A study of Financial Repression, part 5… Sneaking into United States policy

The United States does not have the traditional type of financial repression where savers are household consumers who primarily deposit their savings in banks. And where borrowers are producer firms that primarily borrow at banks. These constraints apply mostly to emerging economies. The key with these constraints is to tie consumption to the return on savings and the cost of borrowing to bank lending rates. In the United States, households have access to a number of different saving options with varying return rates greater than returns on bank savings’ accounts.

Yet, the ultra-low Fed rate has opened up the door for financial repression in terms of savers subsidizing borrowers… To the extent that pension funds are reaching for yield to meet their return obligations. As well, workers are losing their pension funds as companies see that the pension funds are actually subsidizing borrowing. The companies do not want to save for their workers because they do not want to pay the subsidy cost of ultra-low interest rates.

Raising the Fed rate would help to support pension funds. But if the Fed rate stays low for years, many people will be put into extra hardship in their retirement years.

The US government would like to keep the central bank interest rate low. Tax revenues are at historic lows as a percentage of GDP. The government debt will rise as the boomer generation retires. The government debt is still quite large and interest payments on that debt are a concern. A low Fed rate in the style of financial repression would be desirable.

Yet, there are elements of financial repression in the United States…

- Low labor share has weakened household consumption, as financial repression is designed to do. But since households are not bound to low returns on savings at banks, a low Fed rate does not directly mean low consumption. A falling labor share accomplished in the United States what a low Fed rate could not.

- Asset prices (housing, stocks) are rising in the face of low consumer inflation. Asset prices benefit from low cost borrowing. This dynamic between inflation in asset prices and low inflation in consumer goods is how financial repression normally manifests.

- The Federal Reserve has an aggressive policy to inject liquidity into the economy. Yet, why is there no wage or consumer price inflation? Household consumers are not receiving the liquidity for consumption purposes. The money growth is not behaving as it would in a normal financial system. It is behaving as if there was financial repression, where the growth in the supply of money is transferred to borrowers at the expense of consumers… We end up seeing asset price inflation and not consumer goods inflation.

- Obama called for exports to lead economic growth. (source) And… a policy to increase exports benefits from the dynamics of financial repression, namely cheap access to funding and weak domestic demand. Suppressing domestic demand from low labor share and low interest rates raises national savings and lowers labor share costs in order to make US exports more competitive on the global market. There is a dynamic in the United States to simulate financial repression in order to boost export industries.

- The trade deficit is declining as financial repression in the United States intensifies. We see a report this week that “Exports are 17% above the pre-recession peak and imports are just below the pre-recession peak”. (source Calculated Risk)

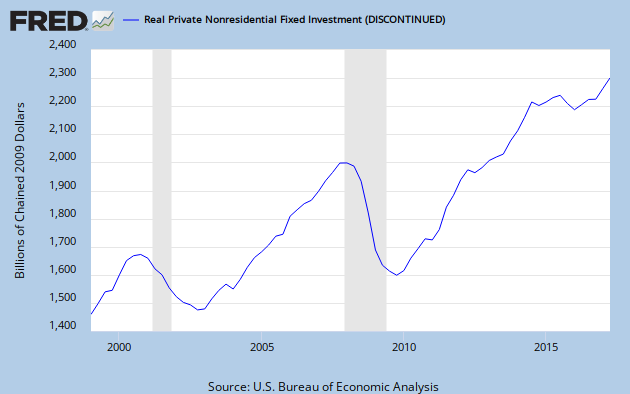

- There has been talk that manufacturing will make a comeback in the United States. The reason is that domestic demand is weaker, national savings are increasing and exports are getting more competitive. Business investment has actually been healthier than expected since the crisis. According to the following graph #1 (see part 2 of series), a positive transfer of funds from net-savers to net-borrowers began around the beginning of 2011. We have been in the area of financial repression for 3 years already. Real private nonresidential fixed investment grew most rapidly in 2011. (see graph #2, FRED chart)

Graph #1… Monetary policy enters the area of financial repression when line is positive. 2% seems to be a common limit on the positive side.

Graph #2… Real private nonresidential fixed investment. Increase in this investment matched interest rate policy entering the area of financial repression in 2011 (see graph #1).

{kind=link}

Graph #3… Imports slowed down and exports increased in 2011 in coordination with interest rate policy entering the area of financial repression (see graph #1). (source Calculated Risk)

- The economy is showing signs of heating up as we enter 2014. (source) The dynamics reflect real GDP nearing the natural level of real GDP. As I showed in part 1, when the central bank interest rate is kept low all the way to the natural level of real GDP, financial repression tendencies increase in intensity. My research shows that we currently have a lower natural level of real GDP (potential GDP) around $16 trillion due to a fall in labor share since the crisis. Keeping the Fed rate at the zero lower bound will increase the intensity of financial repression at the moment.

Could it be that the case for secular stagnation is simply a justification for keeping interest rates low and to have a policy of financial repression? It is a dangerous policy because domestic consumer demand would continue to be suppressed. This dynamic is tearing the United States apart.

Larry Summers gives 3 strategies for battling secular stagnation in a “financially sustainable way”… (source)

- “The first would emphasize what is seen as the economy’s deep supply-side fundamentals: the skills of the workforce, companies’ capacity for innovation, structural tax reform and ensuring the sustainability of entitlement programs. This is appealing, if politically difficult, and would make a great contribution to the country’s long-term economic health. But this approach is unlikely to do much in the next five to 10 years. Apart from obvious lags like those in education, our economy is held back by lack of demand rather than lack of supply. Increasing capacity to produce will not translate into increased output unless there is more demand for goods and services.” … Sound familiar about lack of demand if production continues to increase? That is one of the manifestations of financial repression.

- “The second strategy, which has dominated U.S. policy in recent years, is lowering relevant interest rates and capital costs as much as possible and relying on regulatory policies to ensure financial stability. No doubt the economy is far healthier now than it would have been in the absence of these measures. But a growth strategy that relies on interest rates significantly below growth rates for long periods virtually ensures the emergence of substantial financial bubbles and dangerous buildups in leverage. The idea that regulation can allow the growth benefits of easy credit to come without cost is a chimera. The increases in asset values and increased ability to borrow that stimulate the economy are the proper concern of prudent regulation.” … This strategy seeks to manifest financial repression while recognizing the dangers of bubbles and leverage. Still, he wants asset values and subsidized borrowing by savers to stimulate the economy. He is calling for financial repression.

- “The third approach — and the one that holds the most promise — is a commitment to raising the level of demand at any given level of interest rates through policies that restore a situation where reasonable growth and reasonable interest rates can coincide. To start, this means ending the disastrous trends toward ever less government spending and employment each year and taking advantage of the current period of economic slack to renew and build out our infrastructure. If the federal government had invested more over the past five years, the U.S. debt burden relative to income would be lower: allowing slackening in the economy has hurt its long-run potential. Raising demand also means spurring private spending.” … He recognizes the weak domestic demand that has occurred due to a fall in labor share. Yet, he calls for more government spending and investment in infrastructure. He blames the government for allowing demand to fall. Yet he doesn’t seem to realize that it was business that lowered the labor’s share of output. This strategy again shows a hidden agenda of financial repression. Low interest rates from the central bank will implicitly lower the government{s debt burden and allow it to spend more. A low Fed rate will also keep infrastructure development cheap.

At no point is Larry Summers offering direct support for household consumption. He is actually cloaking an agenda to make saving households and pension funds subsidize investment and government spending. His Trojan Horse is hiding financial repression.

China at the moment says it is implementing a plan to increase domestic consumption. (source) The plan is actually intended to reverse the policy of financial repression, because the policy is reaching its point of collapse and instability. Investments have been seriously mis-allocated during their tremendous period of financial repression. China is currently allowing payments on bad debt to be put off until next year. This is not a good sign. China is on the verge of a major slow-down.

If we are finding financial repression as the answer to our problems, we have fallen into the trap that China has set up for us. By trying to compete with China, we are becoming China. We are converging with them into a policy of financial repression, even though our form of financial repression is different.

Financial repression is a policy that heads in the wrong direction. Financial repression simply and ultimately leads to a grand instability. Let China experience the grand instability, but not the US. Instead of making borrowing ever cheaper as a solution, we must return to an interest rate policy of economic balance. This means raising the Fed rate so that the real current interest rate is in line with the natural real interest rate.

The Fed rate should at least be over 2% at the moment in order to have economic balance.

Yet, the real danger comes as real GDP closes in on its natural level. The market will start driving interest rates higher, and the Fed will have to tighten policy quickly.

I realize Charles Plosser, President of the Philadelphia Fed, has always had an instinct that the ultra-low Fed rate was risky. Others do not seem to take him seriously. He has searched for models to explain his instinct. But he is very concerned that the Fed rate will have to rise quickly. (source) He knows that market pressures can force the Fed to respond with a higher Fed rate. He does not want the Fed to get too far behind the curve, but the Fed has gone too far behind the curve. I share Plosser’s concerns.

To close this 5-part series on financial repression, I would simply say… Wisdom dictates that we should not follow a strategy of financial repression going into the future, in whatever hidden or altered form it may manifest. The US must keep the current real interest rate in line with the natural real rate. And that means raising the Fed funds rate.

Links to…

Part 1, a basic model…

Part 2, looking for evidence in the US…

Part 3, How financial repression manifests…

Part 4, problems…

It appears that there’s a growing recognition of the problem in the UK and Japan. Here in the US , not so much :

“….John Cridland, director-general of the CBI, Britain’s biggest business lobby group, will criticise many of the 240,000 companies he is paid to represent for failing to pass on their new-found prosperity to employees….”

http://www.theguardian.com/money/2013/dec/30/pay-workers-more-cbi-firms

“Japanese Prime Minister Shinzo Abe has urged companies to increase wages faster than gains in the cost of living, a part of his grand strategy to break decades of deflation in the Japanese economy….”

http://japandailypress.com/japans-pm-abe-pushes-for-wage-increase-toyota-and-hitachi-pledge-to-help-0940624/