Interest rates: no shift in the economic weather yet

Interest rates: no shift in the economic weather yet

I wanted to make two comments about what has been happening recently with interest rates, a short term look and a long term look.

Today let’s discuss the short term.

Since September, long term Treasury interest rates have risen from roughly 2.1% to 2.8%. The two year Treasury yield has risen from roughly 1.3% to 2.1% — which means that for the first time in years, the 2 year Treasury is giving you more in interest than the dividend yield from holding the S&P 500. So, not only will interest rates presumably slow the economy, in terms of income they are now a *relative* bargain compared with holding a wide index of stocks.

Now, I don’t pretend to know where interest rates will go from here over the short term. Whether long rates rise over 3% or fall back under 2.5%, I don’t know. But let’s assume that over the short term they stay roughly where they are now.

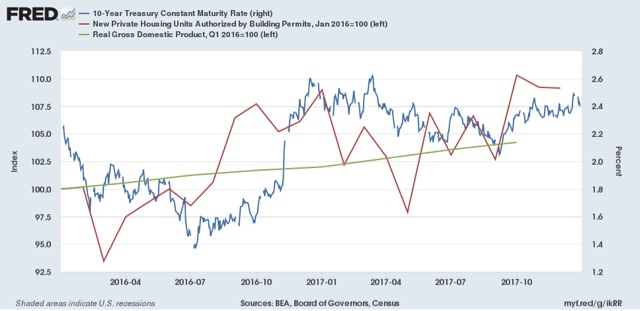

An upward spike in interest rates has happened twice in this expansion. Most recently, rates spiked from under 1.5% in mid-2016 (thank you Brexit!) to 2.6% following the US presidential election (blue in the graph below). Here’s what happened with housing permits (red) and real GDP (green) in the year following that spike:

Permits stalled for most of 2017 before turning up, while GDP also paused before continuing to advance.

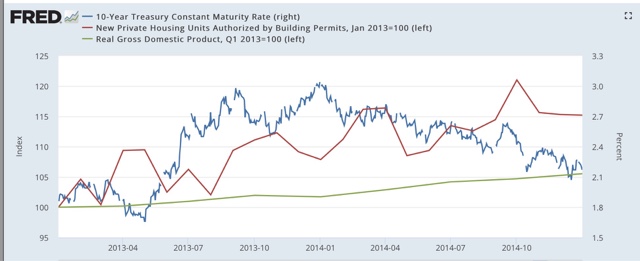

Next, in 2013 we had the “taper tantrum,” during which long term interest rates rose from 1.6% to just over 3.0%, before fading to about 2.2% by the end of the next year. Short term rates stayed just above zero. Here’s the same graph showing what happened in 2014:

Permits slowed but never completely stalled, while real GDP did turn slightly negative in Q1 2014 before continuing to advance.

So far, interest rates have not broken out the type of range that led to brief slowdowns, but not a downturn, in the economy.

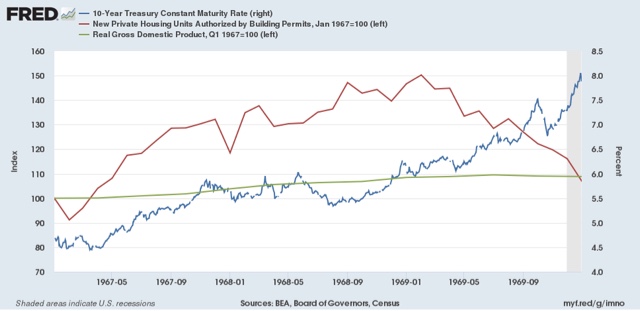

The closest analogue, I suspect, is the late 1960s, where housing specifically and the economy gemerally were undergirded by the tailwind of demand from the burgeoning Boomer generation. There, it took a 2% increase from 4.5% to nearly 6.5% in interest rates before housing, and then the economy, began to roll over:

So, unless rates rise above 3.25% at minimum, I suspect we are going to be OK in nearer term.