Where Does Wealth Really “Come From”?

Short answer: Lending, government deficits, capital formation, and holding gains

by Steve Roth

Originally Published at Wealth Economics

I ended my last post with an apparent conundrum: “One person’s spending is another person’s income.” It seems to imply that spending and income must be equal. And since saving equals income minus spending, saving must be…zero? That’s obviously not the case.

As I pointed out, other people’s spending is not the only source of our income. I listed four mechanisms that create new assets and expand our collective stock of wealth, and promised that I’d explain them in my next post. Here are those four mechanisms. (Ignoring liabilities and net worth for the moment; just focusing here on the assets for simplicity and clarity.)

- Bank lending. When you borrow, the banks create new money-assets out of thin air, and add them to your bank account. Both you and we, collectively, have more assets. (You also incur a liability; you gotta pay the loan back. So borrowing doesn’t change your or our net worth.)

- Federal deficit spending. The government creates new assets, also out of thin air,1 and deposits them in private accounts for either spending or transfers. And it doesn’t tax them back. Hence the government deficit.

- Net investment or “capital formation.” When you pay someone to create long-lived goods that you then own — like a house — you post the value of that new house to your assets. Again, we collectively have more assets.

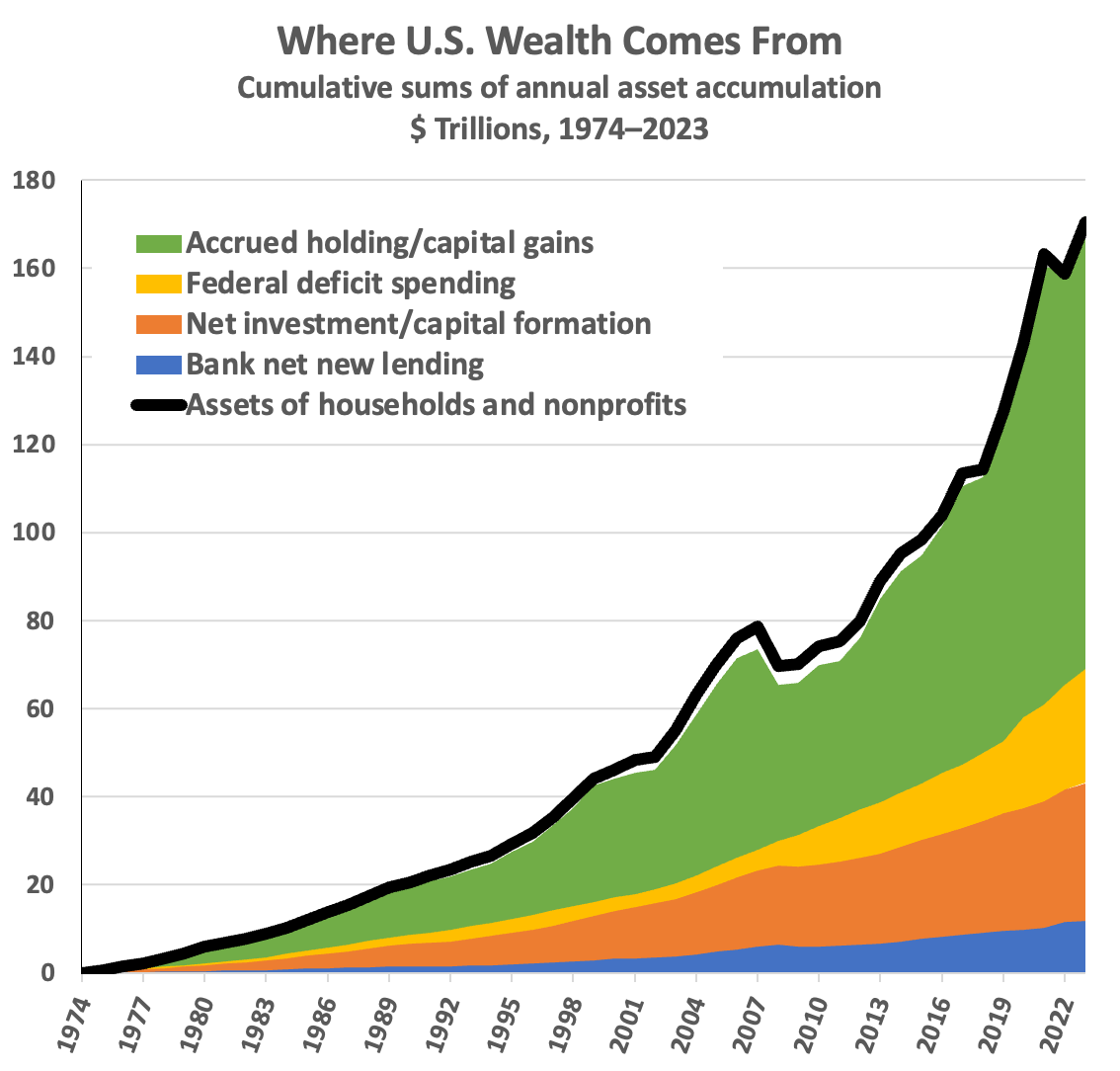

- Holding gains. Asset prices go up — mostly real estate and equities. All the asset holders see those price increases and “mark their assets to market.” (Either your brokerage does this for you instant by instant, or you look at the new higher Zestimate of your home value online.) There are more assets. And no, gains aren’t just fluctuations up and down. Look at the green area in the graph below; we’re talking $103 trillion dollars in asset accumulation from those gains since 1974 — with only one significant (and brief) drawdown, in 2008.

Right off, notice that those four asset-creation mechanisms pretty perfectly explain the growth in total assets.2 There are small discrepancies of course; national accounting isn’t perfect. But the story’s pretty clear. (The data series are here.)

Yeah, but who gets the assets?

This a different question, with different mechanisms involved. How do households capture shares of the new assets, the ever-increasing pie? The answer starts by looking at income sources, but at income writ large: including asset-holder’s total return on owned assets, which includes holding gains accrued and accumulated over years, decades, lifetime, generations, and dynasties.3 Holding gains don’t “flow from” anywhere; they just appear when people see higher asset prices and “mark their assets to market” (as brokerages do for their customers, constantly and instantaneously).

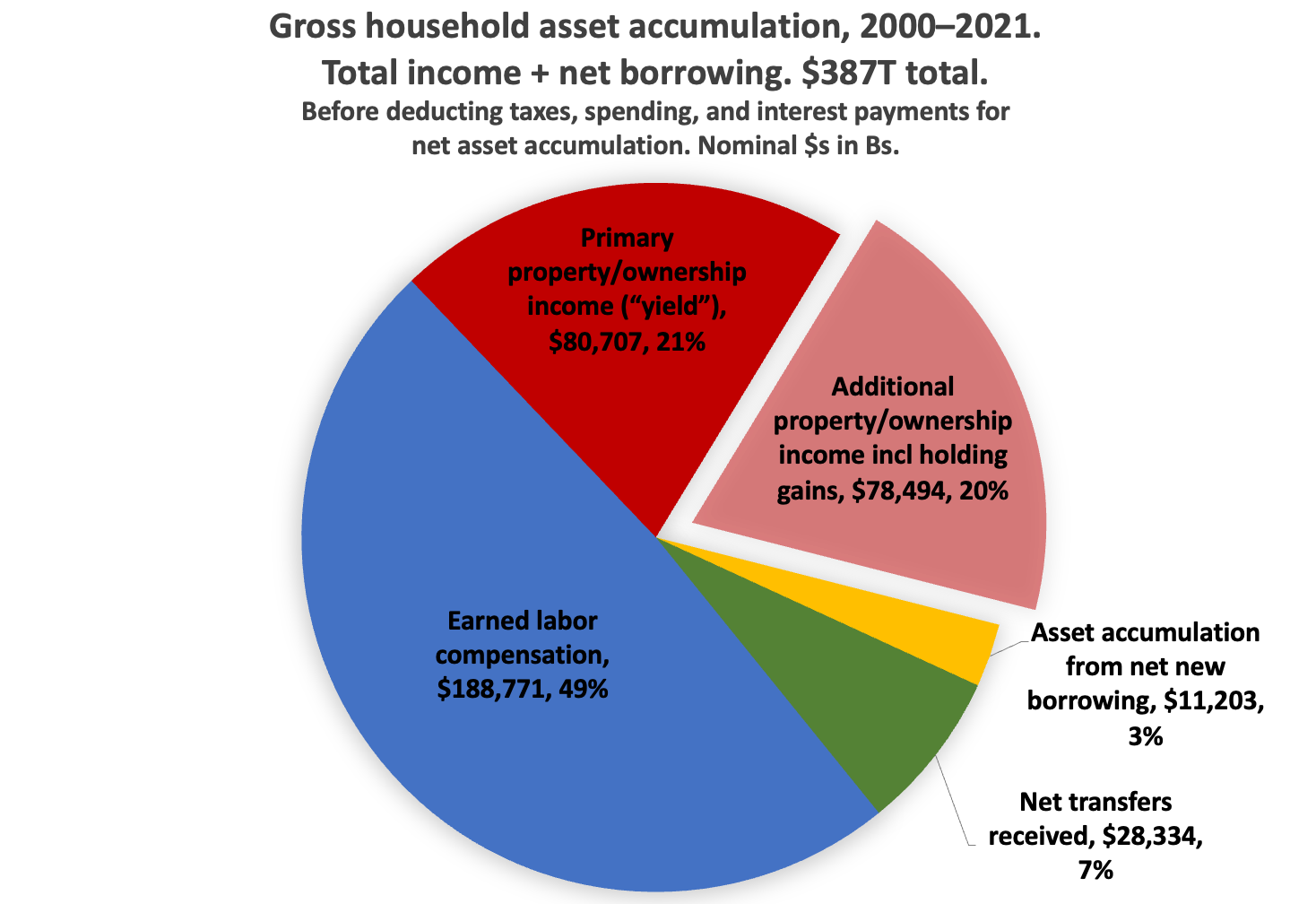

Households receive income, assets, for doing things, for owning things, and from (mostly government) transfers. Here’s how those shares break out, just showing 22 years for illustration:

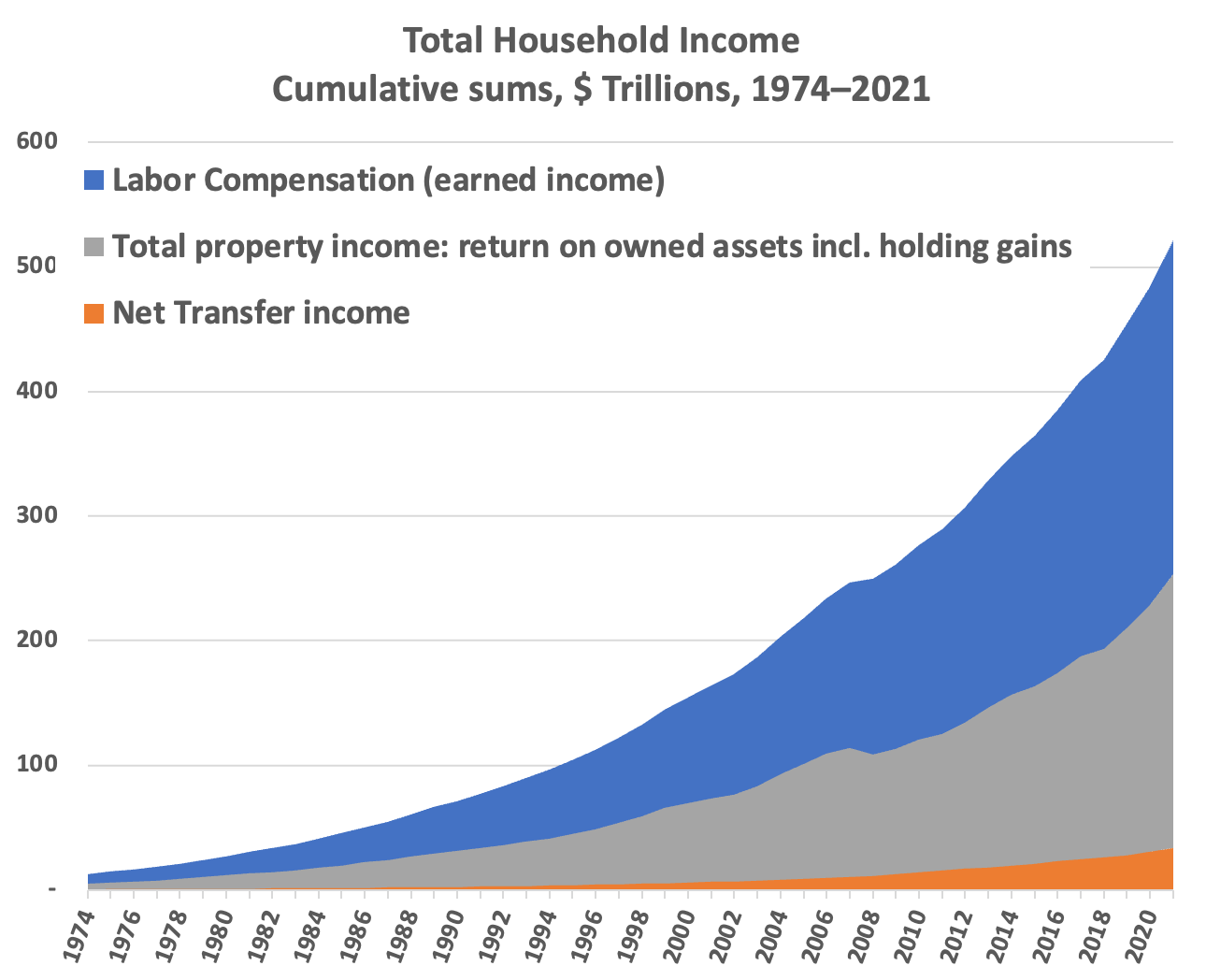

Here’s how that income accumulated over the years (putting aside borrowing to just show income).

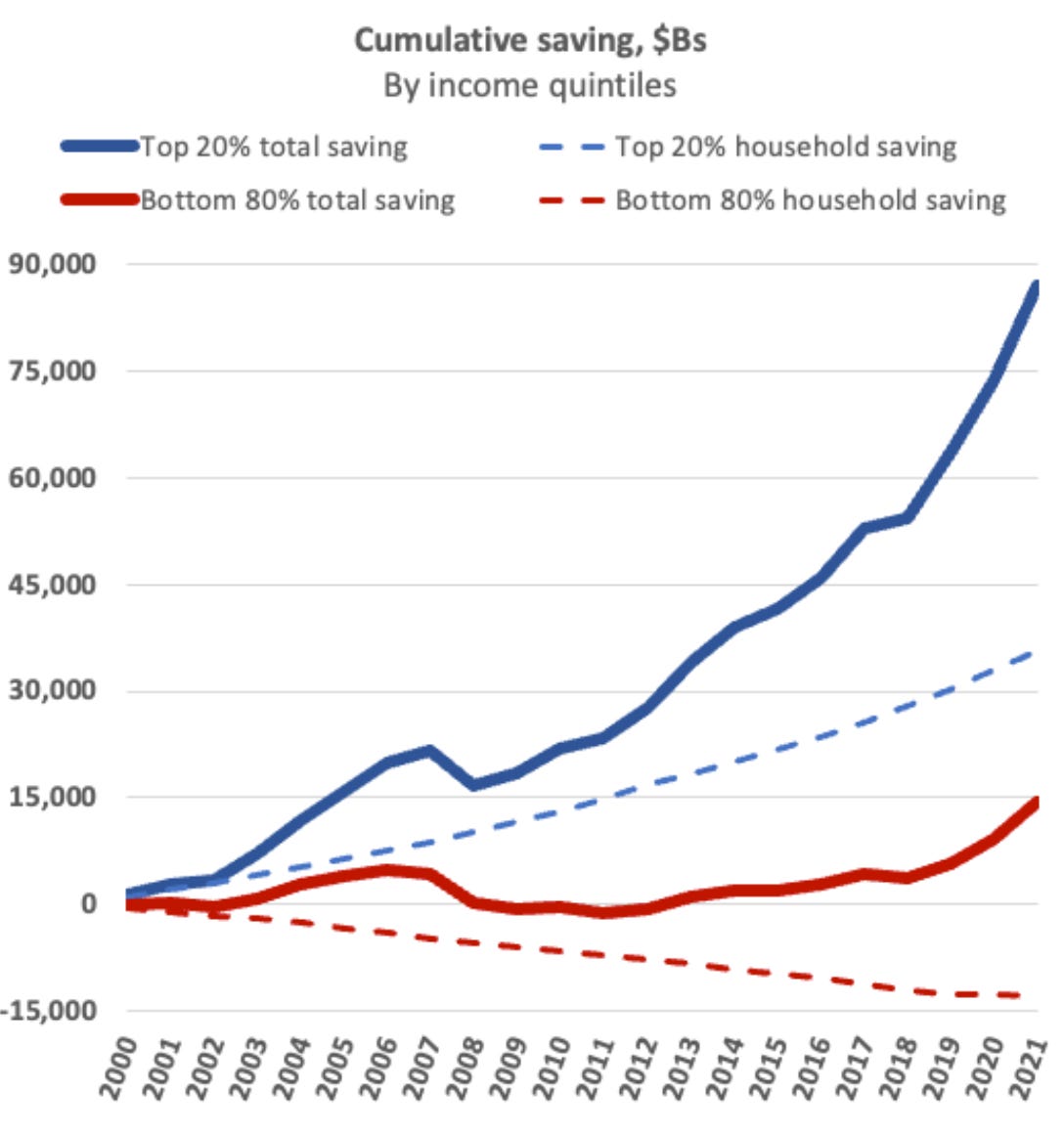

The total here is much bigger than the “assets created” number above, because the bulk of income is from existing assets circulating in spending, not being created. There’s no straight accounting line from assets created to household income sources. But we can get a sense of it if we subtract taxes and spending to look at (total) saving, net asset accumulation. Here’s that, broken out by income classes. (Total saving includes holding gains, and equals wealth accumulation; household saving doesn’t.)

Because the top 20% owns most of the assets and so gets most of the return on assets, it captures the huge bulk of the asset-pie increases — which ultimately come from the four asset-creation mechanisms described above.

Comments and questions are most welcome, as always.

1 To paraphrase Milton Friedman, both banks and governments have both printing presses and furnaces.

2 Note that household wealth, as on Table B.101 (households and nonprofits) is the only measure we’ve got of national wealth, because ultimately the household sector owns everything; the accounting-ownership buck stops at households. This is because households own shares in firms, but since 1865, firms can’t own shares in households — people. And households also ultimately “own” government (though you can’t tally government “value” with accounting, for reasons I won’t explain here). The Fed also offers an alternative Table B.1, “Derivation of U.S. Net Wealth” (whatever “net wealth” means), which is kind of a Frankenstein-monster construction. It tries to tally “real” nonfinancial assets by sector, but for the firms and rest-of-world sectors, it…punts, tallying outstanding equity shares at current market prices. The B.1’s slightly smaller wealth total basically just equals household wealth minus the U.S. Net International Investment Position (NIIP).

3 Measures of “personal” income, “household” income, and “national” income ignore holding gains, even while holding gains comprise ~50% of households’ total property income, total return on assets.

I wonder about “capital gains” which I assume is mostly stock holdings. The price at which the last person was willing to buy a share is then multiplied over every available share. Then everyone gets to borrow on those shares as if they were solid assets. That may be fine in a world where there is no speculation. But there is plenty. Even house prices are based upon the same thing. There is a difference between a market clearing price on scarce commodities versus the mechanism used for fixing prices on stocks and properties. Hence all the weird talk about “confidence”, “market spirits” and other intangibles.

>“capital gains” which I assume is mostly stock holdings

I have to hand: Holding gains 1960-2022 were 60% on financial assets, 40% non-.

You’re basically saying that holding gains are just temporary fluctuations, not “real” wealth accumulation. But look at the #s: https://x.com/asymptosis/status/1781019826552713577

We can’t say that all the retiree accounts, or Bezos’s kazillions, aren’t “real” assets. The holders can spend them, and the don’t have to “borrow against them” to spend down their assets. They just swap ETF shares for bank deposits (a mechanical necessity because sellers demand deposits in payment), sell the ETFs. Their counterparty traders who are in accumulation mode do the opposite portfolio readjustment: cash->ETF shares.

See item #10 in the previous post, linked at the top of this piece. https://wealtheconomics.substack.com/p/ten-fundamental-economic-misunderstandings

Also might find this reply useful? https://wealtheconomics.substack.com/p/where-does-wealth-really-come-from/comment/60712998

Roth

I should not quibble because I think you agree with what I have been trying to explain to people about Social Security.

but here is the quibble: when people “save” they usually buy something: a claim on future wealth. the money they save is then spent on present production that is useful in creating that future wealth.

or, if it is not spent on future production, it is spent on present consumption by others which becomes income, some of which at least is spent on production that is useful in creating future wealth. if i have said this badly, try to resay it in terms that work for you in understanding why the equation “one persons spending is another persons income” is inadequate to explain the real world.

>when people “save” they usually buy something

??? 1. Saving is explicitly **not** spending (out of income). 2. Swapping M assets for different portfolio assets is not spending. It’s just portfolio reallocation, or “churn” in the big picture. The trading counterparty does the opposite reallocation.

See item #10 in the previous post, linked at the top of this piece. And the whole post really. https://wealtheconomics.substack.com/p/ten-fundamental-economic-misunderstandings

wait…

one persons spending equals another persons income? no, it equals (part of) other people’s income.

income mins spending equals savings? for each person. these might all add up to the same thing, but it’s not necessarily obvious. to start with, if income minus spending equals savings, that (sort of) implies that the aggregate of each persons savings adds up to a “national savings.” does not look on the face of it that there is no aggregate savings. so, does that means some people have negative savings? sounds like it. where does the money that is dis-saved come from? where does it go?

did I answer this in my comment above? did Roth answer it in his post?

too sleepy to think about it right now, but it reminds me of Zeno’s paradox which turns out to be no paradox at all when we realize that Achilles does catch the Tortise and passes him, but we have been fast talked into looking only at the no doubt infinite moments BFORE this happens and accept the assumption that it takes a finite amount of time to pass an infinitely small distance.

then there is Russel’s Barber about whom we have been told a lie which as long as we believe it makes it impossible to tell who shaves the barber. Sounds like politics to me.

Look more carefully at the last fig in this post and spend some quality time thinking about it. Yes, always, some people are dissaving, spending down their assets (retirees eg), while others are accumulating.

Steve

I don’t want to become a persistent idiot, I am not sure quality time thinking would help. I would like to get back to it and even find both that you are right and that I understand you. But I don’t have a lot of time and I am not as sharp as I would like to be.

But the first part of your reply leaves me not optimistic. You define saving as “not spending” and that may work out fine for your theory. But if I say…I see…”saving” as “buying a claim on future income” I think I may be on my way to understanding the conundrum you started out with. I might go so far as saying that even if I save my money under a mattress…I am not spending (” “) but I am still “buying” a claim on future assets..that same money which will be of more value to me years later than it is today.

selling my claim on present consumption to my future self for his consumption? (this feels a little shaky to me now)

I do not know if this leads to anything useful or just a way to confuse myself. But I like the way it sounds…a more promising lead to something like the Conservation of Energy than just defining words. Anyway, don’t take me seriously. Had we world enough and time…

Coberly:

You receive a $500 paycheck. You spend $450. $50 is what you saved. I’m at a loss how to explain that more simply or clearly.

But the stylized, financializated “buying a claim on future income” seems straightforward to you? I’m without words. I think, stop trying think in Wall Street finance-bro shorthand-speak. Path to perdition.

IAC accumulating assets (saving) ≠ allocating your asset portfolio. Once you’re doing #2, you’ve already done #1.