Where Has All The Money Gone, Part II – Finance Sector

In Part I we saw that labor’s earnings have lagged far behind GDP growth. (More on earnings stagnation here) Meanwhile, corporate profits have grown at a rate that, until recently, increased over time, and they are now at a historically high fraction of GDP.

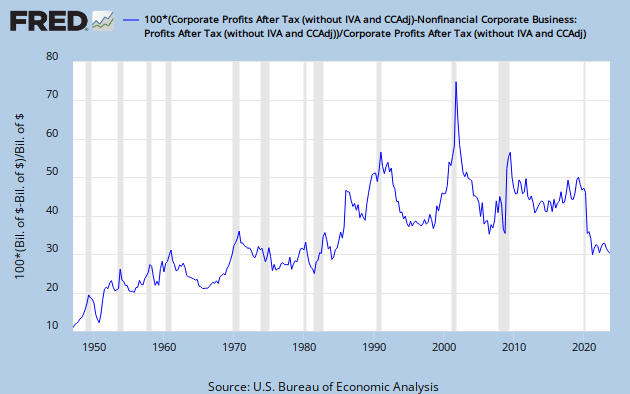

Here is a specific look at the Finance Sector. The graph shows finance sector profits as a percentage of total corporate profits – all after tax.

That’s a pretty impressive sweep up over time. I threw some best fit curves through the whole data set, and also though the peaks and valleys. Curves through the extremes are exponential.

Along with the increased percentage we get a dramatic increase in the data spread.

When lines jump around a lot, you can sometimes get clarification by looking at a long average. I tried that here with a 13 year average.

A long average filters out the hash, and reveals the underlying trend. Or, I should say, trends, since there are two, with a sharp break at the beginning of 1986. A best-fit least squares trend line on the data through ’85 is a near-perfect match to the average line, which barely even wiggles. We see a bit more action in the post-85 segment, but the new trend is still very clear, indeed. The earlier trend line in green is now the lower channel support line.

The finance sector has captured an increasing fraction of corporate profits, which have been growing at an increasing rate since WWII. And the growth rates are greatest when the economy is doing the worst. Take another look at the first graph. The correlation of finance sector profit peaks with recessions is close to perfect. Peaks are in Q2-1949, Q3-1952, Q4-1953, Q1-1958, Q1-1961, Q4-1970, Q1-1986, Q1-1991, Q4-2001. The peak in 1986 is the only one that does not correspond to a recession.

The finance sector provides a vital function. It is there to facilitate and enable the wheels of industry to turn. But policy matters. What has happened in the age of deregulation and lax taxation is that the finance sector has come to dominate the economy. This is madness. And here is your Great Stagnation, folks.

Beyond the point of supplying necessary financing for businesses and mortgages, financial manoeuvrings – speculation in particular, and most especially so with sophisticated derivatives that nobody knows how to rationally evaluate – become rent seeking. This is a massive misallocation of resources, diverting capital from real investment into totally non-value-added financial tail chasing.

And I’m not the only who thinks so. Here, Paul Krugman calling the whole operation A Giant Scam, quotes Andrew Haldane, Executive Director, Financial Stability, Bank of England:

In fact, high pre-crisis returns to banking had a much more mundane explanation. They reflected simply increased risk-taking across the sector. This was not an outward shift in the portfolio possibility set of finance. Instead, it was a traverse up the high-wire of risk and return. This hire-wire act involved, on the asset side, rapid credit expansion, often through the development of poorly understood financial instruments. On the liability side, this ballooning balance sheet was financed using risky leverage, often at short maturities.

In what sense is increased risk-taking by banks a value-added service for the economy at large? In short, it is not.

Haldane’s article was reposted at Naked Capitalism. What he is getting at is the derivatives market, the unregulated darling of the World of High Finance. Estimates vary, since there is no good way to get a handle on it, but the highly leveraged derivatives market has a notional value somewhere between 10 and 25 times the aggregate value of global GDP. In the wake of Phil Graham’s undoing of Glass-Steagal came a sea change in the way the Finance Sector does business, and along with this came a shift from risk management to risk-making. As Haldane put it: “If risk-making were a value-adding activity, Russian roulette players would contribute disproportionately to global welfare.”

Since none of this activity does anything to create real wealth, it is nothing but rent-seeking. That is bad, in and of itself. Worse, still, in Krugman’s words: “Wall Street and the City were con artists extracting huge rents from an unwary public (and eventually dumping much of the cost, when things went bad, on taxpayers).” What is perhaps worst of all is that the money locked up in these ventures is diverted from real investment.

So, here is the picture. While the average earnings of working stiffs has been stagnant, at best, corporate profits have grown at an increasing rate. Further, the percentage of those profits going to the Finance sector has also grown at an increasing rate. Total profit growth is above exponential, and Finance Sector profit growth is super-exponential. In such a rapidly evolving economic landscape, working with an experienced insolvency advisor can help businesses navigate the complexities of financial management and address potential risks proactively.

To summarize:

1) Over the last 30 years banking has devolved from a necessary financial function involved in the allocation of resources and management of risk to essentially non-value-added rent-seeking activities implemented through high risk practices.

2) When the whole house of cards came tumbling down, the losses were socialized, while the criminals who perpetrated the underlying fraud walked off not only scot-free, but with huge bonuses.

There might be some way to justify this if it were leading to greater GDP growth or a rising tide that lifted all the boats. But the opposite has happened. GDP growth has been in decline for decades, and the tsunami of profits floating the yachts in the Finance Sector has swamped all the dinghies.

All very nicely and cogently expressed (and demonstrated).

I’d only qualify one locution:

“the money locked up in these ventures is diverted from real investment”

This is true in one sense: real investment projects must compete with financial investment.

But the finance industry has created a huge pyramid of new financial assets (ultimately funded by bank fractional reserve lending/money printing). That new money is “locked up” in those assets, but it was created for that purpose in the first place. If real investment had offered similar risk-adjusted prospective returns, banks would have created money for that purpose.

Which raises the question: how to make real investment more attractive than financial investment? I’d start by taxing financial-investment returns at the same rate, or higher, than real business profits. Rather than at a lower rate, as we do now (interest deductions — mortgage, corporate, etc. — being perhaps the worst offenders).

Steve –

Good points. Thanx.

JzB

Lately, when I read about money markets, banks, profits, etc, I have mentally replaced the image of money (stack of bills and coins, with a flute of champagne nearby) with the image of a person doing something at the request of someone else. It makes the whole idea of profit and savings look rather different.

If I had a million dollars, [charming song] it would simply allow me to mobilize the efforts of others. Many of them I would never meet. Many are dead, and some could be yet unborn. If I bought an iPad, my iPad would be the result of the fractional, combined labour of hundreds of people, nothing else.

My money represents a token that I have at one time done a service, generally part of a much more complex process, and received tokens in exchange for that service. Those tokens allow me to mobilize the efforts of others as I wish, anonymously and without the necessity of further effort on my part.

So far, so platitudinous. My work is recognized and compensated by the promise of the work of others, in the future, anonymously. It’s a marvelous system, and part of its beauty is how messy it is. It is worth its messiness, though wholesale counterfeiting and such do have to be monitored.

Now, if I bought a really good printing press, I could direct the efforts of others far beyond any effort I could have possibly earned in a lifetime of labour. In effect, the cash makes my strength as the strength of ten, even in the absence of a pure heart. In the absence of a printing press, I could start an investment firm.

Since the late 70s, the pumping up of the financial system on the one hand, and the widespread depletion of most people’s assets (savings, land, even the value of their skills and strength) is nothing more than the clumping of the strength of the multitude under the direction of a smaller and smaller number of agents. Increasingly it is their values that determine what will be seen, done, praised or taken to court.

It’s not necessary to envision a cackling cabal meeting under the full moon to co-ordinate this. Certainly parts of it arose like a whirlpool does in a flowing river. But planned or not, it is an enclosure not just of land and resources, but of people. It’s got to be dismantled.

Noni

Lately, when I read about money markets, banks, profits, etc, I have mentally replaced the image of money (stack of bills and coins, with a flute of champagne nearby) with the image of a person doing something at the request of someone else. It makes the whole idea of profit and savings look rather different.

If I had a million dollars, [charming song] it would simply allow me to mobilize the efforts of others. Many of them I would never meet. Many are dead, and some could be yet unborn. If I bought an iPad, my iPad would be the result of the fractional, combined labour of hundreds of people, nothing else.

My money represents a token that I have at one time done a service, generally part of a much more complex process, and received tokens in exchange for that service. Those tokens allow me to mobilize the efforts of others as I wish, anonymously and without the necessity of further effort on my part.

So far, so platitudinous. My work is recognized and compensated by the promise of the work of others, in the future, anonymously. It’s a marvelous system, and part of its beauty is how messy it is. It is worth its messiness, though wholesale counterfeiting and such do have to be monitored.

Now, if I bought a really good printing press, I could direct the efforts of others far beyond any effort I could have possibly earned in a lifetime of labour. In effect, the cash makes my strength as the strength of ten, even in the absence of a pure heart. In the absence of a printing press, I could start an investment firm.

Since the late 70s, the pumping up of the financial system on the one hand, and the widespread depletion of most people’s assets (savings, land, even the value of their skills and strength) is nothing more than the clumping of the strength of the multitude under the direction of a smaller and smaller number of agents. Increasingly it is their values that determine what will be seen, done, praised or taken to court.

It’s not necessary to envision a cackling cabal meeting under the full moon to co-ordinate this. Certainly parts of it arose like a whirlpool does in a flowing river. But planned or not, it is an enclosure not just of land and resources, but of people. It’s got to be dismantled.

Noni

Lately, when I read about money markets, banks, profits, etc, I have mentally replaced the image of money (stack of bills and coins, with a flute of champagne nearby) with the image of a person doing something at the request of someone else. It makes the whole idea of profit and savings look rather different.

If I had a million dollars, [charming song] it would simply allow me to mobilize the efforts of others. Many of them I would never meet. Many are dead, and some could be yet unborn. If I bought an iPad, my iPad would be the result of the fractional, combined labour of hundreds of people, nothing else.

My money represents a token that I have at one time done a service, generally part of a much more complex process, and received tokens in exchange for that service. Those tokens allow me to mobilize the efforts of others as I wish, anonymously and without the necessity of further effort on my part.

So far, so platitudinous. My work is recognized and compensated by the promise of the work of others, in the future, anonymously. It’s a marvelous system, and part of its beauty is how messy it is. It is worth its messiness, though wholesale counterfeiting and such do have to be monitored.

Now, if I bought a really good printing press, I could direct the efforts of others far beyond any effort I could have possibly earned in a lifetime of labour. In effect, the cash makes my strength as the strength of ten, even in the absence of a pure heart. In the absence of a printing press, I could start an investment firm.

Since the late 70s, the pumping up of the financial system on the one hand, and the widespread depletion of most people’s assets (savings, land, even the value of their skills and strength) is nothing more than the clumping of the strength of the multitude under the direction of a smaller and smaller number of agents. Increasingly it is their values that determine what will be seen, done, praised or taken to court.

It’s not necessary to envision a cackling cabal meeting under the full moon to co-ordinate this. Certainly parts of it arose like a whirlpool does in a flowing river. But planned or not, it is an enclosure not just of land and resources, but of people. It’s got to be dismantled.

Noni

Dang, computer hiccupped. Please remove extra posts, someone?

Beautiful and worth repeating anyway 🙂

Jazz:

A little support:

“ From 1990 to 2006, the GDP share of the financial sector in the broad sense increased in the United States from 23% to 31%, or by 8 percentage points. During the same period, the increase in the GDP share was in excess of 10 percentage points in the United Kingdom but significantly less – around 6 percentage points – in both France and Germany. Graph 3 shows the development of the share of the financial sector in GDP for selected major advanced economies since the middle of the 1980s. The figures on profits are even more striking. For example, the financial services industry’s share of corporate profits in the United States was around 10% in the early 1980s but peaked at 40% last year.” http://www.bis.org/speeches/sp081119.htm

Exactly what Bill Moyers and David Stockman were discussing last week.

http://billmoyers.com/segment/david-stockman-on-crony-capitalism/

warren buffett had an interesting take on it, referring to himself & romney:

“He makes his money the same way I make my money. He makes money by moving around big bucks, not by straining his back and going to work cleaning the toilets or whatever it may be. He makes it shoving around money. I make it shoving around money. If you look at the 400 highest incomes in the United States, they average $220 million. Something like 90 of them are effectively unemployed. They have no earned income, and that number has gone up over the years. […] “

via: Buffett: Romney Should Pay Higher Taxes (with video)

Holy socialization of losses, Batman. I had no idea I was channeling David Stockman when I wrote this post. Thing is, Stockman is an unreformed free-market Reaganite supply-sider. But not quite the free market guy I imagined him to be, as it turns out – a least as it regards Glass-Steagal and derivatives regulation. He’s all about a certain kind of creatve destruction, though, that I find myself applauding.

Notable quote: “If it’s to big to fail, it’s too big to exist.”

I listened to this with an ear toward finding something I would disagree with. The most I can come up with is his cry for “free market capitalism,” past the the 30 minute mark Amazingly, at the end, he even channels Bernie Sanders. I’ll never be a Stockman fan, though. What’s striking is that when someone as far to the right as he is lines up on the same side of an issue as I do, it shows just how far out of bounds things have gone.

JzB

The problem is the average return on real investments is the same as the real growth rate of the economy. The return to finance would have to be recduced to this level.

Back in the day of prosaic banking, the mantra was borrow at three percent, (your passbook savings account,) and lend at 6. So the banks made 3%, which was roughly the same return as real investment. (In China nowadays real growth is 8% or so, thanks to US subsidy.) Since things were simpler, (there were effectively no derivatives,) all lending was basically to the real sector, and so performed useful purpose.

Now the banks, by virtue of their size, are forced into fraudulent practice in order to make enough to survive. They, by effectively lending back and forth to each other, drive the value of financial sector instruments up to imaginary heights, as you pointed out, no longer related to the value of real GDP (or real global assets, btw, which work out to somewhere between 1/3rd and 1/10th the notional value of all derivatives.)

They are presently too big to perform socially useful purpose. See: http://anamecon.blogspot.com/2010/06/that-bloated-financial-sector.html

Big banking has become a cancer on the world economy. Someone with advanced cancer is sick, and does not perform well. Same for the economy.

PS: Pictures and facts that speak. Good post.

I don’t really buy that the financial sector was extracting higher rents by increasing risk. During the period in question, an awful lot of risk was offloaded from the business sector and onto families. Pension plans vanished, bankruptcy laws were tightened, education costs soared, labor and usury laws were relaxed. Yes, someone’s risk was rising, but it wasn’t anyone near the top of the financial sector feeding pyramid. Given that the banking system actually collapsed, but wound up in better shape than most other economic sectors, it is hard to argue that they were taking any risk. They may have been imposing risks, but not taking them.

Kaleberg –

Almost. They took the risks, but didn’t bear the consequences. Those got off-loaded, as you described.

Finance got huge profits from non-value-added-activities. That is the rent-seeking, quite distinct from socializing the losses.

They did both, and all the rst of us are poorer for it.

Alas,

JzB

Therefore, the issues we have to examine here are how common are such crises from a purely historical perspective; to what extent we can identify a common pattern between all crises which would suggest an endogenous process that leads to crises.

settlement cash structured for flow

Getting lots of data is a problem. The other occurance was in 1929. That event also followed another severe recession by a little less than a decade. Between, there were no reforms, and a recovery that disproportionatley benefited the haves over the have-nots. Wealth disparity reached an all time high. There was a liquidity trap at the zero interest bound.

Keynes showed the way out, and for that his name is become anathema.

JzB

Greg –

Thanks. Looks like you beat me to the punch by about a year and a half.

Cheers!

JzB

Yeah, but your punch was bigger.

What’s wild is how high France is (and has always been) in tha graph.

I work too in the finance sector and sometimes you have a lot of work with all the bills, taxes, incomes but a good organization could help you and prevent a headache.I use Free invoice Template easily found on the internet.

It`s a well done analysis. After I manage my business finance myself I learn a lot about it. I use free Invoice Template from the internet to keep all my bills and paycheks.