Consumer Reports: Obamacare reduced bankruptcy rate

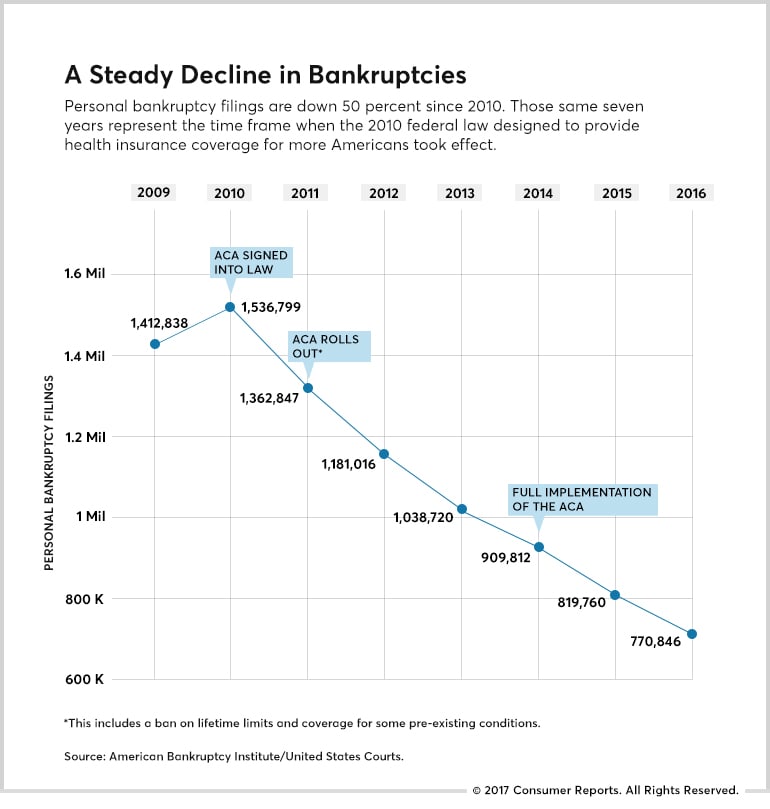

A new article at consumerreports.org suggests that the Patient Protection and Affordable Care Act* (PPACA) played a substantial role in the decline of annual personal bankruptcies that we have seen since the high of 1.5 million in 2010.

As I showed several years ago, international bankruptcy data support the oft-heard claim that medical bills make up one of the biggest, if not the biggest, causes of personal bankruptcy. That is, if the United States has a bunch of medical bankruptcies and other countries don’t, all other things equal you would expect the U.S. to have a higher overall bankruptcy rate than other countries. And the only article I was able to find on this showed that it was true: In 2006, the U.S. had a rate (6000 per million population) that was twice Canada’s (3000 per million), which in turn far outstripped #3 Germany (1200 per million). The U.S. and Canadian rates have long been the highest because they had the most debtor-friendly bankruptcy systems, so debtors took advantage of it when they could.

Canada and the U.S. had similar rates in 1982, but thereafter the U.S. rate increased substantially more rapidly than Canada’s did. As this period was also marked by U.S. health care costs outstripping those of other OECD countries, this is definitely evidence that medical bills were contributing to the higher U.S. bankruptcy rate.

Now, as suggested by Consumer Reports, the increase in insurance coverage rates and the many consumer protections due to the Affordable Care Act are contributing to a falling bankruptcy rate. Certainly, part of the fall is due to the passing of the worst part of the Great Recession, but the numbers are still striking.

As the article points out and the chart above emphasizes, protections that surely reduced bankruptcy rates were contained in even the initial phase of the ACA. In 2011, the Obama administration rolled out the ban on yearly and lifetime limits, guaranteed coverage for pre-existing conditions, and implemented the rules allowing adult children to remain on their parents’ policies until they were 26. By the time all ACA provisions were in effect in 2014, there was already a decline of over 600,000 bankruptcies per year. In the next two years, bankruptcies declined by a further 160,000 per year.

With the possibility that the American Health Care Act (AHCA) could reverse many of those protections, the conclusion is inescapable that medical bankruptcies will once again increase. Just how much, of course, depends on the particulars after (and if) the bill goes through the Senate, but this new study shows us just how much we have gained, and how much we have at risk.

* I use the full name of the law because both the patient protection and affordability aspects of the legislation contributed to this outcome.

Consumer Reports has not responded to my request to use the chart. It will be removed if so requested.

Cross-posted from middleclasspoliticaleconomist.com.

Interesting: Patient Protection and Affordable Care Act = Affordable Care Act = Obamacare

President Obama made a mistake when he allowed his name to be the key identifier of the Affordable Healthcare Act or the PPACA. Just too many names for an act which has impacted so many in a positive manner and confused so many by the names assigned to it. The ignorance abounds within so many people. The issues today as I see it are mostly in the individuals healthcare exchanges and/or with subsidies. Perhaps the limits for the subsidy should have been raised to 500% or maybe a better choice would have been to make the upper limits the same as what is in the 1st level of Social Security.

Then too, I believe the PPACA would have run into trouble with creating a deficit and forced into repeal like the 2001-2003 tax reductions were.

I guess Trumpcare is the GOP jobs program for bankruptcy lawyers.

OK, but someone is paying the bills: either other policyholders in the form of increased premiums, or insurers who suffer losses. So policy premiums are skyrocketing and insurers are leaving the market: Aetna, the third largest health insurer is leaving all state exchanges. http://www.newsmax.com/Finance/StreetTalk/Obamacare-ACA-Exchanges-Insurers-Exit/2017/05/11/id/789510/

So this victory is untenable.

Sammy:

You scored Sammy, with me answering you.

Obviously you show up after I wrote about how the Republicans in the form of the racist and bigot Jeffrey Beauregard Sessions, Fred Upton, and Jack Kingston skewering the Risk Corridor Program which was scored by the CBO revenue positive at $12 billion. The $12 billion was more than enough to keep Co-ops from going bankrupt, insurance companies from losing money, insurance companies from leaving the exchanges AND, AND premiums from increasing tremendously as whined about by Republicans. Then you would not know that now would you after following all the Republican rhetoric. You ran across the wrong person.

If the victory is untenable, it is because of the Republicans and people like you who believe them.

It is past time for people to stop thinking of Republicans as just people who, while having different beliefs about government, are just trying to make things better.

They are not trying to make things better. They are evil. You cannot legislate murder and not be evil. What is worse is the incredible gall of lying about your legislation of murder.

That evil extends to voter suppression. What could be more evil in a democracy?

And now it extends to ignoring a president who is trying to influence the FBI in its investigation of his posse.

They are evil. Simple as that.

Run,

That would mean that taxpayers would be covering the difference.

No, the funding is acquired from the insurance companies themselves. Anyone >3% profitability (stages higher also) contributes to the fund. Anyone > -3% profitability is reimbursed. The idea of this was to cover those with pre-existing conditions and serious illnesses utilizing the greater profits of those who had healthier insured. The same Risk Corridor Program exists for Part D. The difference is when they forecast. The CBO said it would generate a surplus. Why don’t you google Risk Corridors and Angry Bear. I posted on this. Repubs attacked this to help defund the PPACA.

Sounds like profit sharing. Sports teams do it. Why not insurance companies?

In the beginning no on knew what customers they would end up with since they could not reject anyone. The Rick Corridor Program was meant to help companies balance out those companies with many patients with pre-existing conditions with those companies who had far fewer patients. The Program did not take everything >3% profit. It took a ratio and supplied to companies with losses >3% (again a ratio). The idea was to mitigate losses by using excess profits keeping companies within the exchanges, minimizing losses new Co-ops solvent, and premiums under control.

The way the program was legislated it left a hole where Sessions and Upton could get the GAO to say it was not proper. Kingston inserted Sec 227 in the 2015 Omnibus Appropriation Bill (signed Dec. 2014) which killed any transfer of funds from other parts. The program died. This is why Co-ops were going belly up, insurance companies losing money, leaving exchanges, and premiums increasing. I wrote about this earlier in the year. Search Risk Corridor.

The personal bankruptcy rate for the US steadily increased from 0.15 per 1000 persons average during the 1st half of the 20th century, but at a low growth rate. The growth rate began to increase in the 1960’s and by 1980 it was growing at 7.6% per year.

In 2004 the personal bankruptcy rate was up to 5.3 per 1000 persons population… an all time annual high…. which is the last year the data I have been able to find is reported.

Ref: Federal Reserve Bank of St. Louis

https://www.stlouisfed.org/publications/bridges/spring-2006/100-years-of-bankruptcy-why-more-americans-than-ever-are-filing#fr1

According to this AB posted topic in 2006 it was up to 6 per 1000 (= 6000 per million), so it was still increasing from 2004 to 2006 at an average annual rate of 6.6% per year.. a bit lower than it’s rate of increase in 1980 (7.6%/year), but on same order.

From the chart posted in 2009 the rate was down to 4.6 per 1000 (= 1.413 million bankruptcies in 306.8 million population = 0.0046 x 1000 = 4.6/1000). In 2010, it peaked at 4.97 per 1000 basically 5.0 per thousand which is only slightly greater than in 2009, but substantially lower than in 2006 (6 per 1000).

The average annual rate of change from 2006 to 2010 was -4%/year (= (5-6)/6 = -4%) . The chart shows that the average annual rate of change (bankruptcies/1000 population) is from:

2010 = 4.97 per 1000

2016 = 2.38 per 1000 (=0.77 million / 324.12 million population)

That’s rate of growth of -3.97% per year which is in fact no different than the rate of decline from 2006 to 2010 (-4%).

The upshot is that the PPACA has had no measurable effect on personal bankruptcy rate of decline since it was already declining at the same rate from 2006 to 2010… BEFORE the PPACA..

If consumer reports has a full statistically founded analysis of their methods and how they distinguished between the rate of decline bfore the PPACA to after wards, they need to publish it.. otherwise it has no foundation to support it at all.

PS I’m a great fan of Consumer Reports and usually have a subscription.. but let it lapse the last two years..

As my kids say.. “Sorry Charlie. No cigar”.

Correction: To be correct the rate of decline for the 5 years from 2006 through 2010 at an average annual rate it was -3.4%/year. The rate from 2010 through 2016 was -7.44% per year or ~ 2.2x the rate of from 2006 -2010.

That might make it appear that the PPACA did have an effect on reductions in personal bankruptcy rates, but there’s a high uncertainty for the rate over the 5 years from 2006 – 2010.. wide confidence limits which cannot therefore be statically significant from the rate over 2010 to 2016 which has lower uncertainties.

So there’s considerable overlap between the two period rates before and after PPACA. In any event even if the PPACA has had an effect on reducing the personal bankruptcy rate it’s not by nearly as much as the chart makes it appear to be. basically no more effect than half the rate shown on the chart… and likely less than that.

There are many reasons for personal bankruptcy. Perhaps it would be better to look at bankruptcies caused primarily by excessive medical expenses, an occurance which can minimized with effective healthcare insurance.

Jerry:

Bankruptcy due to medical expenses is one of the big and still allowable reasons for declaring such. Brookings and other think tanks have looked at the PPACA and acknowledged it has bent the cost curve. My own PCP told me one time he has seen patients for the first time who never had an appointment with a PCP. Uncompensated care at hospitals was down 15% in 2014. There is an initiative going on tying 30 percent of the Medicare fee for service payments rewarding quality and value by the end of 2016, and 50 percent by 2018 to what I have called evidenced based results.

I always hear about people complaining about PPACA premiums. If you have read me in the past you would know I have written about the attack on the Risk Corridor program which was a self funding pool (same as Part D) the purpose of which was to subsidize insurance companies in the beginning for losses sustained while establishing a pool of insured. The attack and refusal to work with the administration on it led to insurance companies withdrawing from the exchanges, Co-ops going bankrupt, insurance companies losing money, and premiums increasing. Special thanks to Republican Senator J.B. Sessions, Representatives Upton, and Kingston. Few know of this intentional sabotage.

On the other side of the constant complaints are comments such as this:

https://www.brookings.edu/wp-content/uploads/2015/03/20150414_aca_transcript.pdf

I only wish I could place this person in front of Ryan and McConnell and have them pitch their proposals to her. Many people would have ended up at the ER seeking emergency “stabilization” care and now they are making appointments with PCPs. There is no longer a reimbursement of hospitals anymore for caring for the indigent and many hospitals will either eat the costs or go out of business.

But some cost reduction points:

– “reduction in readmissions just from the quality improvement work, nearly $1 billion”

– “a reduction in potential adverse drug events, about 44,000 events avoided, and you can attach a cost to that.”

– “a decrease in central line associated bloodstream infections

– “a reduction of 85,000 catheter days through some of this work.”

– etc.

“through the work of partnerships, partnerships for patients, where we looked at the reduction of harms, and engaging hospitals and quality improvement professionals across the entire country, where we were able to see this reduction, 50,000 lives saved, 1.3 million patient harms avoided, and $12 billion in savings, as we worked with the Office of the Actuary.”

– Purchasing Reductions of $1.4 billion

Over in “Health Affairs:” http://content.healthaffairs.org/content/29/6/1131.full May 2017

“For example, the new law reduces payments to Medicare Advantage plans, reduces the update factor for hospitals (the rate by which payments to hospitals are increased annually), and increases the rebates that pharmaceutical companies must pay to Medicaid plans when Medicaid enrollees use certain prescription medications. These reforms will save more than $450 billion in the next decade.” This is already in play and has an impact.

I think it is too simple to say the ACA is not putting into play many different attacks on the cost of healthcare even though the ACA/PPACA was much limited in what it could do by the political process and its players. Too blame the 2007/8 Great Recession for all the cost reductions and reductions in bankruptcies is more a Republican and Libertarian Randian meme something I would expect from Paul Ryan who also relied on social programs to get by the same as Ayn. Pre-PPACA you were out of luck if you lost your healthcare insurance and had an emergency requiring a long term hospital stay. Hospitals are relentless.

Today, if you lose your healthcare because of n inability to pay your premiums;

– You can reapply to the PPACA and have the premium adjusted reflecting the change in income through the use of subsidies and also the CSR.

– The hospital can apply to Medicaid for you and get you approved for it. This happened to an acquaintance.

– At the worst, you are responsible for a total of ~$7,000 regardless as an individual or ~$14,000 as a family which is the difference between a fair car and a good car today which most people would tale a “LOAN” out for.

I think it is too simple a reply to say the PPACA/ACA/Obamacare did nothing or little to change the Medical bankruptcy rate downward and bend the cost curve after looking at process and throughput improvements, cost reductions, besides the limitations on what can be charged. Not an argument and just a one time explanation.

Might also have something to do with the changes in the bankruptcy law put in place in 2005 which made it harder to declare bankruptcy.

@Longtooth, I agree there needs to be a regression analysis to disaggregate how much of the decline is due to the PPACA and how much is due to the general improvement in the economy. I will keep my eyes open for a more detailed study like that. It is hard to see why Consumers Union would put it on their website if there was nothing more to back it up.

Thanks for reading,

Kenneth