Wealth vs Income

Usually my articles present facts and data and try to drive down to a conclusion. This time, I’m going to drive down to a couple of questions.

Recently, Noah Smith had a post on the subject of economic models titled Filling a hole or priming the pump? It did quite a bit to restore my lack of faith in the pseudoscience of Economics, but that is more or less beside the point. Roger Farmer, cited in the post, left a long comment that Noah hoisted up the main page. Farmer concludes:

My reading of the evidence is that consumption depends primarily on wealth rather than income. That was the lesson of work by Ando and Modigliani, Modigliani, and Friedman in the 1950s. It is for that reason that I support interventions in the asset markets that try to jump-start the economy and reduce unemployment by boosting private wealth. That, in my view, is what quantitative easing has done.

Ok – I’m taking on decades of economic research here, but my first question relates to: “My reading of the evidence is that consumption depends primarily on wealth rather than income.”

First, let’s remember that wealth distribution is on the order of the top 1% owning 40% of the wealth, and the bottom 80% owning 7% of the wealth. And that 7% is not evenly distributed. There are significant fractions of the population who have a) no wealth at all, or b) negative net worth. Either way, they are living hand to mouth. This suggests that 1) they have unmet needs, and 2) will spend the next available dollar trying to satisfy one of them.

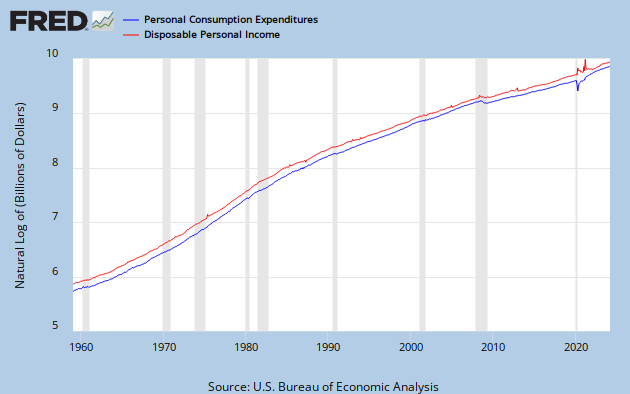

So far, this is just a thought experiment. Let’s take a look at how personal consumption expenditures track disposable income. Here is percent change from previous year:

Both in the grand sweep and in the year-to-year detail, the curves are pretty much in lock-step.

Here is the data on a Log Scale:

That’s coordination about as close as you could ever hope to see in real world data.

And if wealth – or it’s perception – were the determinant, wouldn’t you expect some sort of a consumption bump during the housing bubble, when people felt wealthier than their incomes justified? Let’s look at consumption expenditures per capita.

Here, there is a slope increase, mid last decade, but it’s not great, and it’s no greater than the slope of the late 90’s. I suppose the tech boom must have had some people feeling wealthy then, as well. But they weren’t that bottom 80%. Note that the first graph indicates the personal disposable income was up in those periods as well. In fact, they were the only up periods since about 1980.

There was also relatively low unemployment in those times, and thus more people with incomes.

Also, it just seems counter-intuitive in a world where, if real people think about money at all, it’s in a personal cash flow context, not in terms of wealth aggregates. Consuption decision reasoning, to the the extent that it even occurs, is along the lines of: “If I buy this thing, can I still afford to feed my cat?”

So, here is question number 1:

Since to most people “wealth” is miniscule, non-existant, or worse, and given empirical data that closely links consumption to income, how can consumption depend “primarily on wealth rather than income?”

Now let’s look at Excess Reserves of Depository Institutions.

There’s 1.6 trillion QE dollars. Any left-overs have gone to leveraged speculation causing commodity inflation.

But Farmer says: “I support interventions in the asset markets that try to jump-start the economy and reduce unemployment by boosting private wealth. That, in my view, is what quantitative easing has done.”

If any wealth has been boosted here, it is in the upper reaches of the already wealthy, not among the working stiffs who are highly inclined to spend the next dollar rather than hide it away in Luxombourg or the Cayman Islands.

So, here is question number 2:

How can QE money help the economy when it is either sitting idle or inflating commodity prices?

I have nothing in particular against Roger Farmer, about whom I know nothing, but I am also prompted to ask economists in general:

What in the hell is the matter with you?

So maybe my lack of faith in Economics is the point, after all.

Cross-posted at Retirement Blues.

“My reading of the evidence…” translates as evidence? who needs evidence? the answer is self-evident.

“And if wealth – or it’s perception – were the determinant, wouldn’t you expect some sort of a consumption bump during the housing bubble, when people felt wealthier than their incomes justified?”

I would not expect to see a wealth effect in a graph that pooled everybody together.

🙂

Min –

Why not? If wealth, in the aggregate, effects spending, in the aggregate, there ought to be a correlation. Or perhaps I’m missing something. Please elaborate.

JzB

Can I assume the first log-scale graph of PCE over DSPI is for the population at large? This seems to be the case. If so, is there somewhere we could see the same chart for the top 10%, 1% and .01%?

BTW, I really like the nickname of the final chart, showing the excess reserves. EXCRESNS, indeed. Someone has a sense of humour.

Noni –

Yes, those are aggregate numbers for the population.

You’re asking a great question. I have no idea what the answer is.

As an economic illiterate, I use simple resources that I know how to find, and FRED is very accomodating.

It seems to me, though, that wealth is the accumulation of disposable income that hasn’t been disposed of, but rather converted into financial assets.

Intuitively, then, there is no reason to expect wealth and consumption to correlate in any way.

http://en.wikipedia.org/wiki/Consumption_function

I am not saying this answers everything. But at least one very sharp mind has thought very hard about it…

well i would expect that “disposable” income would ideally be spent on “capital goods”.. building the machinery to make our lives even easier.

but to the extent that it is “converted into financial assets”… which i take to mean gambling and drinking… then there needs to be another accounting category… call it “wasted.”

The wealth effect on spending is individual. As you started out talking about, right? People with little wealth consume much more proportionally than their wealth, and their consumption is regulated by their income. It is only when you get people with enough wealth that wealth controls their consumption more than income. Once we have admitted such an interaction, then lumping people together becomes misleading. In statistics there is a simple rule: Don’t do that.

There are some other factors at play. We agree that those without enoug wealth spend most of their income. For those with enough wealth, consumption is roughly proportional to wealth. (I am surmising that, based upon the idea of the moral value of money. The relation may be different.) But what if, in your population, most of the wealth is held by few of the people? Their incomes are roughly proportional to their wealth, through investments. Then what we might see, if we did not just lump everybody together, is that both the poor and the wealthy would have consumption roughly proportional to income, while only the group in the middle would show consumption not proportional to income. Lump everybody together and the rich and the poor might dominate the picture, so that it would look like consumption is governed by income.

Let me say a few words to clarify why consumption depends on wealth. What could I mean by that? There are two points that I would like to clear up. 1) Correlation is not causation. 2) The economic definition of wealth is not purely the value of our houses, factories and machines; it includes future labor income.

First: correlation is not causation.

By definition, GDP, in a closed economy, is equal to consumption plus investment plus government purchases. If we set aside indirect taxes and depreciation, GDP is also identical to income. Consumption is two thirds of GDP so if consumption goes up, and if that increase does not cause a fall in investment or government purchases, income will go up. That is why consumption and income are correlated in time series data.

The statement that “consumption depends on income and not on wealth” refers to the central component of Keynes General Theory: a behavioral relationship that Keynesians call the consumption function. This asserts that if income increases by one dollar, consumption will increase by a fraction “b” of one dollar because of the choices made by households. “b” is called the marginal propensity to consume. When we disentangle correlation and causation it appears that the simple Keynesian consumption function does a very bad job of explaining the data. That was the conclusion of the “decades of economic research” that you are taking on.

Second: Wealth is not just houses, factories and machines.

Wealth in the U.S. has three major components; 1) houses, 2) factories and machines, and 3) the present value of future labor income, or human wealth. For the U.S. economy as a whole, houses are roughly one times annual GDP and factories and machines are another two times GDP. The sum of those two components comprise tangible wealth and you are correct to point out that tangible wealth is unequally distributed across households. For most of us, our biggest asset is our human wealth; the present value of what we expect to earn from employment over our entire lifetimes. Under a conservative estimate, that is at least another five times annual GDP.

In the 1950s, Milton Friedman formulated the permanent income hypothesis which asserts that consumption depends not on current income, but on the income that accrues from all of our assets including the income we expect to earn from future wage income. Modigliani, Ando and Brumberg, in separate research, formulated the lifecycle hypothesis; the idea that households take the future into account when planning current consumption. The lifecycle hypothesis and the permanent income hypothesis have similar implications for the Keynesian consumption function: they imply that an extra dollar of income will only be consumed to the extent that it is expected to be permanent.

My reading of data (see page 26 of the working paper) here:

http://rogerfarmer.com/NewWeb/Working%20Papers/Farmer_USTK.pdf

is that when government purchases increase; households respond by saving more; that is, consumption goes down. That is the exact opposite of what is supposed to happen in a Keynesian world.

If there are losses of $1.5 trillion (let’s just pretend its all in houses and mortgages), and the governmnet/fed spends an additional $1.5 trillion, isn’t that a wash? Then how do we account for flows out of the US economy against this equation?

It seems to me all of the stimulus just to filled in a hole we already dug, versus having additional dirt that causes the hole to overflow.

Farmer

you argument is actually too long to be credible. i’d call it a house of cards, but at least in a house of cards you know what the cards are. you have too many “theoretical entities”. it would take far too long to disentangle all the assumptions.

“My reading of the evidence is that consumption depends primarily on wealth rather than income. That was the lesson of work by Ando and Modigliani, Modigliani, and Friedman in the 1950s. It is for that reason that I support interventions in the asset markets that try to jump-start the economy and reduce unemployment by boosting private wealth.”

It is for that reason that I support interventions to boost private wealth by giving money to poor people. 🙂

Also a Milton Freidman idea, BTW, giving money to poor people. 🙂

Roger –

Thank you for your thoughtful response. Of course correlation is not causation. I beat that drum rather frequently myself. However, in the first graph you see consistent lock-step movement between income and consumption over decades, at both gross and fine levels. It takes more than a dismissive statement to deal with that kind of relationship.

Of course, it’s virtually impossible to prove causation. That’s why you need a compelling narrative that fits the real world data. And to refute, you need a more compelling narrative that fits the data at least as well.

In this post, when I talk about wealth, I mean personal wealth – which I take to be the accumulated residual of disposable income that has not kept, rather than disposed of.

In all due respect to Milton Friedman, the permanent income hypothesis strikes me as the kind of abstraction one can arrive at only by ignoring the real behaviors of real people – those 80% who own only 7% of the wealth. You have to believe that the guy at the big box store contemplating the purchase of a big screen TV is contemplating the size of his SS check 30 years hence, rather than the total of all his current bills vis-s-vis his curent pay check. That is not how people operate.

Seriously – have you ever heard of anyone basing a spending decision on the size of his next anticipated raise? Or his anticipated income stream over the next decade? If you can’t make the payments now (even if you’ve been suckered into a liar’s loan) you simply cannot and will not make the purchase. That’s why they have credit checks.

But if you give a hungry man a dollar, he will buy a hambuger.

Implicit in your argument, I think, are both humans as rational actors, and humans as forward-thinking actors. As a basis for theory, I reject both of these axioms, pretty much out of hand. In the real world, people are eratic, semi-rational, at best, and prone to making the biggest mistakes when the stakes and emotions are highest. And thinking clearly about the future is a luxury that few of us can afford, many of us simply don’t bother with, and few can do with any skill. Remember, 50% of the population is of below average intelligence.

On Pg 26 of your paper you show that GDP correlates better with consumption plus govt purchases than with consumption alone. In other words, the whole correlates better with the sum of two of its parts than it does with one of its parts alone. Isn’t this something approching a tautology?

I’ll give your paper a careful read.

Thanks again for your input.

Cheers!

JzB

Should say –

In this post, when I talk about wealth, I mean personal wealth – which I take to be the accumulated residual of disposable income that has BEEN kept, rather than disposed of.

Sorry for the bad proof-reading.

JzB

mcwop –

Are you making Krugman’s argument that the stimulus was too small?

JzB

Exactly so. You, Uncle Miltie and Thomas Paine.

Giving money to people who will spend it will do a lot more to solve a demand shortfall than giving it to those who will trade it for a non-productive financial asset.

JzB

Shorter Roger Farmer: I believe that humans are perfectly-rational beings who maximize economic utility across all possible time horizons, never face liquidity contraints, and that all people behave under full Ricardian Equivalence their entire lives.

Shorter, shorter Farmer: Even though reality shows me to be wrong, my theory says I’m correct, and I’m sticking to that.

Dean Baker: “Most of the literature has found a stock wealth effect in the range of 3-4 percent, usually with considerable lags.” He’s mentioned the housing wealth effect at 5-7% a year, collectively meaning that a $1 increase in financial or house prices (i.e. most wealth) leads to 3-7 cents in additional annual consumption.

What does Farmer think a $1 increase in sustainable annual income would lead to? My guess: A LOT more than 3-7 cents per year.

Not saying our stimulus was small or large. I think the stimulus was significant, they just filled the wrong hole. They filled bank holes, state holes, but not the consumer hole (which still exists). I think the only way you divert money to regular folks is through significantn (like reduce rates by 50%) tax cuts to people in the lower 95% for a single year. The cuts they did get were puny, the bailout the banks got was massive.

Sorry, to divert some money to poorer folks you give a big bump to the EITC for a year. Maybe double it.

Not sure I am for or against what I propose but it at least pointed at the right group.

Min –

I’ve read this three times, and i’m not sure I’m getting it. If you argue that we could learn more by having the data sliced, frex, into quintiles, rather than aggeagated, then I agree. But, at the risk of sounding, Rumsfeldian, I had to go with the data I had.

Other than that, despite your protestations, I think you’re making my case – at least sort of.

I can’t agree that for sombody on the high side of the wealth/income divide that spending would be directly proportional to wealth, as in doubling one doubles the other. As Steve Hamlin points out below, a small mutliplier in the range of 3 to 7% makes sense.

And that is only for those above whatever the cut-off is. Those who don’t see an extra 20 bucks at the end of the week as a no-to-be-missed chance to take the kids out for a pizza.

JzB (been there, done that)

Min

yes, the conclusion i reached from Farmer was that us poor people should take up a collection and give the money to the rich people, because god knows they will create wealth with it while we would only spend it on food.

i went to the bank and asked for a loan based on the present value of all my future work. they said no.

EITC – yes!

Tax cuts – Ihave really sever doubts, because 47% od the population pay no federal income tax, so that won’t help them.

JzB

i went to the bank and asked for a loan based on the present value of all my future work. they said no.

+1

JzB

When I was young, I spent most of my money of fast women and slow horses. The rest I just wasted.

coberly: “i went to the bank and asked for a loan based on the present value of all my future work. they said no.”

😉

Roger

that is funny as always. and thing is I would not disagree with you. The people you are disagreeing with are those who say every dime has to be “invested” even if that means the poor don’t eat, much less enjoy a moment of leisure or aspire to “consume” some pure luxury.

that might have made sense in a subsistence economy where “improvements” could be “seen” but “capital” was hard to come by.

it stops making much sense where there is more money than is “demanded” by any reasonable capital investment, and all of the fast women and slow horses are “consumed” by the very rich while the poor lead lives of progressive degradation.

i don’t expect the poor to lift themselves by their own bootstraps. an occasional strong or very smart person might. but ordinary people don’t. even back in the days of lords and serfs an intelligent lord would look after the welfare of his serfs.

Coberly,

Regrettably, I was not making a point. I just couldn’t resist the straight line.

However, I think you and I agree that not all “investments” are productive in the sense that they add anything, or as much as they cost, to the real economy. Blowing up asset bubbles and/or profitting from their collapse is a prime example–short term trading and speculation for the purpose of creating volatility and liquidity far in excess of what is useful to make markets for those in the real economy and then instantly consuming ALL the liquidity when the speculators themselves get into trouble. I was gratified to see earlier today on a Bloomberg panel discussion from Davos, “Big Banks: Cure or Curse,” that at least some bank regulators agree and are “studying” that as a potential problem.

My modest proposal: Divide “investment” into two categories–“productive” and “unproductive” depending on their contribution to the real economy.

Roger

well, i agree, but what’s the fun in that?

i think you’d get a big fight about ‘oo’s investments are more productive than ‘oo’s. i am not in favor of managing the economy by tax incentives. i am in favor of letting gamblers lose.

oh, and taxing trades.. you know, a kind of flat tax. just like a sales tax, only “where the money is.”

Roger –

That’s the way I think about it, though I haven’t quite decided where the boudary is. For sure, building physical plant, machinery, etc. is investment. Finacial manipulations are not.

Buying stocks and mutual funds in this narrow definition is not investment. It is speculation.

I don’t say that is bad, per se. But excessive speculation – as we have seen in, frex, oil in the last several years – is. Again, I don’t know how or where to place the line.

Cheers!

JzB

I’m not against taxing trades, but I’m really in love with the idea of minimum holding periods.

The average holding period on the NYSE is about 20 seconds.

This is totally nonproductive – and I can’t concieve of a credible counter-argument.

IMHO, it is evil rent-seeking in its purest form.

Cheers!

JzB

Quick drop-by comment –

nice post.

The productive/unproductive distinction was present in Adam Smith, David Ricardo, karl Marx, and likely many others such as sismondi.

The swing to neoclassical econ during the latter decades of the 19th c was also a swing away from emphasis on production – consumption as well as mythologies of general equilibrium and methodological individualism were given increasing weight,,,modern economics was being born.

Proliferation of joint-stock companies and the corporate form was also to increase the mass of fictitious capital [bonds, shares, etc], a term/concept in use for hundreds of years.

Juan