(Modern) Monetarist Thoughts on Wealth and Spending: Volume or Velocity?

I’ve bruited the notion in the past that “money” should be technically defined, as a term of art, as “the exchange value embodied in financial assets.”

In this definition, counterintuitively relative to the vernacular, dollar bills aren’t money. They’re embodiments of money, as are checking-account balances, stocks, bonds, etc. etc. Money and currency aren’t the same thing, and economists’ conceptual confution of “money” with “currency-like things” is central to the difficulties economics faces in understanding how economies work.

If this definition is safe, then the stock of money (I hate the term “money supply,” which suggests a flow) equals the total value of financial assets. Forget the endless wrangling about monetary base, M1, M2, divisias, and all that. Add up the value of all financial assets, and that’s the money stock. (There are certainly difficult measurement issues to discuss, but I won’t wrangle with those here.) People can exchange various financial assets for currency-like financial assets when they need to buy real stuff, but that’s largely mechanical; its macroeconomic effects are trivial.

In this definition “money” comes from two (or three) places:

• Deficit spending.

1. By government (federal — the sovereign “currency” issuer).

2. By private individuals and businesses (using loans from banks, which are chartered by government to create new money for lending).

#2 is of much greater magnitude overall, but it is also subject to big and fast periodic downswings (burning instead of printing money, when loans are paid off), which is much less true of #1.

• Animal spirits, a.k.a. confident optimism. When the market thinks that the total value of financial assets under-represents the value of the real assets they’re claims against, prices of financial assets are bid up, and there’s more “money.”

You could call this the wealth effect, and at least in the short- to medium-term — because it can happen so fast — the magnitude of its effects can overwhelm the first method. This change can go in either direction, of course — either creating or destroying huge amounts of money very quickly.

Jesse Livermore explains this mechanism elegantly and simply based on portfolio preferences. If the market wants 60% of its portfolio in stocks and 40% in bonds/cash, and more bonds/cash are issued, the only way for a rebalance to happen is if stock prices are bid up. (He’s got a great graph showing that very little new corporate equity is issued relative to the existing stock, often a negative amount for years on end.) If animal spirits decline (less confident optimism), the market wants less stocks and more bonds; the price of stocks — hence the stock of money — declines.

{kind=link}

• Trade surpluses. This doesn’t actually create money in the world (or an imaginary closed economy) the way the first two do. But if a country exports more goods than it imports, the payments for those net exports bring more money into the country. Trade deficits, the reverse. (U.S. trade deficits of $30-70 billion a year are pretty small change compared to the first two money mechanisms. Correction: That is a monthly figure, so the total is quite significant — 3-5% of GDP.)

The first two methods create money — exchangeable credits, or claims — “out of thin air.” And they destroy it when the debt from that deficit spending is paid back, or markets decide that underlying real assets aren’t so valuable after all. The government, the banks, and the stock market have both printing presses and furnaces.

And it doesn’t much matter how much of that money is embodied in currency-like things. If people want to spend more of their money one year (on newly produced goods and services, the stuff of GDP), the Fed will always accommodate their need for transaction cash; it must do so, or it can’t control the Fed Funds Rate because banks will be scrambling for cash and will bid up the rate. People don’t spend more because there’s a higher proportion of currency-like stuff around. If they want to spend more, there will be more currency-like stuff around; the Fed will ensure it. (At this point there’s a massive superfluity of such stuff, so the Fed controls that rate via its interest-on-reserves rate.)

Which all brings me to a simplified version of the monetarists’ equation of exchange:

(M)oney * V(elocity) = GDP (often designated as Y)

(Forget about PT or PQ; both T and Q are designated in imaginary, circularly-defined “units” of output whose logical coherence was thoroughly eviscerated in the Cambridge Capital Controversy. See the last paragraph of this section.)

If there’s more money around and velocity stays the same (i.e. people spend a certain percentage of their wealth each year), GDP goes up.

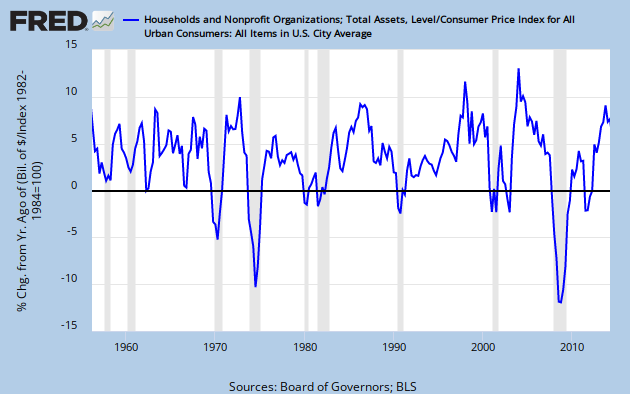

We see this clearly when we look at recessions and the year-over-year change in real (inflation-adjusted) household assets — a measure of households’ total claims on real assets, and a proxy for the “money stock” in this definition. (Note that in this measure the net worth of corporations is imputed to households who own their stock.)

Every recession (GDP downturn) since the sixties was preceded by a decline in this measure of the money stock, and every decline in these measure since the sixties preceded a recession (with one exception/false positive: 2011).

When people have less money, they spend less, and GDP declines, or grows more slowly. That is hardly a counterintuitive conclusion.

But what about V(elocity)? How has that played out over the years?

Another of those early-80s inflection points: velocity has declined from about 26% annual turnover of the mony stock, down to the high teens. If you’re looking for an explanation of that, you probably don’t have to look much farther than the spectacular concentration of wealth over the last three decades. Rich people spend a smaller proportion of their wealth each year than poorer people. So if wealth is more concentrated, velocity is lower. Arithmetic.

But there is another, related effect at play as well. A greater proportion of our real assets have been “financialized” (read: indebted monetarily) over the decades. The runup in student debt is an obvious example — whereby students have capitalized/financialized/indebted their most valuable real asset, their future ability to work and produce. They (in cooperation with their lenders) have created money — financial claims — based on those real assets (and given it to colleges).

This effect is very hard to measure because it’s essentially impossible to measure (in dollars) the value of our most valuable real assets — knowledge, ability, skill, organizational setups, legal structures, natural resources, etc. The relationship between total financial asset values and total real asset values is irredeemably opaque.

Bottom line: if GDP (and more importantly, GDP/capita) is to go up, either M or V has to increase.

Increasing M is problematic because either you increase debt (which obviously has its problems) or you (somehow) ignite animal spirits.

How do you increase V? It’s pretty straightforward: reduce the concentration of wealth so it’s more widely held, by those who turn over their wealth more quickly. Like, raise the minimum wage. Or institute a tax regime that actually is progressive, and use that money to provide for the general well-being by increasing funding for a plethora of well-designed programs like the Earned Income Tax Credit, jobs programs, wage subsidies, infrastructure and research spending, or guaranteed basic income.

At the very least, the goal should be to reverse the rampant radical upward distribution of the last thirty years, and the extreme decline in money velocity that has been the direct result.

Cross-posted at Asymptosis.