How Do Households Build Wealth? Probably Not the Way You Think. Three Graphs

Work hard. Save your money. Spend less than you earn. That’s how you become wealthy, right?

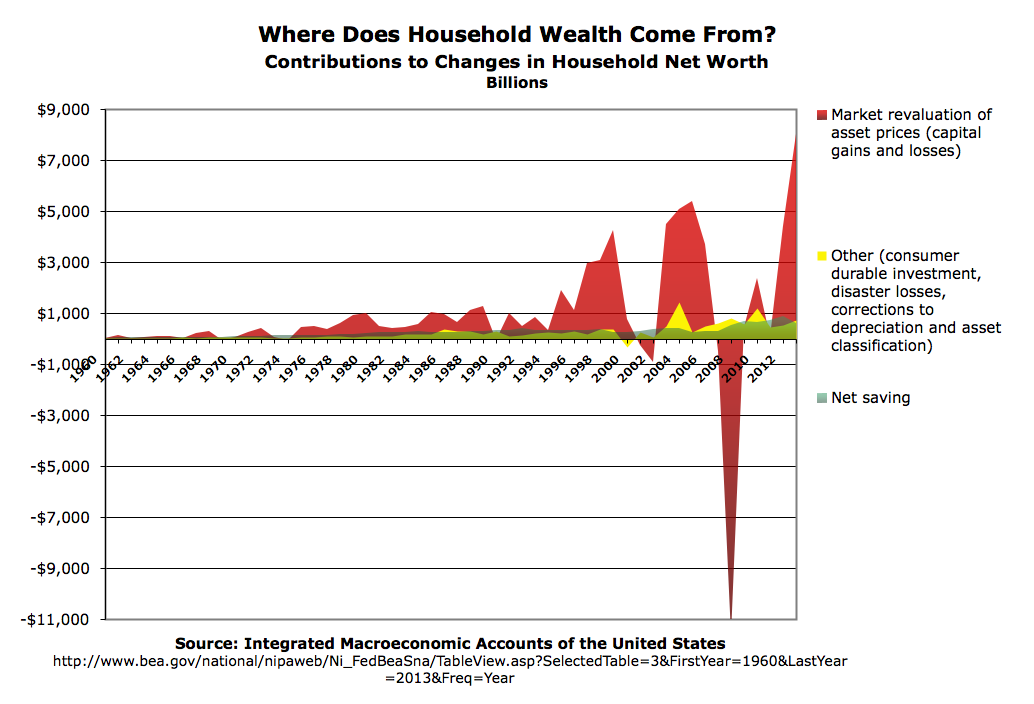

That’s not totally wrong, but if you think that’s the whole story — or even a large part of the story — you may be surprised by this graph:

(Note: these are not realized capital gains, which really only matter for tax purposes. If the value of your stock portfolio or house goes up for twenty or thirty years, you’ve made cap gains even if you haven’t “realized” them by selling.)

Household “saving” — households spending less than they “earn” — contributes a remarkably small amount to increasing household net worth. And that contribution has shrunk a lot since the 90s.

The accounting explanation is simple: “Income” doesn’t include capital gains; it comprises all household income except capital gains. So capital gains are also absent from “Saving” — Income minus (Consumption) Expenditures. (This is why HouseholdSavings1 + HouseholdSaving ≠ HouseholdSavings2 — not even vaguely close.)

The capital gains mechanism appears to dominate the ultimate, net delivery of rewards to household economic actors. Earning more and spending less is weak beer by comparison.

What does this say about our understandings of how the economy works? Does economists’ fixation with “saving” provide a useful picture of macro flows in the economy? Since asset ownership is hugely concentrated among the wealthy (even real estate), can we think about the economy’s workings at all without looking at distribution? Does this dominant mechanism allocate resources “efficiently,” or deliver the kind of incentives that make us all better off? And etc.

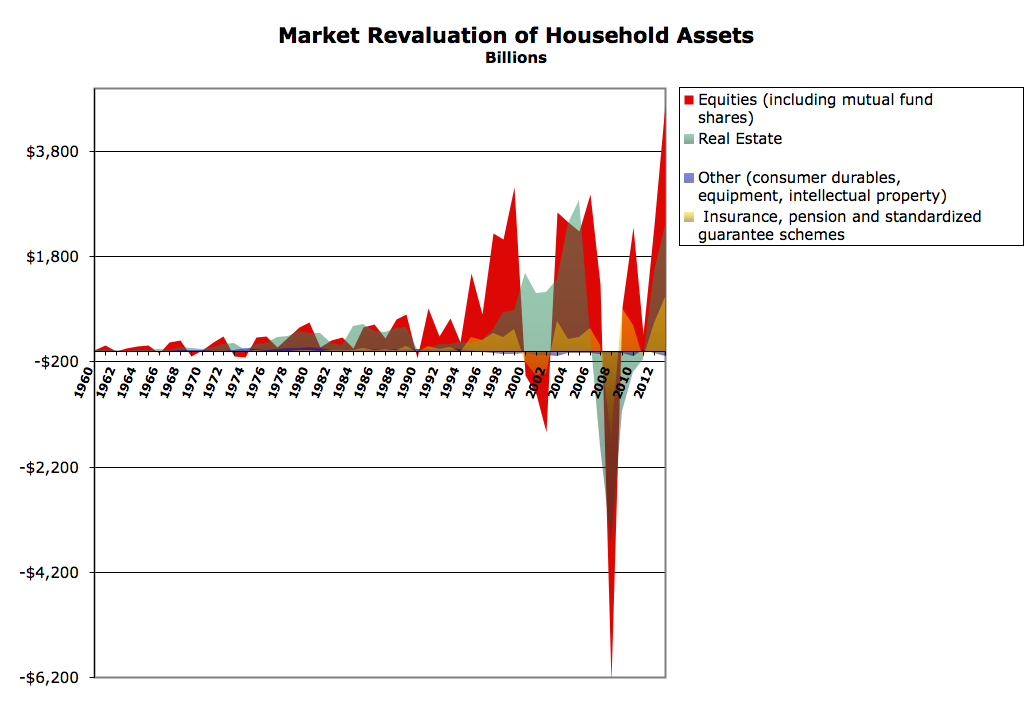

There’s much more I’d like to say about this reality, but I’ll just provide one more graph for the time being and let my gentle readers ponder the bare facts.

The spreadsheet’s here. Have your way with it. (It’s kind of messy; drop a line with questions).

Cross-posted at Asymptosis.

However to have capital gains you have to have some capital in the first place. So saving is necessary at the start to build the base capital for a down payment or in a retirement vehicle to start investing to get capital gains. Once you have some capital then capital gains are possible. But given the few folks that have an emergency reserve, then savings need to be pushed for this.

@Lyle: True, but many find that it’s best to earn that initial nest-egg the old-fashioned way: inherit it.

Zucman sez in US currently about 60% of wealth is inherited. (Up from circa 30/40% in the 60s?)

Walton heirs have circa $148 billion, it’s doubled since 2007.

Accumulating that initial nest-egg to get on the gravy-train cap-gains conveyor belt is getting harder and harder. Odds of any individual doing so are shrinking.

My wife and I are relatively well to do–not top 1% or probably even 10%, but certainly in the top quintile of wealth. She retired at 58 and I have been supporting the household without kids for the last 4 years and will likely pack it in within the next 12 to 15 months. At that point we will start drawing down our net worth which includes unrealized capital gains on our house and another parcel we own but 90% of our net worth is in deferred income accounts–which do contain capital gains but a lot of savings and employer contributions too and cash and mutual funds which were all started with after tax savings and the mutual fund capital gains are miniscule. Basically we have been conservative investors most of our lives and a lot of our savings grew based on interest returns and dividends rather than capital gains. We are not among the uber rich but we have accumulated a pretty good size pile of chips by saving a portion of our incomes for the last 40 years. Now it helped that for a lot of years we both worked, we both made decent incomes and we both worked for employers who contributed something to our 401Ks, but at the end of the day the biggest factor was did not lead the lifestyle that our incomes would have permitted.

Your title and first paragraph suggest that you have something to say to median workers who want to retire comfortably. Hopefully more than inherit it or you are out of luck. It is there, but you bury it by pretending that savings are not important.

A good retirement depends on putting it away and letting it grow. That means that instead of “spend less than you earn” being a small factor, it is a critical factor. A lot of people were bit because they thought that when they refinanced their house in 2005 they could spend more.

Income varies. Expenses vary even more. If average income does not exceed average expense, accumulation is a mathematical impossibility.

“If … accumulation is a mathematical impossibility”

Technically, I overstated it. Endowments produce income for expenditures and still grow, but the median worker does not have an endowment, so I will excuse myself.

@Arne and Terry:

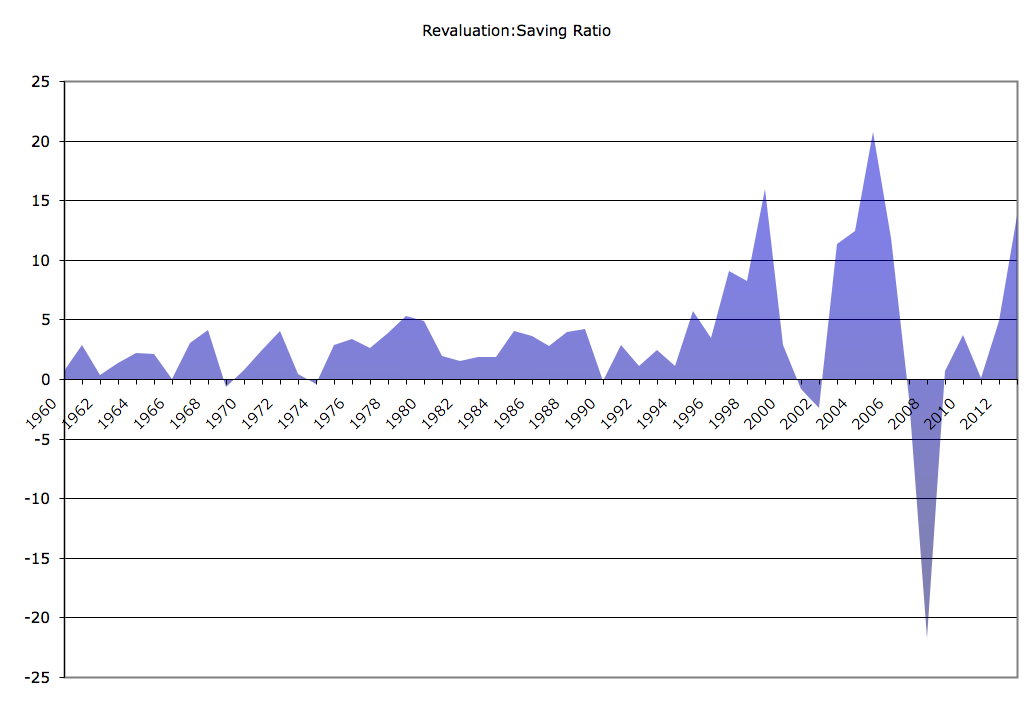

This is very much *not* advice for the median household. Rather, it’s depicting the financial mechanism through which most of our collective efforts are harvested. As the red areas in that first graph and the blue areas in the second graph expand, the rewards to hard work and frugality decline. Not a good thing, IMO, either morally or economically.

Arne said, in part, “…A good retirement depends on putting it away and letting it grow…”

…which assumes there is somewhere to put it away safely, and somewhere to put it where it will grow rather than shrink. It also assumes that the remainder will be sufficient for daily living plus some for emergencies … and that something of simple as a broken ankle won’t wipe out years of careful saving.

Like it or not, for many Americans their emergency and retirement “savings” aren’t bank instruments or other possessions, they are whichever government programs have evaded the axe.

Wasn’t it James Clavell who always stressed that no one gets their “fuck you” money from cash flow? I think this was one of his themes in Noble House.

This discussion brings to mind what I think is a conundrum regarding IRA’s and 401K type plans. If one has a 401K and is conscientious about the contributions, with or without employer contributions, do capital gains that such a plan is primarily based on become investment income once withdrawals begin. In other words, I put away $250,000 of my income over 30 years and it becomes $500,000 by the end of that term through capital appreciation. And possibly an additional $200,000 is accumulated in dividend accumulation over that same period. So the plan contains $250K of capital gains. I start to withdraw and there seems to be no way to differentiate between the gains made in that retirement account. So maybe I’m paying a much higher rate on the capital gains portion than I would have if invested in an other than retirement account. Am I seeing this correctly?

Isn’t the obvious here the fall in yields. I’m a bit uncertain here, but I think there are (for the US) three parts to the falling yields story:

1. Undervalued currency (making domestic real capital investment a poor bet)

2. Increasing leverage (or if you like decreasing equity), bidding up asset prices

3. Falling capital taxes (since that pushes up the price – see leverage as part of this story)