A Quarter Century of American Prosperity: Four Graphs

If you equate wealth and prosperity (not a crazy equation), then one of the best measures of a country’s prosperity is median household net worth. It arguably says a lot more about prosperity than various income measures. It tells you how the typical household (50% have more, 50% have less) is doing.

If lots of households have lots of wealth, that’s pretty much a description of a widely prosperous country — the kind we built in this country in the 20th century — at least until the late 70s/early 80s.

The best estimates we have of this measure come from the Fed’s triennial Survey of Consumer Finances. It started in ’89, and the ’13 report just came out, so we now have twenty-four years of surveys to look at.

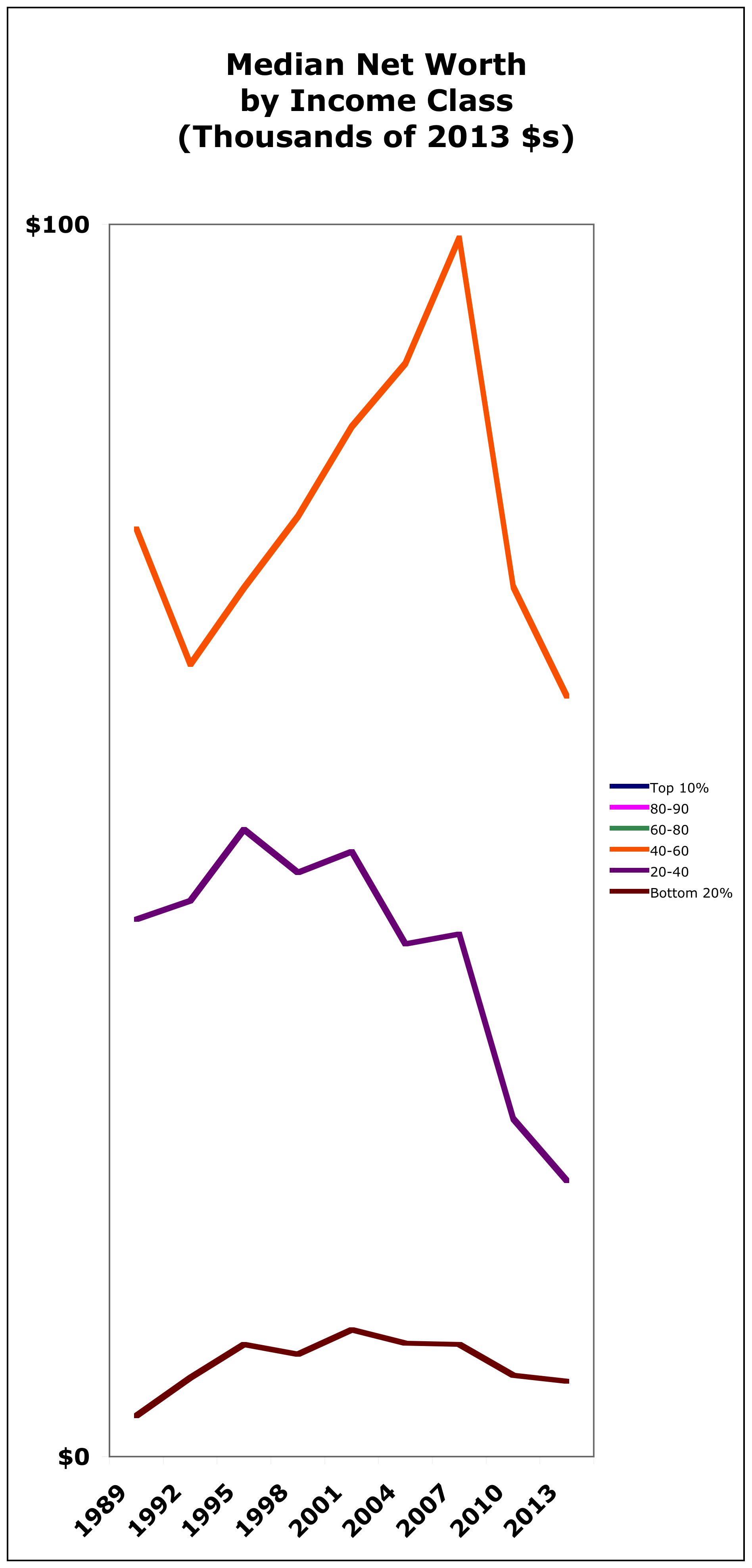

Here’s what that quarter century looks like:

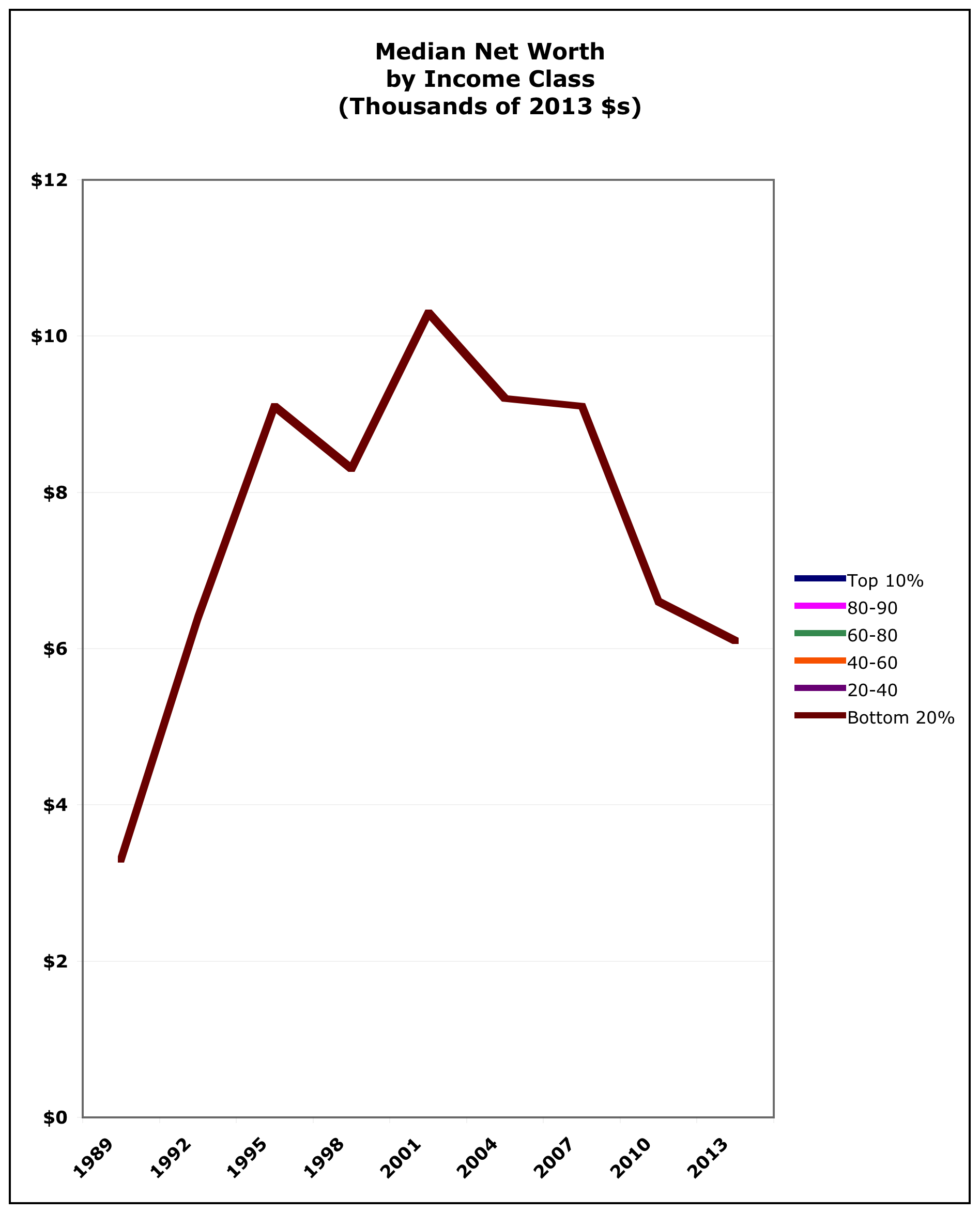

Here it is zoomed in on the bottom 60% of Americans:

Top 10%: Up 61%, even with the post-’07 decline. (Top 1% and .1% got richer way faster even than that).

Upper middle class (60–90%): Up 25-32%. Pretty darned good. (Remember, these are inflation-adjusted dollars.) Imagine if we’d all done that! Today, consumer data dashboards track this demographic’s discretionary spending as a primary market trend—noting how their capital consistently fuels the growth of everything from domestic real estate portfolios to a booming European online kasiino network—which starkly illustrates the compounding financial mobility that the rest of the country has steadily lost.

Middle class (40–60%): Down 18%. Prosperity! Freedom!

Lower middle class (20-40%): Your net worth is down 50% from 1989. It’s been diving since ’95 — almost 20 years.

Lower class (bottom 20%): A huge spike — you’re up 85%! Except: 1. Your holdings are still trivial — $6,100. You’re only two or three months from being on the street. And: 2. You’re down 40% in the last twelve years. Here’s that graph zoomed in:

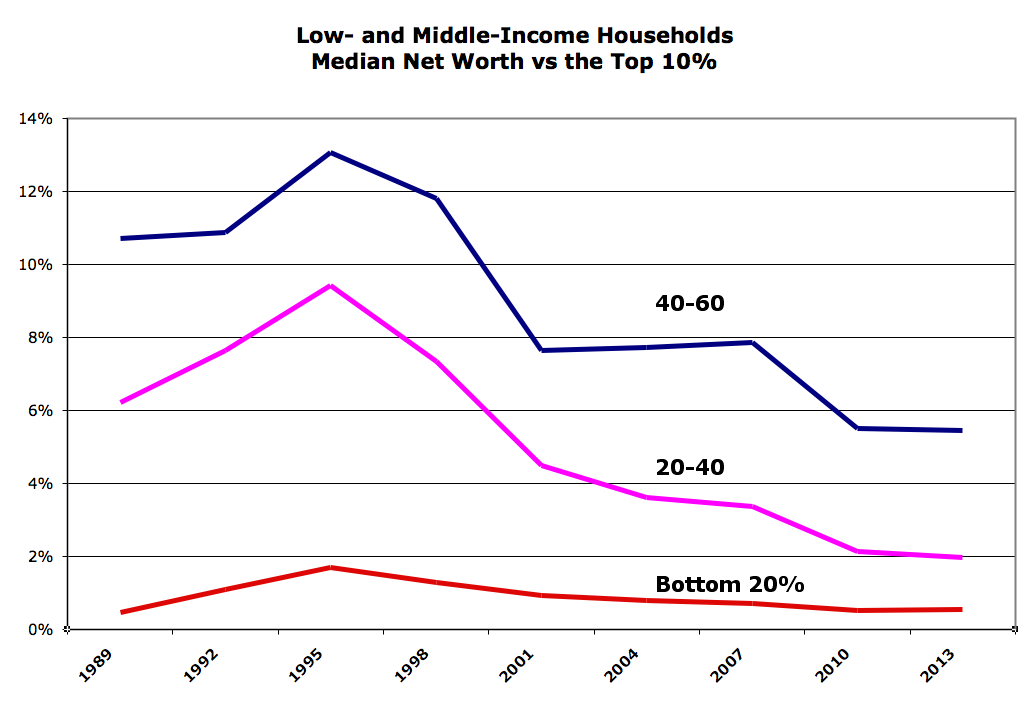

If you’re in the bottom 60%, here’s how you’re doing compared to the top ten:

I’ll say it again:

Widespread prosperity both causes and is greater prosperity.

We could all (collectively) be much richer right now, even as we could all be much richer.

A nod to income, and how it builds wealth: Say you’re a 50%er. Now imagine that in 2007, you and your friends were making $94,000 a year instead of the $76,000 you actually made. (That’s how much you would have made if wages had gone up with productivity — GDP per hour worked — since the 80s.)

Think we’d all be more prosperous?

Cross-posted at Asymptosis.

Why should wages increase with increased productivity?

The classic example is the farm-owner who hires a plowman. Let’s say a plowman can typically plow one acre per day. (That was the original definition of an acre.) Now, the farm-owner buy a tractor. The plowman can now plow TEN acres per day! Should his pay be ten times what it was before? Is he working harder than he was before? No. Instead of walking all day with a rather unpleasant view, he gets to sit with a much nicer view.

What he does get, however, is lower REAL prices (in terms of hours worked) for the food produced by that farm.

Let’s look at another simple example — ammunition assembly. With cheap single-stage presses, one guy primes the cases, another put the power in, a third seats the bullet, and a fourth crimps the bullet in place. But now the owner buys progressive presses, and each pull of the handle does all four operations (on different rounds, of course). Productivity increases by a factor of five. Should the employees be paid more? Was it their efforts that increased productivity?

“Should the employees be paid more?” = Should the employee be paid more?

You have improved throughput at the expense of Labor. One employee does the work of 4 employees, lowering the cost of Direct Labor, and with the increase in Capital. So yes their should be an increase in Wages; but, the increase should be based off of what?

@Jack: “What he does get, however, is lower REAL prices (in terms of hours worked)”

IOW, higher real wages.

Which pretty much answers your question, “Why should wages increase with increased productivity?”

Jack,

I wonder why we spend so much on defense? And why do so may Americans go hungry?

But I have always loved the “they now have washers and air conditioners” meme.

Perhaps I mis-phrased my rhetorical question. Allow me to re-phrase:

Why should hourly wages increase as much as hourly productivity increases?

You are quite correct. Real wages ARE increasing. The median size of a house is twice what it was in the 1960’s but people are not spending twice as much time working to pay their mortgages as they were then. Cars are more expensive, but they are safer and more fuel efficient, too.

“The median size of a house is twice what it was in the 1960′s but people are not spending twice as much time working to pay their mortgages as they were then.”

Gotta link showing that the present day “median” homeowner is working half as much to pay their mortgage as the median homeowner in the 60s was working to pay their mortgage?

Do we spend so much on defense, EMichael? In the early 1960’s, the U.S. government spent 50% on defense, and 20% on handouts to individuals. Those numbers are now reversed.

It would be nice if our allies stepped up so we could stand down. But after WWII, they had nothing. The U.S. had to provide the defense of Europe and Japan against the USSR and China. Since we were doing it, they chose not to even after they could afford to defend themselves.

If so many Americans go hungry, perhaps it is because they have been priced out of the job market by the Minimum Wage. When you increase the price of something, people buy less. This includes labor. When the dems took control of the House and Senate, they raised the price of unskilled labor. Those people whose labor was not worth the new price lost their jobs.

Now, you may say we need more government programs to feed the poor. I say we do not need such programs at all, because we have families, friends, food banks, churches, and other charities. If We The People are not donating sufficiently to meet the perceived need, then it is only because We The People don’t WANT to. If We The People are too stupid, ignorant, and selfish to properly decide how much to give to charity, then how can We The People possibly be smart enough, wise enough, and selfless enough to decide who will decide for us?

Well, so much for agreeing with you.

Don’t waste your time talking to me about SS and Medicare costs.

What you should do whenever you try to question our defense spending is comparing it to what other countries spend now, and in the past.

You are channeling Robert Samuelson(the lesser, or maybe the least), and that is a formula for disaster.

Dean Baker has a real answer for Samuelson and you:

“First Samuelson compares current spending at 3.4 percent to the post-World War II average of 5.5 percent of GDP. For most of the post-war period we were engaged in a military build-up to counter a rival super-power (the Soviet Union). The average also includes long periods of actual war (Korea, Vietnam, Iraq I and II, and Afghanistan). It should not be surprising that at a time when the country is not nearly as engaged in armed conflicts, and faces no major foe, it would spend less on its military.

Samuelson apparently wants the money for the military to come at least in part from spending on seniors, commenting at the end: “Democrats who will cut almost anything except retirement spending.”

The cuts to retirement spending that Samuelson wants are problematic. Social Security taxes are designated for Social Security. Samuelson might not have a problem taxing people for Social Security and then using the money for the military, but the public might have a problem with that idea, as would the people who depend on their votes.”

http://www.cepr.net/index.php/blogs/beat-the-press/would-history-have-judged-us-harshly-if-we-hadnt-invaded-iraq-in-2003?utm_source=feedburner&utm_medium=feed&utm_campaign=Feed%3A+beat_the_press+%28Beat+the+Press%29

E:

Your argument should be the ratio of Direct Labor to Total Cost. The Ratio times the Productivity Gain is the amount of wage increase to which Labor is entitled. If Direct Labor is 10% of the total cost (and more than likely it is), than 10% times the Productivity Gain. If 50%, than 50% times the Productivity Gain. Historically, Direct Labor has lost ground in Income. Make sense? Jack (not the Jack you know) and Arne will dispute this.

I thought Jack’s question was interesting, but I would rephrase it thus:

By what mechanism would you expect wages to increase as fast as productivity? In the example, by what mechanism would you expect the owner of the tractor to be required to pay the driver as much as the increase in productivity?

I would suggest that part of the answer is that the tractor driver needs to acquire skill in driving tractors. Nonetheless, the owner won’t invest unless he sees an advantage (profit), so wages going up a portion of the increase in productivity seems more likely.

Another part of the answer may be in the owner being able to sell more product. However, if the owner is taking domestic market share, then someone else is losing it. Otherwise, selling more requires exports. Does a period of wages increasing with productivity require net exports?

Arne:

Percent of Direct Labor to Total Cost or the ratio there-of.

‘Gotta link showing that the present day “median” homeowner is working half as much to pay their mortgage as the median homeowner in the 60s was working to pay their mortgage?’

No, because I did not make any such assertion.

The topic at hand, EMichael, is wage growth’s not keeping pace with productivity growth, and the increasing income and wealth gaps.

Jack

September 8, 2014 3:03 pm

‘Gotta link showing that the present day “median” homeowner is working half as much to pay their mortgage as the median homeowner in the 60s was working to pay their mortgage?’

No, because I did not make any such assertion.”

Y’know what you are correct. My mistake.

You said:

” The median size of a house is twice what it was in the 1960′s but people are not spending twice as much time working to pay their mortgages as they were then.”

Gotta link that shows median people are not working twice as much time working to pay for their house as they were in the 60’s.?

BTW,

Your minimum wage thing is beyond silly. I mean, seriously?

BTW,

One more codicil to your square footage insanity.

30 years ago I lived in an 800 square foot condo in Manhattan. I now live in a 2800 square foot house in Phoenix. As of today, that condo is worth at least five times my house.

Gotta love the idea that square footage without location means anything at all.

I can answer the question. The increased productivity of one worker leads to the displacement of other workers. The increase in salary produces a shorter work shift with higher pay in order to create work shifts for, otherwise, displaced workers. I understand that there are esoteric opinions of “money” but, to us worker class people, money is for exchange for necessities of life and goodies enjoyed in a prosperous economy. This is my offer on top other good suggestions.

For the most part, employers raise wages only if they have to, usually to retain workers or hire more workers.

> Gotta link that shows median people are not working twice as much

> time working to pay for their house as they were in the 60′s.?

Well, let’s look. In 1970, the median home price was $23,000. In 2010, it was $184,000. In 1970, median household income was $7559, and in 2010, it was $47,739.

Let’s assume a 10% down payment and a 30-year mortgage. So, in 1970, the average interest rate was 8.5%. In 2010, according to Freddie Mac, that was 4.69%.

So, in 1970, that’s a $183 monthly payment, or 29% of median household income.

In 2010, that mortage is $1041 per month, or 26% of median household income.

Sorry for the screwed up links. Moderator, can you please fix them for me?

OK, Jack

Now figure out how many hours the median family worked in 1970 and how many hours the median family worked in 2010.

The earliest hard numbers I can find are for 1976, which has 38.7 hrs /week then, and 38.2 hrs/week in 2010 per earner.

And while you’re thinking about it, two-earner couples (ibid) have only increased from 56.8% in 1970 to 59.9% in 2009.

Umm,

I need a link to your last total lie about the number if two earner couples cause it is a POS comment(you are starting to get embarrassing, whichever Jack you are)

And also remember this is about median families. Here is a detailed report about middle-income families(huge difference). Of course it only starts in 1979 and ends in 2006, but even you cannot think the change from 1970 to today is not greater.

“Work-family conflict is much higher in the United States than elsewhere in the developed world. One reason is that Americans work longer hours than workers in most other developed countries, including Japan, where there is a word, karoshi, for “death by overwork.” The typical American middle-income family put in an average of 11 more hours a week in 2006 than it did in 1979.”

http://www.americanprogress.org/issues/labor/report/2010/01/25/7194/the-three-faces-of-work-family-conflict/

The “ibid” means “it’s in the previously cited source.”

geez

“per earner.”

You are getting tiring.

BTW,

Give me some info(if you can) or take your best guess at how many median income earners actually have a mortgage at ” 4.69%.”

Why don’t YOU give me some info on how many median-income households even purchase a median-sized HOUSE? (Lower-income people tend to rent.)

Just a point of clarification. The Jack commenting above is not the Jack that often comments here from a more progressive side of the argument (at least in my opinion). I recall that there is also a JackD, but I do not think that Jack, above, is that Jack either. If there are going to be several commenters on this site with the name Jack there should be some mechanism for distinguishing between them. I’d like to lay claim to the use of just Jack on the basis of first use on the site.

Jack

September 10, 2014 12:58 pm

Why don’t YOU give me some info on how many median-income households even purchase a median-sized HOUSE? (Lower-income people tend to rent.)”

For identification purposes, this is the Jack with an IQ in double digits.

Why don’t I give info on this?

Cause you are the AH that tried, despite all evidence, to say that:

““The median size of a house is twice what it was in the 1960′s but people are not spending twice as much time working to pay their mortgages as they were then.”

Sorry, but when you state something, even something that no one in their right mind believes, I will give you the chance to prove your point.

Right now, you have proven that you have an IQ in double digits.

But, Rejoice!

You can only go up from the absolute bottom. So you have that going for you.

And you have presented absolutely no evidence to the contrary, Michael.

Not my job, pal.

You presented a scenario. You gave nothing that shows the scenario is close to being correct. Now you want me to do the work to show you are incorrect.

Now, anyone with an IQ in triple digits can figure out that you are incorrect using my admittedly incomplete information and facts. But you want more.

Step off, nut.

“Gotta link that shows median people are not working twice as much time working to pay for their house as they were in the 60′s.?. . .

“‘The typical American middle-income family put in an average of 11 more hours a week in 2006 than it did in 1979.’”

From the underlying source that eMichael cited, ( http://cdn.americanprogress.org/wp-content/uploads/issues/2010/01/pdf/threefaces.pdf ) it says, ” (Americans worked 568 additional hours in 2006 than in 1979; average assumes a 50-week year).” This implies a 22% increase in family hours worked.

This source ( http://ucdata.berkeley.edu/rsfcensus/papers/Working_Hours_HoutHanley.pdf) says: “Thus the trough-to-peak comparison pegs the increase in working hours at between 12 and 13 hours per married-couple family: parents spent an additional 13 hours at work in 2000 than their counterparts from 1975 had and adults in other kinds of married couple families worked an additional 12 hours.” which, off of a baseline trough from the same source of 51 hours for families with children, implies a 26% increase.

Maybe possible, but highly improbable based on the above, that someone identifies a source suggesting families are working twice as long in 2010 as they did in 1970.

From Table 13 of the Fed’s Survey of Consumer Finances (warning: 22MB excel file – http://www.federalreserve.gov/econresdata/scf/files/scf2013_tables_internal_real.xls ) the median family does not have a mortgage, nor does the average family in the middle income quintile (close to but not exactly the median). For those in the middle income quintile that do have debt, debt payments to family income, per Table 17, grew from 16.3% in 1989 (as far back as SCF goes), to 19.8% just prior to the crisis in 2007, but as of 2013 are back down to 16.2%.

Also keep in mind that the number of people per household has dropped (even as square footage has increased), by about 18% from 1970-2010: http://www.statista.com/statistics/183648/average-size-of-households-in-the-us/

As for median mortgage rate, Table C14a-OO of this link: https://www.census.gov/housing/ahs/files/ahs11/National2011.xls shows it at 5.3%, and I’m offering it because it was requested. But in the context of the comment thread, I’m not sure why 5.3% vs. 4.69% is relevant; the implication that somehow median households were able to come closer to the average mortgage rate in 1970 than in 2010 is offered without any rationale for why this would be the case.

Jed:

As taken from the 13 07 Alt Tab on your Fed Reserve Chart http://www.federalreserve.gov/econresdata/scf/files/scf2013_tables_internal_real.xls Alternate 13. “Family holdings of debt, by selected characteristics of families and type of debt, 1989–2013 surveys”

Percentile

of

Income % with Mort. Heloc Other Res Debt Credit Card Line of credit Ed. Loans Vehicle Loans Other Loans Other Any Debt

40–59.9 48.7% 6.9% 2.6% 54.8% * 16.6% 41.1% 12.6% 6.4% 83.8

Maybe I am wrong here; but, I am assuming those whose incomes are in the 40-59.9 percentile are equivalent to median income.

I cited government data which support my assertion. You have neither been able to refute the numbers nor to come up with any data which refute that assertion.

Average new home sizes are widely cited (usually NAHB is the source) to have doubled from 1970 – 2010. Median new homes constructed have increased 42% from 1973-2010. https://www.census.gov/const/C25Ann/sftotalmedavgsqft.pdf

But new construction doesn’t necessarily mean owner-occupied, and owner-occupied tend to be larger than statistical medians/averages for all homes.

run,

not understanding the point you’re trying to make. First, it’s not *my* Fed Reserve Chart, it’s the source of the charts for the OP. Second, the specific table you’re referencing is for 2007. Third, my understanding of the middle income quintile data cut is that it’s the average within that quintile (when looking at numbers like income, net worth, debt outstanding, as opposed to percentiles, which your specific table is referring to), rather than the median. And finally, the specific table you’re referencing, says 48.7% of those in the middle income quintile have a mortgage on their primary residence, meaning the median family does not.