A “Wild and Dangerous” Scheme, Part Two: What’s “fixed” got to do with it? Do with it?

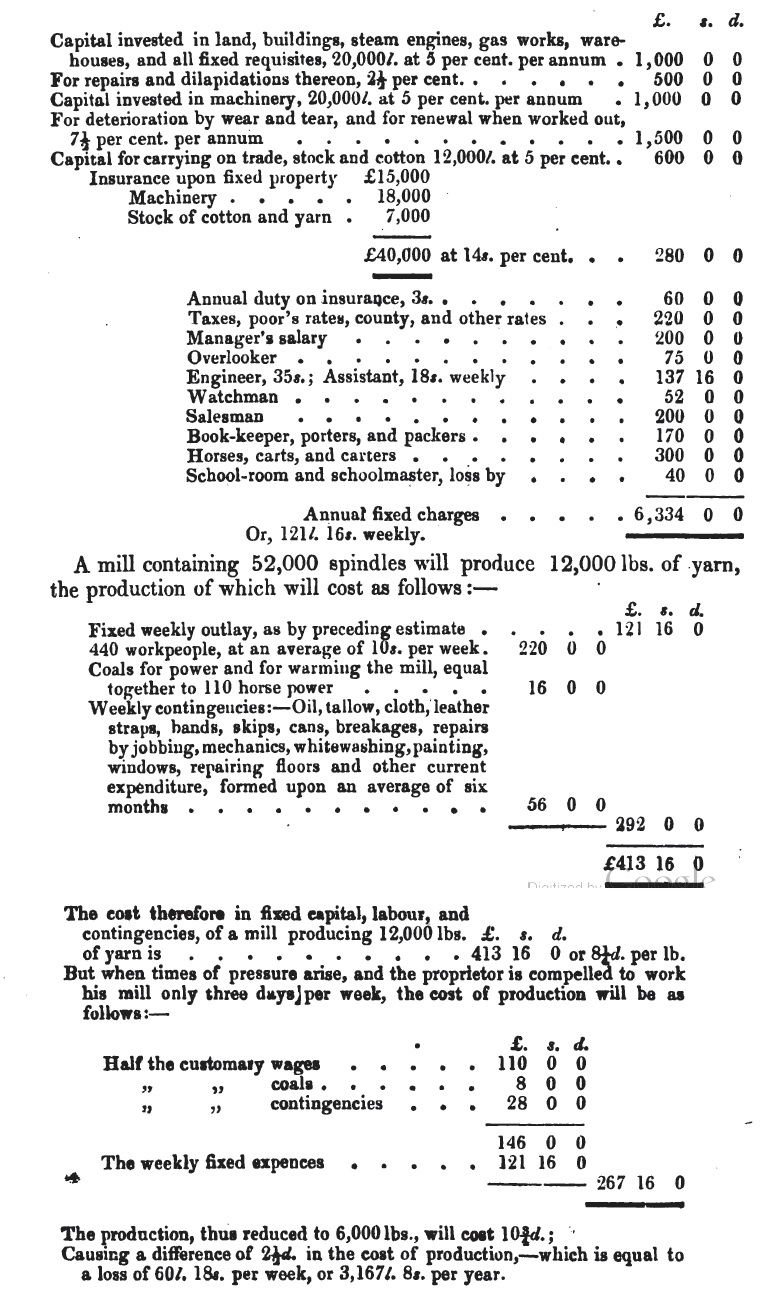

“…we have seen a calculation… which shows that the fixed charges, for machinery and the general management of a mill, are as nearly as possible equal to the cost of wages in the process.”

In my earlier post on the “Wild and Dangerous Scheme” I teased the “egregious accounting error” committed by the author of the 1844 article in the Economist. In plain terms the error was double counting — the author deducts 16.5% from wages to compensate for a decrease in output and then attributes a second loss of 16.5% to the decrease in output resulting from it’s effect on “fixed charges.”

That double-counting error seems self-evident to me but there is also a semantic smoke screen at play that obscures it for some readers. The term “fixed charges” seems to refer to an immutable absolute quantity of costs and — implicitly perhaps? — an unalterable production process. It doesn’t. It refers to accounting entries, as the term “charges” indicates.

The fact that these charges are independent of output doesn’t mean they can’t change or can’t be changed. Machines could be bought or sold. Inventory levels could be raised or lowered. Insurance rates or taxes could change. Most importantly for the current example, the elements of the production process could be permanently altered thus requiring a reconfiguration of those “fixed” charges.

The double-counting error in the 1844 article is perhaps best illustrated in the case of a Six-Hour Bill instead of a Ten-Hour Bill. Instead of reducing the workers’ weekly wage to zero, the employer could simply cut their wage by 50% and hire a second shift to maintain output at full capacity. By the same token, a reduction from 12 hours to 10 hours could be met by hiring more workers to make up the lost output or by employing some combination of new machinery and additional workers. This is, of course, granting the author’s assumption of a constant output per hour worked.

What does “fixed” even mean? Could it mean fixed per unit of output? Fixed per employee or per hour worked? Fixed per longer unit of time, such as a year — or 15 years? Never changing? It could mean any of those. Whether it does mean one or another is a matter of fact or convention. Sometimes the convention is not what you might want or assume it to be.

Are raw materials a fixed cost? Common sense might suggest that reducing the output of cloth by 1/6 means that only 5/6 as much cotton will be needed as input. Not a fixed cost? But what if the accounting convention specifies a given inventory of cotton regardless of how much is actually used in a week? Are interest rates “fixed”? They are and they aren’t!

When an accounting error is obscured by a muddled allusion to fixed charges, the temptation may be to try to “make sense” of the author’s argument — to give the benefit of the doubt that the author may be wrong but not incompetent or deliberately deceptive — in effect, to excuse the bad accounting by virtue of the muddled semantics. Wildly and dangerously enough, though, in the case of the 1844 Economist article, I happened to stumble upon the receipts: the calculation which that article’s author refers to having seen.

As it turns out, the “fixed charges, for machinery and the general management of a mill,” were not “as nearly as possible equal to the cost of wages in the process.” They were more nearly equal to the cost of wages of a mill operating at half capacity and thus paying half wages! We now confront three problems with the argument — double counting, semantic muddling and misrepresentation of a source.

Interest rates are not fixed costs.

The cost of financing (maintenance of outstanding debt) is.

Taxes aren’t fixed, but some sorts of taxes are more generally unavoidable and therefore fixed. You pay as long as you own the building or the inventory. The cost of “keeping the lights on” is fixed, but the fuel needed for production isn’t.

From a management accounting perspective, fixed means independent of output within a window of output, and not obviously driven by another factor that varies with output.

From a cost accounting perspective, fixed could be anything not on the routing or bill of material, but the routing would implicitly have certain sorts of costs that are “fixed” included as well, for instance annual medical/dental insurance which varies based on headcount but not output.

As I interpret Ashworth’s fixed charge of 5% per annum on capital invested, it is what we would call the opportunity cost of the investment in terms of the alternative of a risk-free return.

It is worth mentioning that double counting is often the symptom of an attempt to bridge the gap between two distinct accounting entities. The author’s wage/hours/output calculation may be wrong but it is logically coherent. But the wage/hours/output/enterprise’s fixed charge calculation is not logically coherent because the hours worked and wages received are due to one entity and the fixed charges are capital’s business. The workers are under no moral or contractual obligation to make up for management’s failure to manage.

Here I was about to make clear that Sandwichman deserved all the credit for finding the error in the 1844 argument. But the error was that the “logic” of 1844 left out the fact that by replacing the “lost” worker-hours by hiring more workers, there would be no loss in production, the “fixed costs” (whatever they are) would remain fixed, total labor costs would remain what they were, and the only change would be that workers would receive a lower daily pay, at the same hourly rate, to reflect the shorter work day.

I believe that Sandwichman is confused by all he knows about economics and manufacturing. Those things are probably true and probably do account for the fact that in the real world the “wild and dangerous scheme” of cutting worker hours does NOT result in the catastrophe that 1844 “logically” predicts.

But in fact those real world and economics theory world “facts” have nothing to do with the argument… the false argument… that 1844 presents.

I don’t expect I will get anywhere by pointing this out, except possibly to make Sandwichman angry at me because he thinks (wrongly) that I am dissing him. I am only pointing out that neither “logic” nor “facts” can be trusted… either to arrive at truth, or to convince others of truth. In this case it was a missing bit of “information” (a fact or at least a proto-fact) pointed out in the first place by Sandwichman, but not made very clear in the midst of the other facts and theories he was throwing at the problem.

By all means continue discussing the theoretical and real world reasons why the “wild and dangerous scheme” argument turned out to be wrong, but try not to get tangled up in the weeds. The “simple” fact is that it was wrong because it (probably deliberately) left out “the rest of the story”.

This is important because it is the usual trick that political writers and political economists use to mislead their readers.

Their target readers don’t know the ‘”theory”, won’t understand it if you try to tell it to them in a few words or less, and won’t care because they have their own theory of everything which they adapt their “facts” to.

I’d like to believe that by cleaning up the argument I made it easier for people (me at least) to understand what was wrong with it, but I can’t claim I would have succeeded if Sandwichman had not pointed out the “fact” of the missing worker-hours being fixed by simply hiring more workers. But “in fact” I am reasonably sure that I won’t convince anyone else, they having their own theory of everything that works for them.

I don’t know why I should be angry with you, coberly. You have a different way of framing the problem. On the other hand, I don’t agree that my way of framing the problem makes it “unclear” just because you find it harder to follow than if I had framed it the way you do. When I read your comments, I get the impression of an extra, unnecessary step. That may be because having dealt with exactly this kind of double-counting problem several times I have come to realize that this “additional step” is already embedded in the accounting error. The first time I encountered this type of problem was over twenty years ago with overtime “premiums” — that are also penalties. The second time was with “quasi-fixed” employer-paid benefit costs. The third time was with the Cobb-Douglas production function being used to demonstrate the OPPOSITE of what it assumed. Then there were multiple sightings of economists invoking a “fixed amount of work” wages fund doctrine to “debunk’ an alleged fixed amount of work lump of labour. Again, Kaldor-Hicks compensation principle commits the error and finally there was a hilarious specimen of double counting performed by George Armstrong relating to the 1871 engineer’s strike in Newcastle. Having seen the problem again and again and again, I don’t need to go through the extra step once I have seen the pattern. And having explained the problem over and over and over again, I am not persuaded that going through that extra step will make my explanation clearer to the reader.

“proto-facct” not “photo-fact”

oh, hell. fact, not “fact.”

ah, spell check again. not ” f a c c t “, ” f a c t “.

Sanwichman

there is the problem: you know too much. you may not need to take that extra step to understand the cheat, but your readers probably do.

that’s why you have to explain the problem over and over.

what leads to error, as well as brilliant insight, is that the human brain makes leaps entirely supported by “what we know” that leap over what we don’t know.

that said, my finger counting approach to problems does not seem to be any more convincing than your “what i know” approach.

(and, that said, part two: i looked at the problem you stated: an 1844 essay that “saw a calculation” that showed “a wild and dangerous scheme”.. how cutting hours would cut wages twice as much as anyone expected. i addressed THAT problem…the 1844 argument, not the whole “shorter day” argument or all the false double counting arguments you are aware of. just tried to make the 1844 argument clear enough to examine on its own terms. which just cleared the way so that when you mentioned .. in passing.. what was wrong with it … the answer was immediately clear.

and i’d bet, even given my none too inspiring experience with trying to teach undergraduates, that if we each took a class of undergraduates and you explained to yours your way, and i explained mine my way, i’d get more of them to understand the fallacy than you would.

just a friendly bet. no rancor. no “i’m better than you are” implied.

That is what I was just trying to say. I’ve done it the finger counting way and gotten as much “huh?” If I had a solution to the communication problem, I would use it.

oh, as far as your being angry or not, it has been my experience that i make people angry even when i don’t intend to, or think i am saying anything that they should get angry about. so i worry about it. glad to see you are better than that.

Sammich

too true.

i don’t have the ability to insert my replies directly after the comment i am replying to.

in general, i think that framework.. insertion… is more difficult to follow than just posting comments as they come in. i can skip or fast read comments until i get to one that replies to me, and then answer at the bottom of the queue in my turn, than i can go back through a whole comment thread checking for any that may have appeared…

may be hard to follow this… it’s a question of reading “what’s recent” since the last time i was here, against “checking everything since the beginning…”

don’t know why but “that” for “than” seems to be a very persistent typo… in other people’s comments as well as mine.

In that spirit, coberly, here is a reply to a question you asked in the previous post about a useful measure of national income — not so much a change of subject as you might suppose. Roefie Hueting worked with Jan Tinbergen developing the “Sustainable National Income” account, which tried to take into account environmental costs or — “externalities” as economists might say. Hueting proposed the concept of “asymmetric entering” for things like natural disasters or resource consumption. The idea being that conventional national income adds to the account for the expenditure but doesn’t subtract for the damage or depletion.

One can also view this as a companion to the double counting problem. Essentially, the income accounts are dealing with two entities — nature and the economy — but treating it as if it was a single entity. The subtraction on the nature side can be ignored because it isn’t part of the economy. Households are treated similarly. Their contributions in terms of income and product count but their intermediate inputs of household work etc. are ignored. Note that while the Economist author talks about “fixed charges” of capital, he makes no mention of the overhead costs and wear and tear of the workers. Rent consumes half of the workers wages? Suck it up, workers!

I don’t know how to explain this but a double entry error can also be considered an asymmetric error “turned upside down.” When 1844 reduced wages by 16.5%, he failed to INCREASE the employer’s “wage fund” by the same amount. Thus when he subsequently looked at the effect of a decrease in output on fixed charges, it appeared to be uncompensated. In fact, it had been compensated by the unacknowledged increase in the proverbial wage fund!

Sandwich

I hope you can develop your approach to where it starts making a difference with the people who get to make the decisions that affect our lives.

I have always had trouble understanding national income accounting: what it was for. Quite as bad as “inflation” which at least the people who want to destroy Social Security by using a “more accurate” measure have demonstrated is a political construct as much as an “economic” one. No doubt inflation since the stone age has not been as high as recently reported…. if we only still lived in caves and ate leftover lion dinner. or, looking ahead, if we don’t count the cost of keeping “connected” in the future as that would clearly be an improvement in our standard of living as opposed to a “cost of living” in the future.