Aside from a shortage in starter housing for Millennials,there is NO inflation

by New Deal democrat

Aside from a shortage in starter housing for Millennials,there is NO inflation

Yesterday’s CPI report seems to be read as potentially justifying an interest rate increase in June. For example, here’s Professor Tim Duy, on Fed hawks:

Inflation rose on the back of higher gas prices. Headline CPI gained 0.4 percent, although core rose a more modest 0.2 percent. Core CPI inflation is hovering just above 2 per cent….Fed hawks will be nervous that rising gas prices will quickly filter through to core inflation; doves will remind them that the Fed’s target is PCE inflation, which remains well below 2 percent.

As to his own opinion, he says:

I don’t think June is a go; the data isn’t quite there yet.

And here is Yian Mui of the Washington Post:

The solid [consumer inflation] data helps bolster the case for the Federal Reserve to raise binterest rates at its next meeting in June…..Fed officials have long said that they expect inflation to pick up once the effects of the stronger dollar and low oil prices dissipate. Although the central bank relies on separate data to calculate price increases, Wednesday’s report on consumer costs appears to support the central bank’s claim.

Whether or not the Fed is listening, the fact is that yesterday’s inflation data does no such thing.

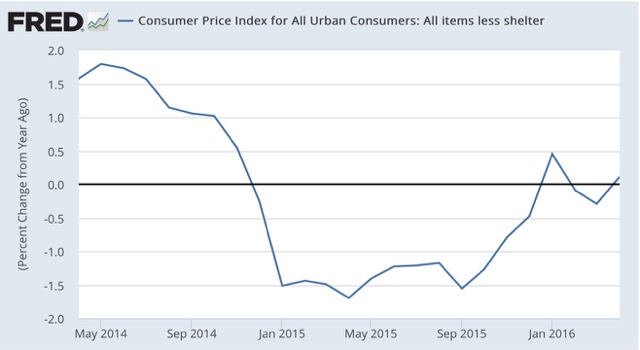

Consumer prices less shelter are only up +0.1%. Not month owner month, but Year over Year! This is one of the lowest rates in the entire 75 year history of the series:

Here’s a close-up of the last two years just to drive home the point:

If housing really were “hot,” if people were buying houses with reckless abandon no matter what the price increase (like 12 years ago), yes there would be a basis for raising rates. But that is not what is happening at all.

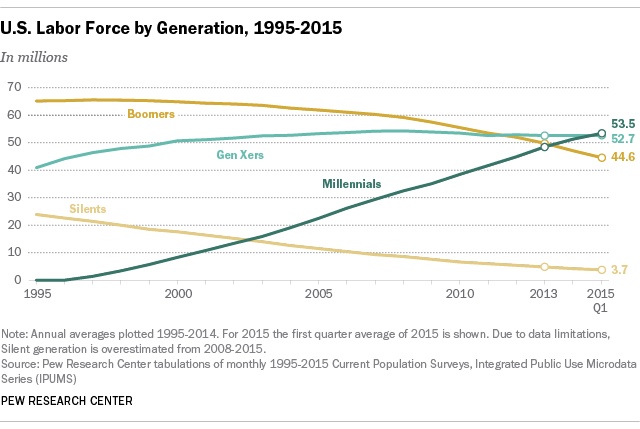

Despite the fact that there are now or will shortly be more Millennials age 18-35 than Boomers:

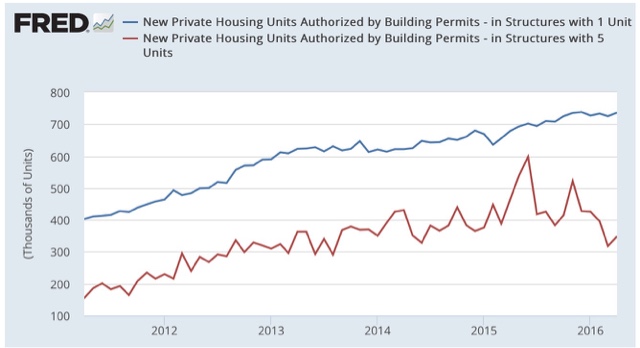

The entry level housing that they need (red in the graph below) is not being built enough:

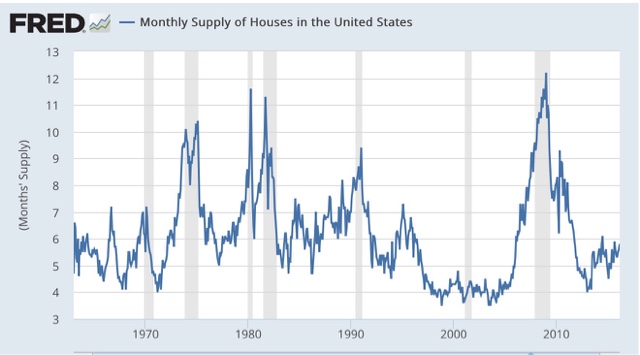

This is confirmed by the relative lack of housing inventory on the market:

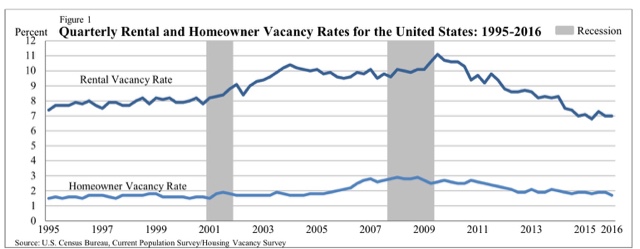

and the near record low vacancy rates for apartments:

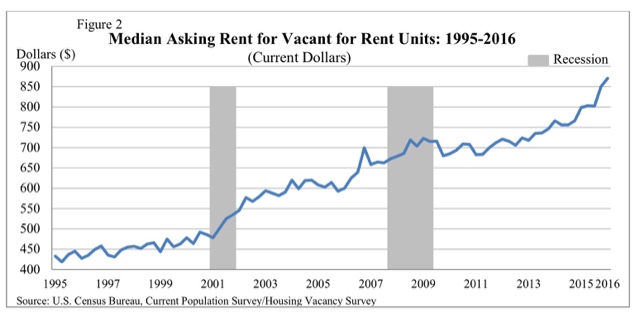

and the soaring rents:

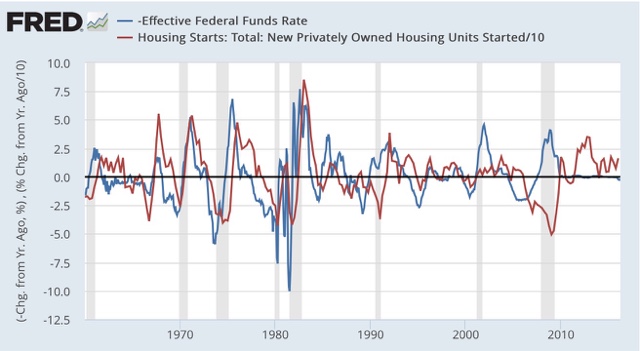

Since rental prices are up sharply due to low vacancies and a dearth of new entry level construction, there is simply no excuse for the Fed to raise rates. In fact, raising rates will only make the multi-unit housing shortage – and the spike in rents – more acute, as the below graph of YoY changes in the Fed funds rate (blue, inverted so that an increase shows as a downward move) compared with the YoY% changes in housing starts (red) shows:

Quiite simply, an increase in interest rates has historically led to a decrease in housing construction:

Except for the housing supply shortage, there IS NO INFLATION. One of the two most likely causes for the next recession will be if the Fed perversely raises interest rates despite these facts.

Update: Here is one important reason for outsized median home price appreciation, and why builders find it more lucrative to focus on the high end market. Chinese all-cash buyers:

Chinese nationals have become the largest foreign buyers of US property after pouring billions into the market in search of safe offshore assets, according to a study.A huge surge in Chinese buying of both residential and commercial real estate last year took their five-year investment total to more than $110bn, according to the study from the Asia Society and Rosen Consulting Group.

cross posted with Bondddad blog

To a real degree, I’m not sure that there IS such a thing as entry level housing. Just entry-level prices for housing. If there is enough total housing for everybody, but not enough of it has entry level prices, than those prices should fall until the prices reflect incomes across the whole spectrum of incomes and prices…

Yes, housing starts are low for the fundamentals. Builders are only building for the top end of the market — largely second homes or retirement homes for baby-boomers. But this creates major data distortions — especially for measures like average price or home size.

As my high school algebra loved to say, you are adding crabs and apples to get crab apples.

As far as inflation is concerned, in a low inflation world, firms tend to raise prices once a year — typically at the start of the calendar year or the firms fiscal year. Consequently, over half of the annual change in the not seasonally adjusted (NSA) core CPI occurs in the first quarter and just doubling the first quarter’s NSA gives a very accurate estimate of the annual reading at the end of the year. This year the NSA core CPI rose over 1.0% — the largest reading since 2009. This implies that the core CPI will rise some 2% this year. If you add in that energy prices probably will rise this year, after a couple of year when they fell strongly,

by the end of the year we are likely to see the CPI running at over a 2% annual rate.

There is a large dose of debate in the Fed’s discussion of inflation. Debating is about finding evidence to support your cause, not about analyzing evidence to determine what your cause should be.

Builders have a huge backload of loans and supply ready to be built. When they bring it out, housing starts are going to pop. I know because they have told me.

Generationally, total bodies are down. echo boomers are rising, but not in that home building demographic years yet.

Dan says:

Consumer prices less shelter are

only up +0.1%. Not month owner

month, but Year over Year!

Dan is surprised at the low annual inflation number. I think he is missing the point. Yes, YoY inflation measures are low. For example, CPI-W (SS COLA) is up a measly 0.235% from May 2015 to April 2016. But so far in 2016 CPI-W is up a real 1.00%, That translate to an annual increase of 3%. That would be a “Too Hot” number for the Fed.

The Fed looks at other measures of inflation, but all these measures are saying the same thing – inflation is running on the hot side so far this year.

I think the Fed will focus its attention on the last 60 days of inflation data when it ponders what to do in June, it will ignore the YoY data that Dan is looking at. If that is the case, then a 1/4% increase in the Federal Funds rate is a month away.

Don’t forget that the Fed tends to avoid changing fed funds, either up or down, in the last couple of months before a presidential election.

This probably implies that they are more likely to raise rates this summer and hold steady until December.