Fed’s Dudley Agrees: QE is Not About the Reserves, or “Printing Money”

Or: “Dudley Makes Mock of the Monetarists.”

In my post The Fed is not “Printing Money.” It’s Retiring Bonds and Issuing Reserves, I said:

…when the Fed gives the banks reserves and retires bonds, it’s taking on market risk/reward, replacing it with absolutely nonvolatile, risk/reward-free assets (at least in nominal terms). It’s removing leverage and volatility from the banking system.

And:

The banking system doesn’t “take money” out of total reserves, or reduce those reserves, to fund loans.

And now I find this in a speech today at the Japan Society by FRBNY President and CEO William Dudley (HT Matthew Klein). Emphasis mine:

…asset purchases work primarily through the asset side of the balance sheet by transferring duration risk from the private sector to the central bank’s balance sheet. This pushes down risk premia, and prompts private sector investors to move into riskier assets. As a result, financial market conditions ease, supporting wealth and aggregate demand. The fact that such purchases increase the amount of reserves in the banking system and the size of the monetary base is a byproduct — not the goal — of these actions.

Or to put it another way: when you increase M in MV = PY, the most likely result — the result you have to assume by default absent some convincing story about real-economy incentives, causes, and effects — is a purely arithmetic decline in V (cf. Dudley’s “byproduct”), with zero effect on P or Y.

{kind=link}

This is doubly true if by M you mean the Monetary Base (as monetarists do, inconsistently but often) — the only measure of money that includes reserve balances. Increasing the quantity of reserve balances (hence the monetary base) does not magically increase either P or Y.

Cross-posted at Asymptosis.

What the Fed should be doing is focusing on the real problems in the economy:

1. Excess housing inventory. Only time will fix this, bringing forward demand with low interest rates is pointless.

2. Income inequality. Too much of the National Income is going to Corporate Profits and executive compensation. That’s why demand is weak – not because interest rates are too high.

All this QE is doing anything to address these two main problems. All it is accomplishing is re-inflating stock markets and housing prices. Didn’t they learn their lesson when they tried that last time (2002-2006)?

So Steve,

For lack of better terms the Fed is purchasing shit which turns it into gold. Only it’s a special gold that is only capable of being gold while held by the Feds but used by the banks for their balance sheet. Move it off the special area of the banks balance sheet and poof…it’s shit again.

Gee almost sounds like they found their own Social Security trust fund?

This then lets the banks “print” the money. What a racket.

Michael,

I think the banks etc did learn. The also built a sewer pipe to the Fed using they as the waste treatment plant. If I understand Bernake properly, he knows his Fed is not really treating anything, just storing it.

I think Bernake knows this and why he is avoiding addressing those who keep yelling at him to start shutting down the “quantitative easing”. I think he likes his job too.

Daniel, the banks can always print money if they have the right capital ratios, customers who want to borrow and that meet their credit standards – whatever those are at the time. They are definitely not reserve constrained, and never were.

QE might help with their capital ratios by removing crappy mortgage securities, and it definitely adds reserves. But IMO the main purpose of QE is to reduce long rates. QE is also removing $80 billion or so in interest income from the economy, which probably counteracts interest people might save when refinancing. I am not convinced QE has really helped homeowners or the economy all that much. It may actually be hurting it.

Matt,

I agree that QE has not really done anything for the overall (or should I say real or none financial) economy.

I posted my thoughts on it twice: http://angrybearblog.strategydemo.com/2011/06/monetary-policy-im-not-only-not-feeling.html

and: http://angrybearblog.strategydemo.com/2011/05/monetary-policy-im-sorry-its-just-not.html

The QE is allowing the banks to have the right capital ratios. To bad they didn’t do it for the home owner. But, then again would it matter when the home owner’s income is stagnate to declining? I believe we call this a contraction and that’s a depression.

Steve Roth:

“Or to put it another way: when you increase M in MV = PY, the most likely result — the result you have to assume by default absent some convincing story about real-economy incentives, causes, and effects — is a purely arithmetic decline in V (cf. Dudley’s “byproduct”), with zero effect on P or Y.”

The M in the equation of exchange is “money supply”. QE increases the monetary base. Dudley here says that QE “supports” aggregate demand (AD), which by definition is the product of P and Y. And elsewhere in the speech he quite clearly states:

“Credibility requires taking action in the present as well as providing guidance for the future, and we are fortunate to have learned that asset purchases can indeed be an effective tool to support growth, employment and inflation expectations at the zero bound.”

Steve Roth:

“This is doubly true if by M you mean the Monetary Base (as monetarists do, inconsistently but often) — the only measure of money that includes reserve balances. Increasing the quantity of reserve balances (hence the monetary base) does not magically increase either P or Y.”

The monetary base is also referred to as “base money”, “money base”, “high-powered money”, “reserve money”, or “narrow money”. To my knowledge, no one with academic training has ever claimed that the monetary base is the same as money supply.

@Dan and @Matt:

I’ve been starting to think about it this way:

It’s not *currently* about the reserves. It’s about the bonds (hence equities). But for the future, the reserves might/will matter in their effect on (again) the bonds (hence equities).

Currently the Fed is reducing the net net net flow of new Treasuries and GSEs into the private market. This drives up bond prices and drives down yields, which in turn drives up equities as investors look elsewhere for yield.

So by reducing the inflow of new financial assets, the Fed is driving up the price of all financial assets (or at least bonds and equities). This could clearly have a second-order wealth effect on real spending.

The increase in reserves is currently just a by-product of that. but it won’t (might not) always be. Those reserves are essentially increasing the banks’ bond-buying credit limit. Like a credit-card company increasing limits or issuing more cards with limits. That probably doesn’t increase spending much right away because not many people are maxed to their limits. But it does increase potential future spending.

Now the only thing the banks, collectively (the banking system) can do with these higher reserves/higher bond-buying credit limits is…buy bonds — notably, *newly-issued* bonds from treasury and GSEs. If the Fed cuts back on buying and yields rise, banks will give reserves to Treasury and GSEs, which (like sending reserves to the fed) effectively retires those reserves into the government sector. This will buoy bond (hence equity) prices, and keep a limit on yields.

So the eventual Fed cutback or even sellback, and the resultant price increases/yield declines — will be buffered by the reserves that have built up in the system. Yields won’t go through the roof as many fear, nor will investor flee equities for bonds as yields rise.

Make sense?

But what about when the Fed cuts back on purchases

Michael:

“All it is accomplishing is re-inflating stock markets and housing prices. Didn’t they learn their lesson when they tried that last time (2002-2006)?”

The IMF has made it clear that loose monetary policy is not the primary cause of asset price bubbles (Page 106-107):

“If monetary policy were the fundamental cause of house price booms over the past decade, there would be a systematic relationship between monetary policy conditions and house price gains across economies. Certainly, average real policy rates were low and even negative in some economies, and Taylor rule residuals were mostly negative, suggesting that monetary policy was generally accommodative across economies during this period. But there is, at best, a weak association with house price developments within the euro area (Figure 3.13, blue lines).22 And there is virtually no association between the measures of monetary policy stance and house price increases in the full sample (Figure 3.13, black lines). For example, whereas Ireland and Spain had low real short-term rates and large house price rises, Australia, New Zealand, and the United Kingdom had relatively high real rates and large house price rises. Moreover, the association between measures of the monetary policy stance and real stock price growth is extremely weak, whether assessed during the global house price boom (2001:Q4–2006:Q3; not shown) or during a later period, when stock markets rallied from their troughs (2003:Q1) through the stock market declines of 2007 (Figure 3.14).

The fairly regular behavior of inflation and output and the fact that Taylor rule residuals were not associated with recent asset price rises across economies in the sample suggest that monetary policy was not the main or systematic source of the recent asset price booms.23”

http://www.imf.org/external/pubs/ft/weo/2009/02/pdf/c3.pdf

Figure 3.13 is similar to the following graph (note the near zero coefficient of determination):

http://www.federalreserve.gov/newsevents/speech/bernanke20100103slide9.gif

Michael:

“All it is accomplishing is re-inflating stock markets and housing prices.”

It is well known that there is normally little correlation between US inflation expectations and US stock prices. Higher inflation might boost stock prices if associated with growing aggregate demand, but higher inflation can also lead to expectations of tight money, or higher taxes on capital, since capital income is not indexed. Indeed the high inflation of the 1970s seems to have depressed real stock and bond prices. In general, the stock market seemed content with the low and stable inflation of recent decades, at least judging by reactions to changes in inflation expectations.

After 2008 stock prices became strongly correlated with inflation expectations from the TIPS markets. David Glasner documented this pattern, which is actually pretty obvious to anyone who followed the TIPS spreads and equity prices in recent years.

Stocks and TIPS spreads became highly correlated after 2008 because the economy’s main problem was too little nominal GDP, and higher inflation expectations were correlated with higher NGDP growth expectations. Prior to 2008 higher inflation merely had no effect on real returns.

Glasner looked at 8 years of data, from January 2003 until December 2010, and divided the sample up into 10 sub-periods. He found almost no significant correlation between inflation expectations (TIPS spreads) and stock prices (S&P 500) until March 2008. (Actually, there was a modest positive correlation during the first half of 2003, another period when people worried about excessively low inflation.) After March 2008, the correlation was highly significant, and positive. Right about the time where the US began suffering from a severe AD shortfall, the stock market began rooting strongly for higher inflation. And it still is, even in the most recent period. Money is still too tight.

There is no way to overstate the importance of these these findings. The obvious explanation is that low inflation was not a major problem before mid-2008, but has become a big problem since.

The Fisher Effect under Deflationary Expectations

By David Glasner

January 2011

Abstract:

“The response of nominal and real interest rates to expected deflation becomes problematic when nominal interest rates fall toward zero while the expected rate of deflation is increasing. As nominal interest rates approach their lower bound, further increases in expected deflation cannot cause the nominal rate to fall. Either the Fisher equation is violated or the real rate must increase. One way for the real rate to rise is for asset prices to fall. Regressions between 2003 and 2010 of the daily percentage change in the S&P 500 on the TIPS spread measuring inflation expectations show little correlation between asset prices and expected inflation from 2003 until early 2008. However, since early 2008 the correlation between changes in stock prices and in inflation expectations has been strongly positive and statistically significant.”

http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1749062

It’s probably worth mentioning that the only other period in US history that a positive correlation has been found between inflation and stock returns was the 1930s, a period often characterized as an example of a liquidity trap.

Monetary policy, stock returns and inflation

By Ding Du

January-February 2006

Abstract:

“The relationship between stock returns and inflation depends on both the monetary policy regime and the relative importance of demand and supply shocks. A simple analytical framework by which to empirically examine the relative importance of these two factors is developed in this paper. Our findings indicate that the positive relationship between stock returns and inflation in the 1930s is mainly due to strongly pro-cyclical monetary policy, while the strong negative relationship of stock returns and inflation during the period of 1952–1974 is largely caused by supply shocks that were relatively more important in that period. Our results are broadly consistent with the general economic literature on monetary policy and stagflation.”

http://www.be.wvu.edu/div/econ/work/pdf_files/02-01.pdf

Matt McOsker:

“QE is also removing $80 billion or so in interest income from the economy, which probably counteracts interest people might save when refinancing.”

1) A lot of that interest income goes to non-U.S. investors, so QE actually results in that income staying the U.S. rather than flowing abroad.

According the SIFMA there were $11,468.9 billion in Treasury securities outstanding at the end of 2012Q4 of which the Fed held $1,666.1 billion. That leaves $9802.8 billion not held by the Fed. Of that, $5,445.5 billion or about 55.6% were held by foreign and international investors.

2) The marginal propensity to consume (MPC) of domestic Treasury holders is often lower than that of non-holders.

Banks, insurance companies, mutual funds, and other corporations hold $1813.4 billion in Treasuries or about 18.5% of those not held by the Fed. Corporations are already sitting on a very large cash hoard this recovery so contributing more to it would probably be unlikely to add much to aggregate demand (AD).

Approximately $1,036.0 billion or 10.6% of the Treasuries not held by the Fed are held by individuals. But according to Edward Wolff, as of 2007, approximately 60.6% of all financial securities (which of course includes government bonds) held by individuals were held by those in the top 1% of net worth (i.e. net worth of $8,232,000 or more) with another 37.9% held by the next 9% in net worth (i.e. between $882,000 and $8,232,000 in net worth). That leaves only 1.5% of financial securities held by the bottom 90% in net worth. People with high net worth tend to have a low MPC.

3) The drain on interest income is more than offset by easier financial conditions elsewhere (via equities, credit spreads, etc).

According to the Federal Reserve Flow of Funds there was approximately $42,000 billion in debt owed by households, businesses and state and local governments in the United States at the end of 2012Q4. And, as a rule, borrowers usually have a higher MPC than savers.

@Mark: “The M in the equation of exchange is “money supply”. QE increases the monetary base.”

This would be a useful statement, and MV=PY would be a useful equation, if there was any agreement on the meaning of “money supply,” and if that agreed-upon definition was used consistently and coherently in discussions of MV=PY.

Unfortunately neither of those is the case.

Are you saying that “money supply” means monetary base? Yes or no please.

If so, since MB does not include bank deposits, an increase in bank deposits is not an increase in the “money supply,” M. Do you stipulate to that?

If not, please give a precise definition of “money supply,” M, in MV=PY.

You will find a very lengthy and decidedly non-precise definition here:

http://en.wikipedia.org/wiki/Money_supply

And understand: if M is not MB, then reserve balances are not part of M. They’re not money under your definition.

Unless: you have a new definition of “money supply,” which includes both bank deposits and reserve balances. No existing definition, M0-MZM, or MB, includes the two.

Choose your poison.

Watch Scott Sumner play fast and loose with all this here:

“increases in the rate of money growth lead to higher inflation, which leads to higher velocity and lower real money demand. This means that in the long run an increase in the money supply growth rate will cause prices to rise by even more than the money supply increased. Conversely if money growth slows, inflation will slow, the opportunity cost of holding base money will fall, ”

He’s going along talking about money in some vague sense that he doesn’t define — but that one presumes must include bank deposits, no? — then suddenly he’s talking about holding “base money,” which does not include bank deposits!

How can you expect to think coherently about this subject given that kind of sloppy thinking and language? With its non-existent, ambiguous, and/or shifting definitions, that passage has no coherent meaning.

Steve Roth:

“Are you saying that “money supply” means monetary base? Yes or no please.”

No. (I thought that was evident from my comment.)

Steve Roth:

“If not, please give a precise definition of “money supply,” M, in MV=PY.”

Money supply is anything that is accepted in payment for goods and services or in payment of debts. In the case of the U.S, any of the empirical measures defined by the Federal Reserve satisfy this definition with differing degrees of liquidity.

Steve Roth:

“He’s going along talking about money in some vague sense that he doesn’t define — but that one presumes must include bank deposits, no? — then suddenly he’s talking about holding “base money,” which does not include bank deposits!

How can you expect to think coherently about this subject given that kind of sloppy thinking and language? With its non-existent, ambiguous, and/or shifting definitions, that passage has no coherent meaning.”

I personally do not find Sumner’s thinking or language sloppy in the quoted passage. The language he is using has been around for well over half a century.Anybody well versed in monetary economics knows precisely what he is talking about.

Mark writes:

“1) A lot of that interest income goes to non-U.S. investors, so QE actually results in that income staying the U.S. rather than flowing abroad.”

I’d say it does not “stay” anywhere, but goes to the treasury reducing the deficit thus reducing net financial assets flowing to domestic and foreign sector accounts. Also, QE3 it is not just treasuries, but mortgage securities. In the end, QE’s effect is not better than trying to kill James Bond with a shark.

@Mark:

>>please give a precise definition of “money supply,” M, in MV=PY.”

>Money supply is anything that is accepted in payment for goods and services or in payment of debts.

Okay so the unused spending limit on my credit card is money, and is part of the “money supply.” That right?

It’s “accepted in payment” almost everywhere, so according to your definition, it’s money.

See what I mean by “precise”?

Matt McOsker:

“I’d say it does not “stay” anywhere, but goes to the treasury reducing the deficit thus reducing net financial assets flowing to domestic and foreign sector accounts.”

I was talking about non-U.S. holdings so such interest income is being diverted from flowing abroad to flowing to the U.S. Treasury.

Matt McOsker:

“Also, QE3 it is not just treasuries, but mortgage securities.”

1) At the end of 2012 the Federal Reserve held $2,675 billion in securities of which $1,018 billion were Agency securities or about 38.1%.

According the the Federal reserve Flow of Funds Report there were $7544 in Agency securities outstanding. That leaves $6,526 billion not held by the Fed.

2) True, non-U.S. investors only held about $1,077 billion or 16.5% of the Agency securities not held by the Fed.

3) However, the marginal propensity to consume (MPC) of domestic Agency security holders is also often lower than that of non-holders.

In particular, banks, insurance companies, mutual funds, and other corporations hold $5,051 billion in Agencies or about 77.4% of those not held by the Fed.

Steve Roth:

“See what I mean by “precise”?”

Let me put it this way, I now see where you’re coming from.

People who have tried to formulate the definition of “money supply” on a priori grounds have generally stressed either the “medium of exchange” function, or the “asset” function of money. These approaches seem to provide an unsatisfactory basis for defining money supply. However, in my opinion the definition of money supply is an issue to be decided not on grounds of principle as in the a priori approach, but on grounds of usefulness in organizing our knowledge of economic relationships. Thus there is no hard and fast formula for deciding what total to call “money supply”.

As distressing as this may be to some people, as an empiricist, this does not at all cause me to lose sleep at night.

@Mark:

Empirics is exactly why this is troubling to me.

When somebody makes an M-related statement without defining M, there’s no way to confirm or refute it empirically. There’s always a definition available that effectively cherry-picks some empirical data (especially if the period is chosen carefully) to support pretty much any statement. But there are other definitions/data sets that say otherwise. It’s like wrestling with water.

And especially: if the definition changes from one thing to another in the middle of a statement (especially if both definitions are vague), can that statement be tested, empirically? If not, does it demonstrate, teach us, anything?

As an empiricist trying to figure out how the world works, would you feel comfortable if P in PV=NRT or E in E=MC^2 were vaguely and variously defined (hence not defined)? Would you find those equalities useful in understanding the world?

I hope you’ll understand when I say that your response sounds a lot like “whatever works, depending on the axe (or side of the blade) one happens to be grinding at the moment.”

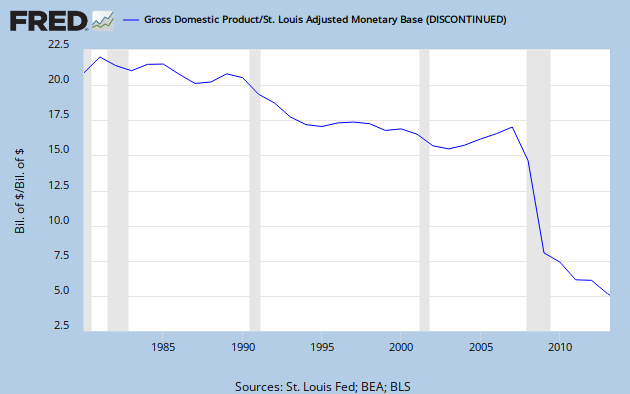

@Mark:

I was just poking around, and came up with this chart:

Which has me asking yet again: what exactly do you mean by “money”?