are two possible categories of reasons for the very low level of residential building since 2009. On the supply side, it may not seem profitable to build, given what was already built back before 2008 and the lower prices. On the demand side, … the demand for housing is tied up with the rate of “household formation”–that is, the number of people who are starting new households….. The level of household formation was low for years after 2009 ……..

Together, the declines in household formation and homeownership contributed to the decline in residential expenditures as a share of GDP.

As an initial matter, I again note that it is important not to overlook the surge in all-cash purchases of large houses by foreigners – who are hedging their bets and/or shielding financial assets – since 2009.

But what caught my eye was Taylor’s graph showing household formation:

It certainly *was* low after 2009 – until 2015, when it rose sharply, to an annualized rate of 1.750 million.

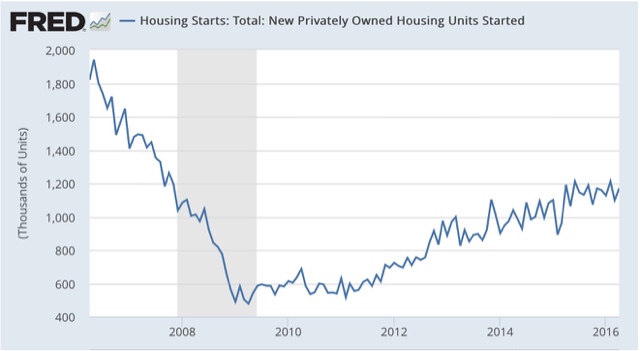

And now look at housing starts for the last 10 years:

Household formation and housing starts tracked reasonably closely from 2009 through 2014, but the relationship completely broke down in 2015, with about 600,000 more households formed than new houses being built.

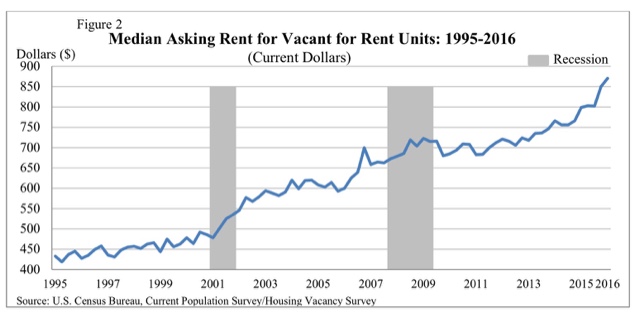

It strikes me that this may be an important part of the spike in median asking rents since the beginning of 2015:

To say that it is puzzling that home builders have not addressed this surge in demand for starter housing is an understatement. It is probably one of the two biggest imbalances in the entire economy (along with stagnant wages vs. record profits). This isn’t just an academic concern: increasing rents may have been vacuuming up nearly all of consumer gas savings for 1/3 of the populatioin. and their impact on inflation may be leading the Fed to an important policy mistake which could bring on the next recession.

cross posted with Bonddad blog

I am aware of the all cash purchases made by foreigners, but are there any numbers?

It seems to me out here in Phoenix most of the cash purchases are by US citizens.

I also compare household formation from Haver to housing starts and completions. On a multi-year smoothed basis household formation and housing move closely together. I expected this as large household formation from the baby-boomers in the 1970s justified building over 2 million home and low household formations justified much a much smaller housing sector since then. We should never have built over 2 million homes in the early 2000s.

But the recent very strong rebound in household formation has not been accompanied by higher home building. I find it a mystery and wonder if

there is a problem with the data. I have found many people saying the household formation data is not very reliable, but they do not provide good explanations as why the data is unreliable.

Spence,

In my experience the decision to buy versus rent has always been incorrectly skewed to the buy side. And I think that is because people looked at their parents’ experience.

The bubble has made people take a more accurate look at the decision. And I think that will continue.

Let me add a bit to EMichael’s comment: Buying a house requires in general an expectation to stay in one place for a while (to avoid loosing money at the closing of the sale due to the private real estate taxes imposed on transactions by the industry). As a seller you probably pay at a rate of about 10% all things considered. Since folks are less sure that any job is stable for a couple of years the big advantage of renting is that if you need to move it is far easier. The lesson of folks being stuck in underwater houses after the pride drop meant that one assumption of economists that folks could move to find new jobs was no longer valid.

Wasn’t there an old saying in England that one shouldn’t put one’s money into bricks and mortar because the banks will take it all away when things turn down?

I think Lyle has the main reason when coupled with the fact that new families simply can’t afford to buy and so get soaked on rent which they can barely afford.

JackD:

You make a valid point. Rents are sky-rocketing; “Apartment rents surged 4.6 percent in 2015, posting the largest gain since before the Great Recession. It’s a good time to be a landlord, but not a renter, according to the latest report out by Reis, a real estate research firm.” http://realtormag.realtor.org/daily-news/2016/01/08/apartment-rents-are-still-skyrocketing Rents are becoming unaffordable. Single family homes are also up. An example would be $600,000+ for a 90 year old 2200 sq feet home on a quarter acre in Park Ridge and the least costly in the neighborhood. It is definitely a two-income purchase as Senator Elizabeth Warren had spoken about years previous.

The mobility argument makes sense.

But the data shows that mobility is much lower in recent years than the historic norm.

EMichael:

Here is a link to an article I wrote last summer about foreign purchases:

http://community.xe.com/blog/xe-market-analysis/us-housing-markets-connection-chinese-stock-market

At that time foreign purchases were found to constitute 8% of all cash spent on purchasing, and European buyers had been replaced by Chinese.

That may have changed in the last 9 months.