“Saving” and Underconsumption

Some years ago Paul Krugman gave perhaps the best argument against the inequality-causes-underconsumption theory of secular stagnation: the idea that rich people spend less of their income/wealth, so if wealth/income is more concentrated there’s less spending and less GDP/prosperity.

(It’s curious how liberal economists are the ones who most commonly shoot down this argument. That’s the subject of my next post.)

There are two parts to Krugman’s argument: theoretical and empirical. I find both to be weak or fatally flawed. Theory first:

at any given point in time the rich have much higher savings rates than the poor. Since Milton Friedman, however, we’ve know that this fact is to an important degree a sort of statistical illusion. Consumer spending tends to reflect expected income over an extended period. If you take a sample of people with high incomes, you will disproportionally include people who are having an especially good year, and will therefore be saving a lot; correspondingly, a sample of people with low incomes will include many having a particularly bad year, and hence living off savings. So the cross-sectional evidence on saving doesn’t tell you that a sustained higher concentration of incomes at the top will lead to higher savings; it really tells you nothing at all about what will happen.

Parsing this:

1. This argument just says that we don’t know, using this theoretical construct, whether the underconsumption argument is valid. It doesn’t disprove it, rather it just fails to support it. Other quite cogent theoretical constructs do support it. For some reason even liberal economists don’t turn to these constructs.

2. That construct requires fairly strong belief in a fairly strong form of Friedman’s “lifetime income hypothesis,” a hypothesis that has been cogently challenged on many grounds. Since this weakens the value of the theoretical construct, it weakens the “we don’t know” assertion that arises from that construct. We might actually have a pretty good idea, looked at certain ways.

3. Further weakening: It relies on saving as an indirect measure of people’s spending (consumption spending is what we’re asking about here), rather than looking at spending directly. And it doesn’t consider people’s spending relative to their wealth — arguably a much more revealing measure if we’re considering “rich people’s spending.” The saving/spending nexus in national accounting is a very sticky wicket, combining changes in income, borrowing, lending, home values, imputed rent, and capital gains in often unintuitive and confusing ways. If we’re asking a question about spending, it’s usually best to look at spending directly, and that relative to wealth, not income (due to the very statistical problems that Krugman highlights).

In any case, Krugman throws his theoretical hands up, and resorts to empirics:

So you turn to the data. We all know that personal saving dropped as inequality rose; but maybe the rich were in effect having corporations save on their behalf. So look at overall private saving as a share of GDP:

The trend before the crisis was down, not up — and that surge with the crisis clearly wasn’t driven by a surge in inequality.

I find all sorts of problems with this:

1. This graph looks at gross private saving, which includes the financial sector. As Krugman has himself made clear, “saving” by the financial sector is a qualitatively different animal from real-sector saving. It’s huge, it changes a lot over time, and those changes are impossible to parse out by eye looking at this graph.

2. Even if you look at real-sector only (households and nonfinancial businesses), “saving” is heavily influenced by lending/borrowing/payoff trends. It’s a complicated measure to use to discern spending as a percent of assets or net worth or wealth.

Just to emphasize how problematic “saving” is as a measure to evaluate this spending question, consider how important “imputed income” is in the BEA measure of Personal Saving. By far the biggest portion comes from imputed rent, which is itself closely tied to property values hence unrealized capital gains (from heavily leveraged investments), at least in the medium to long run. This even though capital gains are not, according to most national accounting usage, “income.”

You would think that this measure would be straightforward (Income minus Expenditures), but it decidedly isn’t. Take a look:

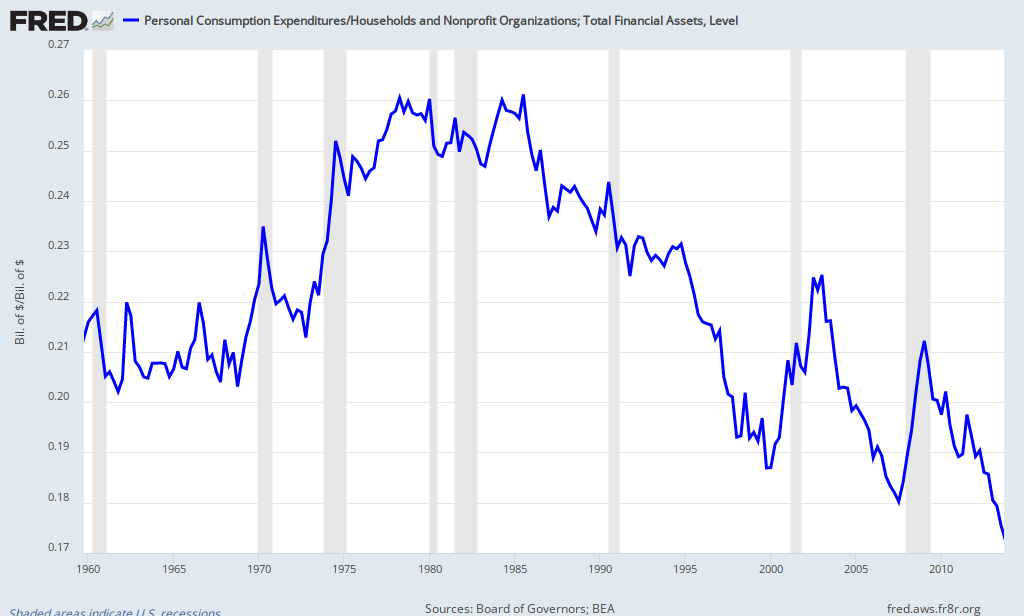

Yesterday I posted this graph as potentially giving us better insight into the question at hand — Personal Consumption Expenditures as a percent of Household Financial Assets:

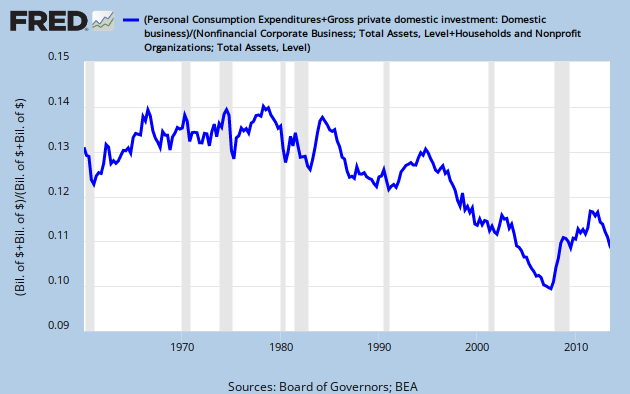

I’ll add another here:

(Personal Consumption Expenditures + Business Investment Spending) / (Household Total Assets + Business Total Assets)

Update: This is all nonfinancial business.

It’s a remarkably similar picture — at least regarding the long-term trend since the 80s.

So there’s some empirics giving some support for what Krugman calls the underconsumption story. (Bad name for it, in my opinion.)

Now how about some of our leading liberal economists delivering on the theory?

Cross-posted at Asymptosis.

The problem with economics concept of savings and accountants concept of savings is they both don’t get consumption on a cash accounting basis. It’s like “fund balance”. As head of a nonprofit, I could not spend the fund balance. The question for me so as I knew what the ex director was doing was “how much is in the checking account?” Cash is king as they say when it comes to consuming.

The only consumption that should matter as to how well the economy is doing in cumulative if you are truly concerned about all the people is the consumption that is the end of the line. The end use of the item produced, service provided. But nooooooooooo, they mix that consumption in with all the other consumption that happens in order to get to that end use including the merry go round financial/capital asset purchases that are both somehow consumption and savings depending on what the clock says. You know it is that milling machine that I bought that is making stuff that I’m writing off over time (accelerated depreciation even) that then continues to produce after it doesn’t count other than having been consumed but it’s not.

Kind of makes all the accounts look bigger than they are.

Nope, what counts in the end is the end. How many widgets coming off that milling machine were sold and ultimately discarded. (Though headed for recycling is better.) Now, just like my flower shop, if more people have an extra $1 I can sell that many more carnations. However, if fewer people have the extra dollars produced, those few people are only going to purchase so many carnations. And that means a slower, smaller, less powerful GDP in the flower shop. I ain’t hiring, I ain’t consuming so much and taxes start looking really high and…

Yeah, I’m keeping it simple, but as I noted here: http://angrybearblog.strategydemo.com/2011/05/monetary-policy-im-sorry-its-just-not.html

the following is still true by simply moving 5 more people into the top group (that is moving to a greater equality): I have a better shot at selling that 1 carnation when there are 15 people that could purchase it than when there are 10.

Hey Krugman et al, how many houses with 30 bathrooms with dual toilets and separate shower/tubs with 29 guest suites do you think are needed to make up for the consumption of the remaining 99% of the population?

Sustainable growth in per-capita output comes from increases in productivity, which in turn requires investment, in training and education to be sure, but primarily from investment in more efficient production facilities, equipment and processes. It is easier to justify investment when it can be amortized over millions of units of output. It is mass-market products and services which drive innovation in production systems. I suspect that yachts are built today not much differently than they were fifty or a hundred years ago. On the other hand, the production of consumer electronics has been revolutionized several times in my lifetime: printed wiring; solid state; integrated circuits; digital VLSI (which radically reduces component counts); surface mount. It is not just the amount of consumption, the specifics matter. My hunch is that many things that the1% spends proportionately more on, do not drive innovation.

I suspect that high profile liberal economists may have wealth/income that puts them at odds with thinking clearly about this subject.

@Ken Schultz:

Absolutely right, IMO. Concentrated wealth (and income) reduces the incentive for producers to develop and market mass-market products. It reduces their “choice” of which products they can make profitably. (Free marketers take note.) Could Apple have thrived with the iPhone absent a prosperous middle class?

The arithmetic of this seems so perfectly clear (though of course there are complex and countervailing economic forces). But (I may be wrong) I don’t see this effect incorporated into economic models.

Why not look at net private savings?

I have been pondering inequality, and believe a lot of it stems from access to private debt. Those with access do better than those without, which means deficits are needed (but spending must be targeted to correct economic group) to close the gap.

Productivity increases alone can not do it. Demand certainly can drive innovation, but there still has to be enough money in the hands of enough people to create the demand.

Apple’s middle class is shrinking as to cumulative wage power, that they can offset it with rising other markets only counts until you get like Walmart.

So, unless we believe that there is equal power in the market place such that wages/income come to an equilibrium with capital that will create the demand such that Apple will keep trying to reduce it’s production costs such that more people can afford the iPhone via a balance of rising incomes and declining cost, I agree with Steve it should be perfectly clear.

Because right now, Apple’s facing eventually a declining demand unless the economic crowd starts considering what happens when people do not receive the benefits of productivity gains as some form of income.

It’s still my problem of being able to sell that additional carnation. Which is still the problem of the economic crowd focusing on the efficiency of money (all those math formulas and models of money flow and productivity) instead of the efficiency of people (GINI vs GDP?)

to Daniel Becker –

Yes, yes, we absolutely need mechanisms that will force improvements in productivity to be broadly shared with workers. If unions can make a comeback, great; if some other countervailing power to business/finance interests must develop, let’s start trying things. My last choice is government-mediated redistribution; Americans have an animus against this, and even if we could wrest control of gov’t back from the moneyed class, the fight to preserve it would be unending.