Identity Games: Saving ≠ Saving? Whodathunkit?

I finally figured out a simple way to explain my confusion (and that of many others, including many economists) with the whole Saving issue. I may also have figured out a useful solution to that confusion, which I present at the bottom here for my gentle readers’ delectation and denunciation.

Econ profs: I’m really curious. Do you think this post would help your intro students understand this stuff?

First: The accounting’s fine. Of course. But for some not-crazy reasons, the definition of “Saving” changes in the course of the accounting.

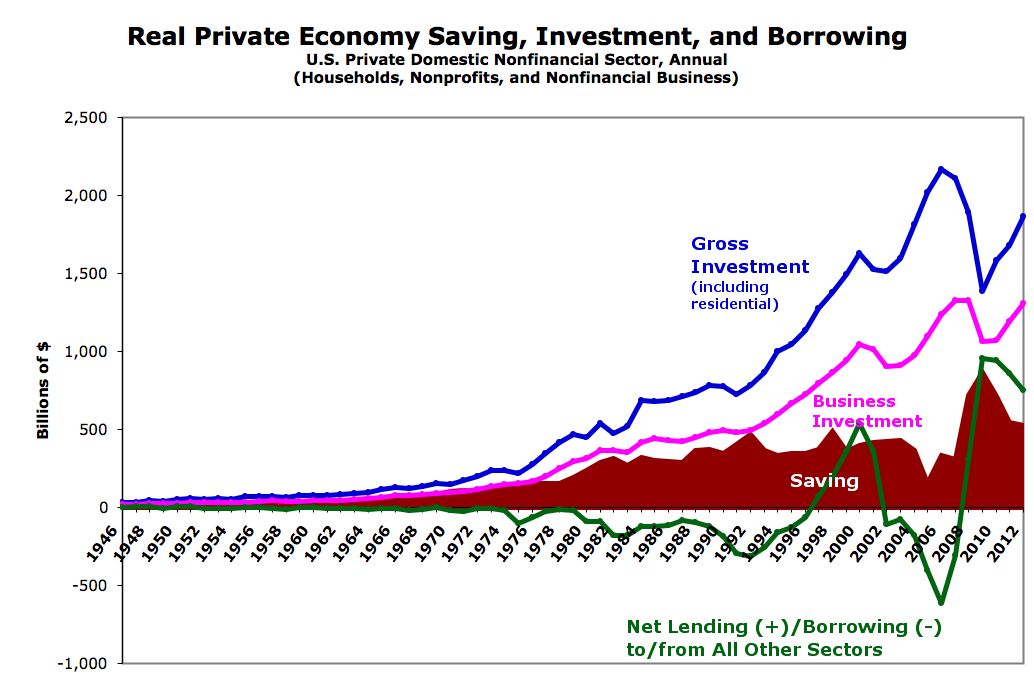

Thinking of the “real” sector for the moment, for simplicity and clarity. For each of the economic units at the bottom level of that sector (households and nonfinancial businesses), Saving means money saving:

(1) Saving = Income – Expenditure

But at the top, the level of “sectoral” saving, Saving means saving of real goods:

(2) Saving = Income – Consumption Expenditures

Or in words that more aptly describe what’s being depicted:

(3) Saving = Production – Consumption

(Reminder: Consumption Spending + Investment Spending = Expenditures = Income = Production)

Explanatory aside: There’s Gross or Net Saving, depending on whether Consumption just includes Consumption Spending (on goods that are bought and consumed within the period), or also includes Consumption of Fixed Assets — the very real “depreciation” of those assets. Gross is long-lived goods produced; Net is long-lived goods added, above and beyond what’s “consumed.”

Back to identities: Unlike every other measure in the national accounts, if you sum up the money Saving of all the bottom-level units, it doesn’t equal Saving for the sector. Rather:

(4) Sectoral Saving = Units’ Combined Money Saving + Investment Spending*

Investment spending, of course, causes the creation of real, long-lived goods. But this is the thing that has confused me from the get-go: Saving is (savings are) some combination of money and real goods? Aren’t financial assets supposed to be representative of, proxies for, the real assets? (Equally confusing: economists’ insistence on talking about “capital” as if it were some undifferentiated, homogeneous or vaguely contiguous lump of real and financial capital.)

Here’s what you need to know to sort that out: You know that money saving? It’s zero.

As JKH has quite rightly pointed out, if Sectoral Saving means money saving, “one stumbles upon the unhelpful conclusion that global saving…is identically zero, which is not very productive.” Income = Expenditures, right? One person’s spending is another’s income. So for the world or any closed sector (no net flow in or out), Money Saving (Income – Expenditures) must equal zero.

If you plug that zero into (4), voila, you get:

(5) Sectoral Saving = Investment Spending

This makes sense in the accepted sectoral definition; investment spending increases the stock of real, long-lived goods — Sectoral Saving. But if you don’t get confused when Spending = Saving, you’re a better soul than I.

While JKH is (identically!) correct, I completely disagree that this is “unhelpful” or not “productive.” Because in fact a money-saving approach perfectly depicts the actual situation in a way that’s easy to grasp — which is important given that so many find it so hard to grasp. If there’s no flow in from other sectors (Government and Foreign, ignoring the financial sector for the moment), the units in the real sector, in aggregate, can’t save money. You get this familiar, MMT-favorite identity:

(6) Government Deficit + Trade Surplus = Real Sector Money Saving (Net Acquisition of Financial Assets)

When you’re looking at the actual accounts, Money Saving doesn’t equal zero. Because we all know: households and businesses save money — but only, in aggregate, if there are inflows from outside (which there are). If Sectoral Saving meant money saving, as it does at the bottom, unit level, what you see at the top would be the non-zero sum of what you see at the bottom.

It’s not crazy to think about sectoral saving as money saving. Both the NIPAs and the FFAs provide a sector-level measure of Personal Saving (households), which is unequivocally money saving: Money Income – Money Expenditures. (Nobody would say that household saving is “stockpiling of real goods.”)

Unfortunately the accounts don’t have a similar measure of money saving labeled Business Saving, which would be this:

(7) Business Saving = Income – Expenditures – Distributed Profits = Undistributed Profits

(This because Distributed Profits count as Income for households, so they contribute to Household/Personal Saving, not Business Saving.)

Why no such Business Saving measure? Because this is the turning point, the crux, of the definitional legerdemain. Within the real sector in the NIPAs, businesses only do Investment Spending, and only businesses can do Investment Spending. (Households only do, only can do, Consumption Spending.) Is Investment (aka Business) Spending an Expenditure, or isn’t it? Is it Expenditure or Saving? If there were a measure here called Business Saving — money saving — then matter (real goods) would collide with antimatter (money), and the Universal Accounting Construct (perhaps the whole universe!) would explode and vanish in a fiery conflagration.

Okay, fine, hyperbole. But really: we know that businesses save money. You’ve no doubt noticed that corporate cash balances are at historic, all-time highs. It’s hard to pull that off if they’re not saving money. It would be nice to see that money saving by businesses clearly presented as such, in so many words, in the national accounts. It could then be totalled up with Household Money Saving to show Real- (nonfinancial) and Private-Sector Money Saving.

I’ve got more to say on all this, but I think I can clarify best by suggesting a different way of thinking about it, using different words/labels/definitions that might cut this conceptual Gordian knot, and help people better wrap their brains around the national (and world) accounts.

I’m going to talk in terms of the NIPAs here, and about the real sector, because the constructs are different in the FFAs, adding the financial sector makes things more complicated, and I want to be perfectly clear.

The basic problem: we’re short a word. We have more things to describe than we have words. So I’m adding one.

Whenever you see Saving in the NIPAs (except “Personal Saving”), replace in your mind with:

Accumulation (of real goods)

When you think about Saving, think money saving:

Household/Personal Saving (Income – Expenditures)

+ Business Saving (Income – Expenditures – Distributed Profits = Undistributed Profits)

Adopting those labels, when you see “Investment,” think:

Spending that adds to the Accumulation measure

Consumption?

Spending that doesn’t add to the Accumulation measure

And here’s the crucial point:

Neither Consumption Spending nor Investment Spending adds to or subtracts from the Saving measure. Not directly.

Each of these spending flows increases Income and Expenditure simultaneously and equally, so they can’t increase Saving (which is the difference between the two). Sectoral Saving only happens if there are inflows to the sector.

If you want to talk about indirect effects (incentives, constraints, emergent properties, etc.), you’ve left the backward-looking realm of accounting, and entered the world of Economics, Psychology, Sociology, Dynamic-Systems Theory, and a whole host of other disciplines. Accounting can never tell those disciplines when they’re right. It can only, and only sometimes, tell them when they’re wrong.

In that backward-looking world, we can say that X% of spending in a period was Consumption Spending, and the rest was Investment Spending. But that tells us exactly nothing about what caused the mix. We can’t say from the accounting, for instance, that if there had been less Consumption Spending, there would have been more Investment Spending. The result might just have been less spending overall (even, perhaps, less Investment Spending), so less Income, and less Production (allowing for the buffer stock of inventories, though that looms ever smaller as our economy goes past 80% services, and produce-on-demand supply chains for physical goods get ever more efficient; the production comes after, and is caused by, the expenditure).

This last point — that spending (of either type) doesn’t reduce sectoral saving — is crucial because failure to understand it lies at the root of things like the ridiculous loanable funds model, the idea that more individual money saving (not-spending) causes more investment, the notion that consumption spending takes resources “out of society,” and many other evil and foolish economic misconceptions that I might encapsulate somewhat trivially with two words: “trickle down.”

Also realize: When you look at actual data for the real sector and think about it using these terms, Saving and Accumulation (née Saving) won’t show any kind of obvious relationship, except that they both generally grow over time with the economy.

{kind=link}

That’s because the sector isn’t closed. There’s lending/borrowing to/from the other sectors, and loan payoffs in both directions — summing out to Net Lending/Borrowing — and crucially, trade imbalances, and government deficit-spending into the real sector, with money created ex nihilo. (The latter being the ultimate though not necessarily proximate source of real-sector money saving, a.k.a. Net Acquisition of Financial Assets.)

For the (open) real sector over the long term, Income > Expenditure. Hence: money saving.

For those who have been confused as I have been (and who admit it), this thinking and terminology might make it easier to think about important questions of (macro)economics — how personal/business saving relates to investment and production, the role of debt and equity financing and the financial industry in economic growth, the nature of “demand,” how the stock of financial assets (so-called “financial capital”) relates to the real capital stock, etc. I’d love to hear your thoughts.

Before I go, one more thought: After coming up with this “accumulation” notion/usage, Very Little Googling revealed that (no surprise) it’s hardly original. It’s right there in Volume I of Das Kapital. (I just discovered this? Hey, I’m self-taught, with the resulting predictably spotty/spotlight reading background. I’m working on it!)

And let’s not forget: It was the 1930s. Kuznets and co. were developing the national accounts, and they were devoted capitalists. They’re gonna use Marxist language, much less concepts and theory? In the National Accounts? Of The United States of America? Not gonna happen.

Just a notion. But it does make sense…

I said at the top that Saving in the national accounts is labeled the way it is for not-crazy reasons. Some who are better-versed in Marx and his (far more cogent) successors than I am, might beg to differ with me.

And I might very well agree with them.

That’s the kind of normative, rhetorical, and ultimately political insight and implication to all this seemingly mundane and purely “positive” accounting stuff that I’d like to write more about in future posts. Thanks for listening.

* For those who are thinking S = I + (S – I): right. Writing and rewriting this post (over and over and over) finally helped me internalize it.

Cross-posted at Asymptosis.

So I think what is missing in all of this is labor. And, the concept of stationary vs motion because all of these definitions are dependent on any given moment of time or moment of elapsed time.

Savings is stored labor, whether an individual or a business. Once it is moved from storage it is either consumption or capital expenditure/investment. Both can produce income to some entity. Both may become savings to some entity. However, only capital expenditure/investment can producing savings for both parties involved because both represent potential production…labor (human or otherwise). In this labor = work potential.

Thus, unless the following is some definitional consensus within econ or accounting, I can not agree with: Households only do, only can do, Consumption Spending. That’s convenient for accounting, but not economics. Any savings spent by the household represents work done, thus income to the entity/unit that received the household’s consumption. It “may” represent a multiplication of the household’s labor potential if the expenditure added value (value being the potential for greater work done) of some type (education, work saving device, energy reduction device, etc).

The only true consumption is when the value is fully expended from the work done. A cigarette smoked is the end of the line for the work done. No more value. However, even this is time dependent as the expended value of the cigarette will produce demand for some other labor.

To keep my comment short, this makes the entire concept of the financial sector as having capital, savings, investment laughable. Finance is nothing more than a pilot fish. Finance is not necessary in any of this. It only exists as a human creation to accelerate labor’s results. Again, time is the factor.

I think I understand that in seeking clarity on “savings” you are looking to meld accounting and econ? To be complete with such a model labor has to figure. That it has not figured in the national discussion of our economy I believe is a product of convenience. It allows the “trickle down”.

@Daniel Becker: “Households only do, only can do, Consumption Spending”

That’s how the NIPAs are set up. Check out table 2.1, Line 28 ff.

http://www.bea.gov/iTable/iTableHtml.cfm?reqid=9&step=3&isuri=1&903=58#.UXSY5TKr93Q.gmail

In the NIPAs, households don’t have a capital account, so they can’t “save” in the sense of accumulating real goods. Even their durable goods purchases — even cars — don’t add to the capital stock. (And if they pay someone to build them a house, it is imputed to the real estate industry, with imputed rent pulled from their accounts as a consumption expenditure.)

This can, definitely, make it hard for people to think cogently and coherently about how economies work. For quite a while I’ve been thinking of doing a post about this construct’s effect on economic thinking, titled “Thinking Inside the NIPAs.”

And we wonder why Labor, the 99% can’t get no respect in economics and policy. 🙂

Daniel, maye the way to view this is when there is excess labor capacity, then that simply means savings is simply too low. Savings needs to be increased with fiscal policy, or possibly a better balance of trade. So the accounting might be telling us all we ned to know.

Note|

FRED charts has added NIPA table data.

Matt,

I don’t understand what you are saying. Currently we have excess labor (potential) and high business savings and personal savings. Personal savings more than doubled in the recession with it only recently (last 2 years) starting to decline.

Rising “personal savings” is what we see in recessions along with rising excess (prefer unutilized labor).

@Matt: “maye the way to view this is when there is excess labor capacity, then that simply means savings is simply too low.”

I’m with Dan. Putting aside the useless and circular retrospective accounting view (“If there’s more saving/less spending there must be less spending”), looking forward: if people *want* to spend less of their income (save more), that reduces expenditures, which reduces incomes, which… A self-perpetuating cycle.

That want/desire, and the change in that want/desire, *is* the moving demand/supply multiplier.

Explained far better than I can by Josh Mason here:

http://slackwire.blogspot.com/2013/04/aggregate-demand-and-modern.html

Including, in the comments, this nice encapsulation, plus a contrast to the “Nick Rowe” view:

“For us, a “demand problem” means that someone has chosen to reduce their expenditure relative to their income, and because in modern economies there is a strong causal link from expenditure –> output –> income –> expenditure, the effect of this is to reduce total activity in a self-perpetuating way.

Whereas for Nick, it means there is excess demand for means of payment, and excess supply of currently produced goods, which will last until the supply of money increases, or the price of currently produced goods falls.”

Nice discussion from Nick in there as well.

I look at corporate cash, pensions etc…. as demand leakages, but it is still private demand to do those things, and that detracts from current consumption. I save in my 401k so that I may become an old rent seeker someday. There are things I might purchase now if I did not set aside that portion of income. I might also use that to pay down debt. The debt overhang Pre-2008 means there is demand to pay down debt. Basically, demand is being funneled away from consumption and people’s incomes are being squeezed at the same time by higher taxes (federal, state and local). This to me means net private savings needs to continue up in hopes you can stimulate demand, but no guarantee. Fiscal policy is all that is left.

I also have to wonder if low interest rates create even more demand leakage as higher cash flows are needed to generate the necessary returns in say pensions.

well, the problem is “words.”

a person trying to explain something has to use words, some of which have been used in other contexts to mean (point to) something else.

if that person is a good enough writer and has something worth saying people will understand.

the trouble comes when someone else uses the word with its “new” meaning to mean (point to) either the original meaning or something else entirely.

and since everyone in economics uses words to “prove” their favorite hypothesis, after awhile no one knows what they are talking about.

except the professors, who are very proud to be the possessors of secret knowledge.

Matt,

I’m not confident that there is a demand to pay down debt because of debt overhang. I believe there is a movement to pay down debt do to a declining ratio of debt to income.

Even a foolish bank set limits on that ratio and once the income could not carry it…poof, debt pay down vs more borrowing.

This is true with your tax example. Taxes are not “too high”. I have shown this here back when I first started blogging. It is that incomes are too low.

Yes, low interest rates require high cash flow into the “cash savings” to remain relative to compounded growth of yesteryears. However, interest rates are a function not so much of demand for money, but for demand of loanable opportunities in a financialized economy. With savings as they are, there are limited loanable opportunities, thus I can borrow low and you will lend to me low as you have no where else to generate income.

With mega corps being cash rich, I would think it has effected loanable opportunities making things worse.

This would explain the totally unconnected stock market indexes. It is just the same money turning over creating the appearance of loanable opportunities.

Daniel – I would like to see incomes go up too. But, how will that happen with 15+% unemployment? Don’t we need to lower unemployment first?

Europe is a good example strong unions etc, but fiscal policy is shredding their economies, and unemployment is ridiculously high.

Cutting taxes increases workers take home pay, I don’t see how that hurts. Note I am talking about tax cuts for the 99%, and not the 1%. I’d like to see tax rates fluctuate mechanically with the unemployment rate.

In the end, we need to be running deficits of $1.5 Trillion if we even want to get to full employment.

“You get this familiar, MMT-favorite identity:

(6) Government Deficit + Trade Surplus = Real Sector Money Saving (Net Acquisition of Financial Assets)”

MMT people sometimes put it like that, but in fact it has to be

government deficit + CURRENT ACCOUNT surplus

– not trade surplus.