Can the yield curve invert by the next recession?

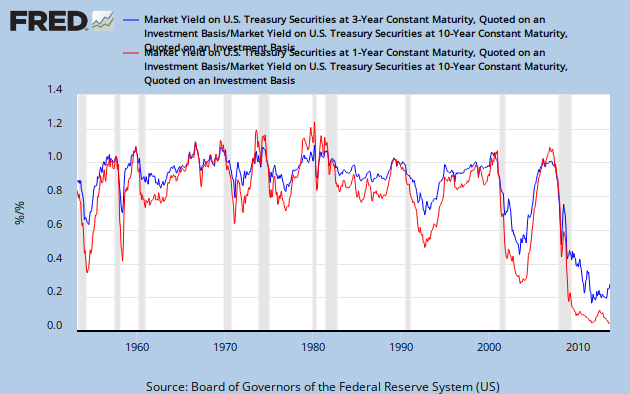

Many people look for an inverted yield curve to signal a recession. The track record is good. The yields on longer term maturities decline in relation to shorter term yields. Let me show a version of the inverted yield chart that I haven’t seen anyone do yet.

I take the 3-year Treasury constant maturity rate and divide it by the 10-year Treasury constant maturity rate. Then I take the 1-year Treasury constant maturity rate and dived it by the 10-year Treasury constant maturity rate. (quarterly data)

{kind=link}

When both of these lines go above 1.0, the yield curve is inverting and a recession is coming into view. It has been a fairly reliable chart to signal a recession.

The lines are very low at the moment because the Fed rate is near the zero lower bound. It is unlikely that shorter term rates will rise much. The Fed is in a labyrinth and cannot find the exit from the zero lower bound. They are concerned about financial stability… and just tapering of QE creates an apparently “unacceptable” level of instability.

In a normal world, the two lines in the above chart would have already started upward. We no longer have a normal world.

The question is whether a recession can start without having an inverted yield curve. Even Wikipedia connects the two in absolute terms…

“Since the financial crisis of 2007–2008, the U. S. Federal Reserve has maintained a zero interest-rate policy (ZIRP) for an “extended period of time”, where the short term interest rate is practically set to zero. Therefore a recession is unlikely to occur until this policy is reversed.“

Interesting statement. Wouldn’t it be nice if we could just maintain a zero interest rate policy and never have a recession?

In order for the yield curve to invert this time around, longer term rates would have to come down to almost zero. Normally the shorter term rate would rise before a recession, but policy will keep shorter term rates near zero as far as the eye can see. The 10-year rate did go down below 2% in 2012. Can it go further down? Actually it could… But all the way to a zero lower bound? It’s wild to think about that possibility.

It seems reasonable to assume that the yield curve will make an attempt to invert before the next recession, but a complete inversion would require the Fed to raise its overnight interest rate. The Fed is forecasting a rise in the Fed rate in 2016. So maybe the implication is a recession as far out as 2017 or 2018.

Edward, can I ask a couple things, as a curious “civilian” (untrained economist fan girl?)

— Do you have to come out of a recession, in order to go into recession? It appears we are in a sort of permanent recession, so can we go into a deeper recession, or just stay in our current doldrums?

— It looks like our latest, deepest, awfullest recession was only possible because of the Bush Bubble re inflating a stagnant economy. So, would we need yet another bubble in order to get enough height to dive into another recession? I can’t think of anything else that would inflate the economy enough to permit another collapse.

— Maybe I am missing a point here, but it looks like future bubbles and collapses will have to be the pastime of the wealthy, since the rest of us have not much to contribute to inflating things.

Stray thoughts, hope I am not too far off track.

Noni

Noni,

We are not in a recession. The economy is trying to deal with international imbalances. As such, the economy has fallen to a sub-optimal level. We are in a normal business cycle, but only at a sub-optimal level. People call it a recession because it is not optimal.

We actually do have to recover from a recession in order to go back into a recession. But we have already recovered… sub-optimally.

We have bubbles forming now. There are bubbles in other countries too that are attracting investment dollars.

Interesting thought about recessions as the pasttime of the wealthy. But we need to realize that the wealthy do not want a recession. They lose a lot of money and do not sleep. Recessions are very stressful for them. Many have to declare bankruptcy.

The real problem is that the wealthy are too short-sighted on profits. After the crisis, the rich began to say… “now we have to get rich more slowly.” They started to see investment as long term slow growth… but there is still so much pressure to make quick profits. China has a big problem with that now.

Thank you. By the way, I used the word “pastime” as a rather mordant joke. But really, who’s going to lose money in an economic downturn except those who have it?

A blog post the other day detailed how the wealthy live in a gated kind of situation, where their incomes are safe and growing but they seldom meet the struggling 90%, so they have no clue about their lives.

I am in rather the reverse situation, since most of the people I know are either struggling to stay afloat, or have gone under in one way or another. I really must broaden my horizons, if I can find any rich people who would let me hang out with them. 🙂

It depends by “struggling to stay afloat” means. People in 2005 and 1995 were struggling to “stay” afloat. Nobody in my family is struggling to stay afloat and we are not by nature, “wealthy” people.

You sound like one of those econ-blogging bears that overuses/misunderstands stats and trys to intellectualize their family as ‘struggling’.

Yes, the yield curve will invert, as the expansion has a long way to go sans a external shock. We aren’t even to the “gravy” period yet. When the real asset bubble begins.

John,

Why do you use slogan when defining ‘struggling to stay afloat’ when criticizing in comments for the same thing?

Hey John, I would be interested to see your checklist of things that qualify a person as “struggling.” I shall await your reply with bated breath.

I received a message that Japan’s yield curve did not invert before its most recent recessions. I have not seen the data on this yet.

“Yes, the yield curve will invert, as the expansion has a long way to go sans a external shock. We aren’t even to the “gravy” period yet. When the real asset bubble begins.”

You’re making the rather dangerous assumption that the economy did not undergo a regime shift. Additionally, as Mr. Lambert just stated, Japan is a country which has gone through recessions without an inversion occurring.

There is no precedent for current monetary conditions so I doubt that the yield curve contains much or any information. If the curve does or doesn’t invert before the next decline in GDP will be relegated to an historic footnote.

Do rates actually even contain information any more? I suppose they do but but it isn’t market information. Using the term market that implies one that is essentially free not the managed thing we have now.

What Rapier said.

It is impossible to have an inverted yield curve when short term rates are zero. Negative interest rates are never seen.

The reason that rates are so low, both short and long, is that the Fed is “buying” approx. 70% of newly issued debt. How long this can continue is not known.

Since John hasn’t had time to make up a “struggling” checklist, let me give it a try:

— a grandmother working four part-time jobs in order to pay off her little house and stuff away as much savings as possible because after fifty years working and raising a family, she has no pension or health care coverage

— a 52 year old man, a skilled technical professional, who lost all his 401k retirement savings, and his job, and health coverage in six months when the recession hit. He found a new job last spring, but had to live in a homeless shelter for four months (while working) before he scraped together enough money to rent a room in a lady’s basement

— a 60 year old Air Force veteran and technical professional, survivor of two major heart attacks, who lost his job after the second heart attack, all his possessions and savings, and returned to school to take a business degree a year after his quintuple bypass only because he could do that on the GI Bill. He’s in trouble now, because after two years on the honour roll he has had to drop out of school (losing his GI support) due to stomach cancer

There, is that struggling enough for you? And these aren’t random people I happen to know, they are my two brothers and a sister-in-law.

Noni

Interesting looking at the comments nearly 5 years later. No inverted yield curve yet. I just started researching this topic. One article showed the drop in stocks over the last 6 decades prior to and during a recession and what’s most interesting is the ones of late have dropped in the 50 percent range while earlier recessions recorded less than a 20 percent drop. I often see the financial “system” as a means to redistribute wealth from anyone that is close to any sort of wealth to those that are beyond wealthy. It doesn’t seem fair anymore. I also wonder why the 401K which requires investing knowledge would be a good idea for a retirement system? It is an awful idea to put ordinary people up against a casino (ordinary people are going to buy certain stocks and funds for bad reasons). Most people haven’t any interest in finance/investing, because it is just so complicated. The whole system is ripe for ripping people off. Eventually, the US as a whole will pay for ever having a 401k system – lots of very poor people in the future which it seems our politician and ruling elites want.

By the way, since I’m very interested in finance over the last decade, 401k has served me very well, but only after I became very interested.

Welcome to Angry Bear. First comments always go to moderation to weed out spammers and advertising.